One of the consequences of globalization is that investors, analysts and companies can no longer stay focused on just their domestic markets, but have to also understand the risks and opportunities elsewhere in the world. When developed market companies first embarked on the journey of expanding into emerging market growth economies, investors pushed up their stock prices, primarily because of the potential that they saw in these markets for expansion. Over time, though, we have learned that, as with much else in business, this strategy comes with additional risk, not just from changing exchange rates, but from unstable economic and political forces. This growth/risk trade off explains why some companies have gained from value from globalizing and others have lost. In this post, I look at country risk through many lens, but with the end game of being able to incorporate it into decision making both for investors and businesses.

The Sources of Country Risk

When companies invest outside their domestic markets, the most immediate risk that they are exposed to is exchange rate risk, since revenues, profits and cash flows are affected by changing exchange rates. That risk, though, is but a piece of the puzzle, a symptom of economic fundamentals and affected by political crises. Digging deeper, the factors that make some countries riskier than others can be broadly classified into the following groups:

The Sources of Country Risk

When companies invest outside their domestic markets, the most immediate risk that they are exposed to is exchange rate risk, since revenues, profits and cash flows are affected by changing exchange rates. That risk, though, is but a piece of the puzzle, a symptom of economic fundamentals and affected by political crises. Digging deeper, the factors that make some countries riskier than others can be broadly classified into the following groups:

1. Life Cycle: I have used the construct of a corporate life cycle to talk about companies at different stages in the life cycle, and how they differ on cash flow generation and growth potential. It is also generally true that younger companies, deriving more or most of their value from future growth, are riskier than more mature companies, where the bulk of their value coming from investments already made. The same construct can be applied to countries, with emerging economies that are growing rapidly being more exposed to global shocks than mature countries. It should come as no surprise, therefore, that in almost every market crisis over the last decade, emerging markets have paid a much large price in terms of lost economic growth and lower market value than developed markets.

2. Political Risk: If the last few years have taught us a lesson, it is that politics can affect economic and market risk, not just in emerging markets, but also in developed ones. While there are many forms of political risk, ranging from abrupt changes in fiscal and monetary policy to regime change, there are at least two measurable manifestations of this risk in the form of corruption risk and exposure to violence.

- Corruption Risk: There are parts of the world where the costs of doing business include greasing palms and paying off intermediaries, and the roots lie deep, resisting feel-good quick fixes. While anecdotal stories of corruption and its consequences are plentiful, there are services to try to measure corruption levels across countries. Transparency International, for instance, derives a corruption score, by country, and in its 2019 report, provides a listing of the ten least and most corrupt countries in the world in the figure below, with higher scores indicating less corruption) for 2018.

The effect of corruption upon business is insidious, making winners of those most willing to play the bribery game and losers of those who resist. In an earlier post, I argued that corruption creates the equivalent of an informal tax, pushing down after-tax income to companies.

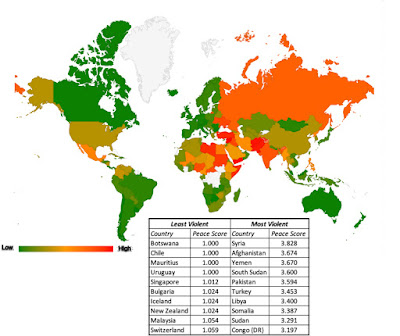

Source: Transparency International - Physical Violence: When talking about risk in investing or business, we tend to focus on financial risk, but it is undeniable that adding the threat of physical violence, from war, terrorism or crime, makes it more difficult to operate a business. There are services again that measure exposure to violence in different countries, and while each brings its own biases, the Institute of Economics and Peace has created and reports on a Global Peace Index, measuring exposure to violence, by country.

The map summarizes their findings from the most recent year. I must confess that I am surprised to see Botswana at the top of the list, but having never been there, that may be a reflection of my regional biases.

