I have made no secret of my disdain for ESG, an over-hyped and over-sold acronym, that has been a gravy train for a whole host of players, including fund managers, consultants and academics. In response, I have been told that the problem is not with the idea of ESG, but in its measurement and application, and that impact investing is the solution to both market and society's problems. Impact investing, of course, is investing in businesses and assets based on the expectation of not just earning financial returns, but also creating positive change in society.

It is human nature to want to make the world a better place, but does impact investing have the impact that it aims to create? That is the question that I hope to address in this post. In the course of the post, I will work with two presumptions. The first is that the problems for society that impact investing are aiming to address are real, whether it be climate change, poverty or wealth inequality. The second is that impact investors have good intentions, aiming to make a positive difference in the world. I understand that there will be some who feel that these presumptions are conceding too much, but I want to keep my focus on the mechanics and consequences of impact investing, rather than indulge in debates about society's problems or question investor motives.

Impact Investing: The What, The Why and the How!

Impact investments are investments made with the intent of generating benefits for society, alongside a financial return. That generic definition is not only broad enough to cover a wide range of impact investing actions and motives, but has also been with us since the beginning of time. Investors and business people have often considered social payoffs when making investments, though they have differed on the social outcomes that they seek, and the degree to which they are willing to sacrifice the bottom line to achieve those outcomes.