Source: Institute of Economics and Peace

3. Legal Risk: A business derives its value from the assets it owns, physical ord intangible, and to continue to derive value, it has to not only preserve its ownership but have a legal system that enforces it’s rights. The quality of this protection varies across countries, either because property rights have fewer protections in some countries or because those rights are not enforced in a timely manner in others. A group of non-government organizations has created an international property rights index, measuring the protection provided for property rights in different countries. The results in 2018, by region, are provided in the table below:

4. Economic Structure: Just as diversification helps investors spread their bets and reduce risk exposure, countries with more diversified economies are less exposed to global macroeconomic shocks than countries that derive their value from one or two industries, or as is often the case from one or two commodities. In a comprehensive study of commodity dependent countries, the United National Conference on Trade and Development (UNCTAD) measures the degree of dependence upon commodities across emerging markets and the figure reports the results.

|

| Source: UNCTAD |

Note the disproportional dependence on commodity exports that countries in Africa and Latin America have, making their economies and markets very sensitive to changes in commodity prices.

Measures of Country Risk

To the extent that country risk comes from different sources, you need composite measures of risk to help in decision making. This section begins with a look at country risk scores, where services, using proprietary factors, measure country risk with a number, followed with financial measures of country risk, primarily designed to measure default risk.

Measures of Country Risk

To the extent that country risk comes from different sources, you need composite measures of risk to help in decision making. This section begins with a look at country risk scores, where services, using proprietary factors, measure country risk with a number, followed with financial measures of country risk, primarily designed to measure default risk.

Country Risk Scores

There are services, ranging from the World Bank to the Economist that measure country risk with scores, though each one uses different criteria and scalars. The PRS Group provides numerical measures of country risk for more than a hundred countries, using twenty variables on three dimensions: political, financial and economic. The scores range from zero to one hundred, with high scores (80-100) indicating low risk and low scores indicating high risk. The figure below captures the June 2019 update, as well as the 10 countries that emerged as safest and riskiest in that update.

|

| Source: Political Risk Services (PRS) |

Default Risk Measures

Country risk scores have the benefit of being comprehensive, but they are also difficult to translate into business-friendly metrics. There are country risk measures in markets, albeit focused primarily on default risk, and the most public of these are sovereign ratings, there are now also market based measures, sovereign CDS spreads.

Sovereign Ratings

Moody’s, S&P and Fitch all estimate and publish ratings for countries, ranging from Aaa (AAA) for countries they view has having no default risk to D for countries already in default. The figure below provides a map of sovereign ratings across the world in July 2019, using Moody’s ratings where available and S&P to fill in some gaps. While the sovereign ratings themselves are alphabetical (and thus are difficult to incorporate into financial analysis), they can be converted to default spreads by looking at traded bonds in the market.

Sovereign Ratings

Moody’s, S&P and Fitch all estimate and publish ratings for countries, ranging from Aaa (AAA) for countries they view has having no default risk to D for countries already in default. The figure below provides a map of sovereign ratings across the world in July 2019, using Moody’s ratings where available and S&P to fill in some gaps. While the sovereign ratings themselves are alphabetical (and thus are difficult to incorporate into financial analysis), they can be converted to default spreads by looking at traded bonds in the market.

|

| Source: Moody's Sovereign Ratings |

Sovereign CDS Spreads

Ratings agencies have come under fire, especially since the 2008 crisis, with one of the primary critiques being their perceived bias. I am not being dismissive of that critique, but I believe that their bigger sin is that they are slow to respond to changing fundamentals, causing rating changes to lag real changes on the ground. In the last two decades, a market has risen to fill in the gap, where investors can buy protection against default risk by buying sovereign credit default swaps (CDS). If the insurance against default is complete, the price of a sovereign CDS can be viewed as a default spread for the country. On July 23, 2019, the map below summarizes the sovereign CDS spreads for the 81 countries that they were available for.

|

| Source: Bloomberg (10-year $ Sovereign Spreads) |

While these market-set default spreads provide more timely readings of sovereign default risk than the sovereign ratings, they suffer from the standard problems that all market-set numbers are exposed to. They are volatile, affected by momentum and mood and can give misguiding signals on risk.