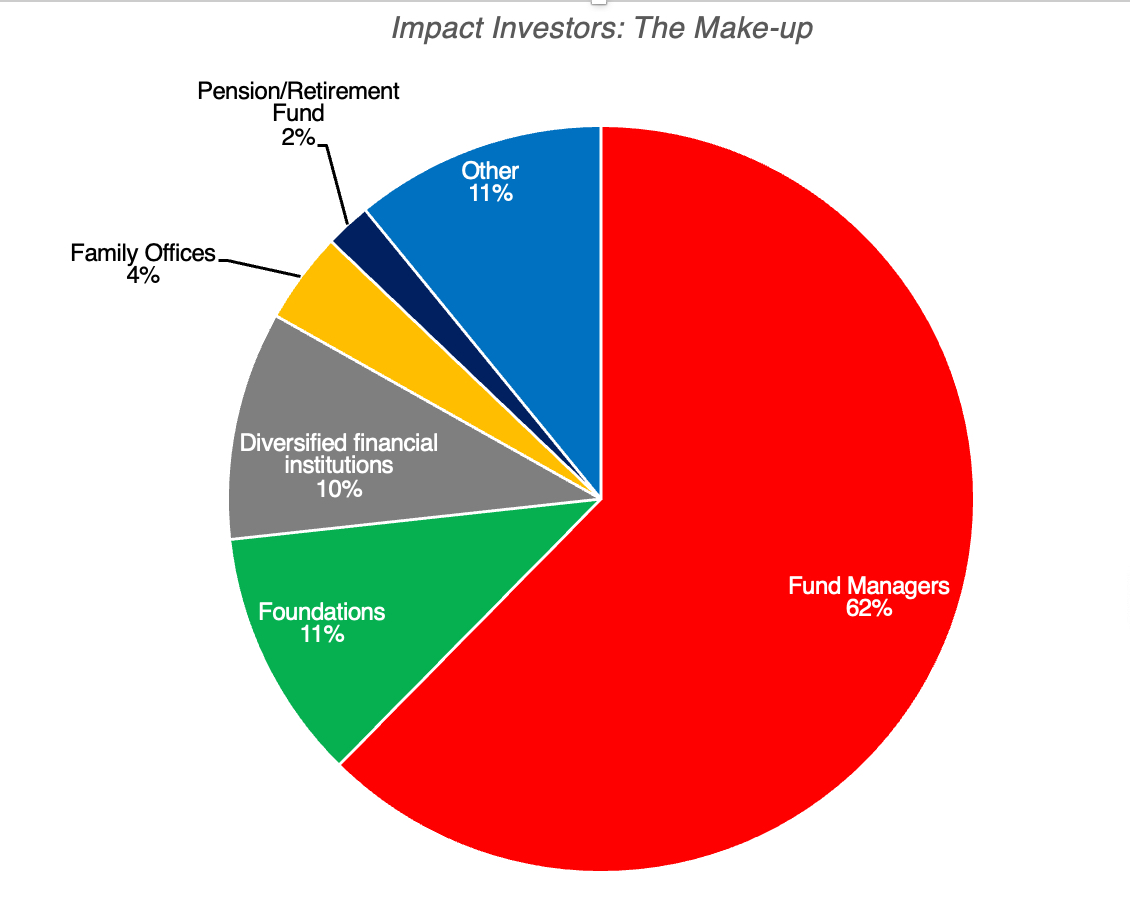

In the last two decades, this age-old investing behavior has come under the umbrella of impact investing, with several books on how to do it right, academic research on how it is working (or not), and organizations dedicated to advancing its mission. The Global Impact Investing Network (GIIN), a non-profit that tracks the growth of this investing movement, estimated that more than $1.16 trillion was invested by impact investors in 2021, with a diverse range of investors:

Global Impact Investing Network, 2022 Report

Not surprisingly, the balance between social impact and financial return desired by investors, varies across investor groups, with some more focused on the former and others the latter. In a survey of impact investors, GIIN elicited these responses on what types of returns investors expected to earn on their impact investments, broken down by groups:

Global Impact Investing Network, 2020 Report

Almost two thirds of impact investors believe that they can eat their cake and have it too, expecting to earn as much or more than a risk-adjusted return, even as they do good. That delusion running deepest among pension funds, insurance companies, for-profit fund managers and diversified financial investors, who also happen to account for 78% of all impact investing funds.

If having a positive impact on society, while earning financial returns, is what characterizes impact investing, it can take one of three forms:

Inclusionary Impact Investing: On the inclusionary path, impact investors seek out businesses or companies that are most likely to have a positive impact on whatever societal problem they are seeking to solve, and invest in these companies, often willing to pay higher prices than justified by the financial payoffs on the business.

Exclusionary Impact Investing: In the exclusionary segue, impact investors sell shares in businesses that they own, or refuse to buy shares in these businesses, if they are viewed as worsening the targeted societal problem.

Evangelist Impact Investing: In the activist variant, impact investors buy stakes in businesses that they view as contributing to the societal problem, and then use that ownership stake to push for changes in operations and behavior, to reduce the negative social or environmental impact.

The effect of impact investing in the inclusionary and exclusionary paths is through the stock price, with the buying (selling) in inclusionary (exclusionary) investing pushing stock prices up (down), which, in turn, decreases (increases) the costs of equity and capital at these firms. The changes in costs of funding then show up in investing decisions and growth choices at these companies, with good companies expanding and bad companies shrinking.

With evangelist impact investing, impact investors aim to get a critical mass of shareholders as allies in pushing for changes in how companies operate, shifting the company away from actions that create bad consequences for society to those that have neutral or good consequences.

As you can see, for impact investing to have an impact on society, a series of links have to work, and if any or all of them fail, there is the very real potential that impact investing can have perverse consequences.

With inclusionary investing, there is the danger that you mis-identify the companies capable of doing good, and flood these companies with too much capital. Not only is capital invested in these companies wasted, but increases the barriers to better alternatives to doing good.

With exclusionary investing, pushing prices down below their "fair" values will allow investors who don’t care about impact to earn higher returns, from owning these companies. More importantly, if it works at reducing investment from public companies in a "bad" business, it will open the door to private investors to fill the business void.

With evangelist investing, an absence of allies among other shareholders will mean that your attempts to change the course of businesses will be largely unsuccessful. Even when you are successful in dissuading these companies from "bad" investments, but may not be able to stop them from returning the cash to shareholders as dividends and buybacks, rather than making "good" investments.

In the table below, I look at the potential for perverse outcomes under each of three impact investing approaches, using climate change impact investing as my illustrative example:

The question of whether impact investing has beneficial or perverse effects is an empirical question, not a theoretical one, since your assumptions about market depth, investor behavior and business responses can lead you to different conclusion.

It is worth noting that impact investing may have no effect on stock prices or on corporate behavior, either because there is too little money behind it, or because there is offsetting investing in the other direction. In those cases, impact investing is less about impacting society and more about alleviating the guilt and cleansing the consciences of the impact investors, and the only real impact will be on the returns that they earn on their portfolios.