Equity Risk

While default spreads may represent adequate measures of country risk if you intend to lend to a sovereign or buy bonds issued by it, you are exposed to more and sometimes different risks, if you plan to expand your business into a country, or invest in equities in that country, and you need equity risk premiums that capture that risk. It is true that many practitioners use default spreads as proxies of additional country equity risk and add it to a mature market premium (often a historical US premium) to arrive at country-specific equity risk premiums. As readers of this blog know, I use a mild variation on this approach, replacing the historical equity risk premium with an implied premium for the US and augmenting the default spread by a scaling factor, to reflect the higher risk of equity:

Equity Risk

While default spreads may represent adequate measures of country risk if you intend to lend to a sovereign or buy bonds issued by it, you are exposed to more and sometimes different risks, if you plan to expand your business into a country, or invest in equities in that country, and you need equity risk premiums that capture that risk. It is true that many practitioners use default spreads as proxies of additional country equity risk and add it to a mature market premium (often a historical US premium) to arrive at country-specific equity risk premiums. As readers of this blog know, I use a mild variation on this approach, replacing the historical equity risk premium with an implied premium for the US and augmenting the default spread by a scaling factor, to reflect the higher risk of equity:

The equity risk premiums that result from this process in July 2019 are reported in the picture below, with the implied equity risk premium of 5.67% for the S&P 500 on July 1, 2019, representing the base number.

|

Source: Damodaran Online (Current Data)

|

The picture continues a story that has been building over the last decade. While Africa and Latin America remain hotbeds of country risk, Asia has become safer over time and parts of Southern Europe have regressed.

If you are a developed market company or investor, and believe that risk in Africa, Latin America or parts of Asia don’t apply to you, you may want to think again. The risk exposure of a company does not come from where it is incorporated but from where it does business. Thus, Coca Cola and Royal Dutch may be US and UK-listed companies respectively, but their business models expose them to risk around the world. With Coca Cola, that risk comes primarily from where it sells its products. With Royal Dutch, the risk is derived from where it extracts its oil and gas, making it more exposed to emerging markets than many emerging market companies. By the same token, Vale and Infosys may be Brazil and India-based companies, but there are both global companies that are exposed to risk in the rest of the globe. In addition, when multinationals try to estimate hurdle rates for projects, it should reflect not just the currency you do the analysis in but also the country in which the project will be located. A Royal Dutch refinery investment in Nigeria will have a higher hurdle rate than an otherwise similar refinery investment in the United States. If you find these concepts intriguing, I have my annual update on country risk available for download at this link. Be warned! It may operate as a narcoleptic to those who are sleep deprived.

Conclusion

There was a time a few decades ago when the line between developed and emerging markets was a clear one. On one side were developed markets, with independent central banks, rule-following governments and stable fiscal policies, and on the other side were emerging markets, with unstable and unpredictable political leadership and central banks that did their bidding. The last decade has seen a blurring of lines, as some “developed markets” mimic emerging market behavior and some emerging markets mature. There are some (companies and investors) who have decided that this convergence is a reason to ignore country risk, but I think that they do so at their own peril. Notwithstanding globalization and convergence on some dimensions of risk, we face wide variations in risk across the world, and prudence and good sense demand that we incorporate these differences into our decisions.

There was a time a few decades ago when the line between developed and emerging markets was a clear one. On one side were developed markets, with independent central banks, rule-following governments and stable fiscal policies, and on the other side were emerging markets, with unstable and unpredictable political leadership and central banks that did their bidding. The last decade has seen a blurring of lines, as some “developed markets” mimic emerging market behavior and some emerging markets mature. There are some (companies and investors) who have decided that this convergence is a reason to ignore country risk, but I think that they do so at their own peril. Notwithstanding globalization and convergence on some dimensions of risk, we face wide variations in risk across the world, and prudence and good sense demand that we incorporate these differences into our decisions.

YouTube Video

Paper on Country Risk

Country Risk: Determinants, Measures and Implications - The 2019 Edition

Data Links

- Measures of Corruption, by Country (Transparency International)

- Measures of Violence, by Country (Institute for Peace and Economics)

- International Property Rights Index

- Commodity Dependence, by country (UNCTAD)

- Country Risk Scores (PRS Group)

- Sovereign Ratings, by Country (Moody's, S&P)

- Sovereign CDS Spreads (10-year) on 7/21/2019

- Equity Risk Premium, by country (Damodaran Online)

1 comment:

Hi Professor,

In valuing emerging market company, like in Egypt or turkey with high Risk free rate up to 12% it led to value destroy at the end, cant assume growth to continue above the cost of equity for terminal value, how to deal with such issue,

Post a Comment