The Impact of Impact Investing: Climate Change

While impact investing can be directed at any of society's ills, it is undeniable that its biggest focus in recent years has been on climate change, with hundreds of billions of dollars directed at reversing its effects. Climate change, in many ways, is also tailored to impact investing, since concerns about climate change are widely held and many of the businesses that are viewed as good or bad, from a climate change perspective, are publicly traded. As an empirical question, it is worth examining how impact investing has affected the market perceptions and pricing of green energy and fossil fuel companies, the operating decisions at these companies, and most critically, on the how we produce and consume energy.

Fund Flows

The biggest successes of climate change impact investing have been on the funding side. Not only has impact investing directed large amounts of capital towards green and alternative energy investments, but the movement has also succeeded in convincing many fund managers and endowments to divest themselves of their investments in fossil fuel companies.

As concerns about climate change have risen, the money invested in alternative energy companies has expanded, with $5.4 trillion cumulatively invested in the last decade:

Source: BloombergNEF

Almost half of this investment in alternative energy sources has been in renewable energy, with electrified transport and electrified heat accounting for a large portion of the remaining investments.

On the divestment side, the drumbeat against fossil fuel investing has had an effect, with many investment fund managers and endowments joining the divestiture movement:

By 2023, close to 1600 institutions, with more than $40 trillion of funds under their management, had announced or concluded their divestitures of investments in fossil fuel companies.

If impact investing were measured entirely on fund flows into green energy companies and out of fossil fuel companies, it has clearly succeeded.

Market Price (and Capitalization)

It is undeniable that fund flows into or out of companies affects their stock prices, and if the numbers in the last section are even close to reality, you should have expected to see a surge in market prices at alternative energy companies, as a result of funds flowing into them, and a decline in market prices of fossil fuel companies, as fossil fuel divestment gathers steam.

On the alternative energy front, as money has flowed into these companies, there has been a surge in enterprise value (equity and net debt) and market capitalization (equity value); I report both because impact investing can also take the form of green bonds, or debt, at these companies. The enterprise value of publicly traded alternative energy companies has risen from close to zero two decades ago to more than $700 billion in 2020, before losing steam in the last three years:

Adding in the value of private companies and start-ups in this space would undoubtedly push up the number further.

On the fossil fuel front, the fossil fuel divestments have had an impact on market capitalizations, though there are signs that the effect is weakening:

In the last decade, when fossil fuel divestment surged, the percentage changes in market capitalization at fossil fuel companies lagged returns on the market, with fossil fuel companies reporting a compounded annual percentage increase of 4.49% a year.. The negative effect was strongest in the middle of the last decade, but market prices for fossil fuel companies have recovered strongly between 2020 and 2023.

It is worth noting that even after their surge in market cap in the last decade, alternative energy companies have a cumulated enterprise value of about $600 billion in September 2023, a fraction of the $8.5 trillion of cumulated enterprise value at fossil fuel companies.

Investor perceptions

Impact investing has always been about changing investor perceptions of energy companies, more than just prices. In fact, some impact investors have argued that their presence in the market and advocacy for alternative energy has led investors to change their views about fossil fuel companies, shifting from viewing them as profitable, cash-rich businesses with extended lives, to companies living on borrowed time, looking at decline and even demise. In intrinsic valuation terms, that shift should show up in the pricing, with lower value attached to the latter scenario than the former:

On the green energy front, to see if investors perceptions of these companies have changed, I look at two the pricing metrics for green energy companies - the enterprise value to EBITDA and enterprise value to revenue multiples:

The numbers offer a mixed message on whether impact investing has changed investor perceptions, with EV to EBITDA multiples staying unchanged, between the 1998-2010 and 2011-2023 time periods, but EV as a multiple of revenues soaring from 2.62 in the 1998-2010 time period to 5.95 in the 2011-2023 time period. The fund flows into green energy are affecting pricing, though it remains an open question as to whether the pricing is getting too rich, as too much money chases too few opportunities.

Looking at fossil fuel firms, the poor performance in the last decade seems to support the notion that impact investing has changed how investors perceive fossil fuel companies, but there are some checks that need to be run to come that conclusion.

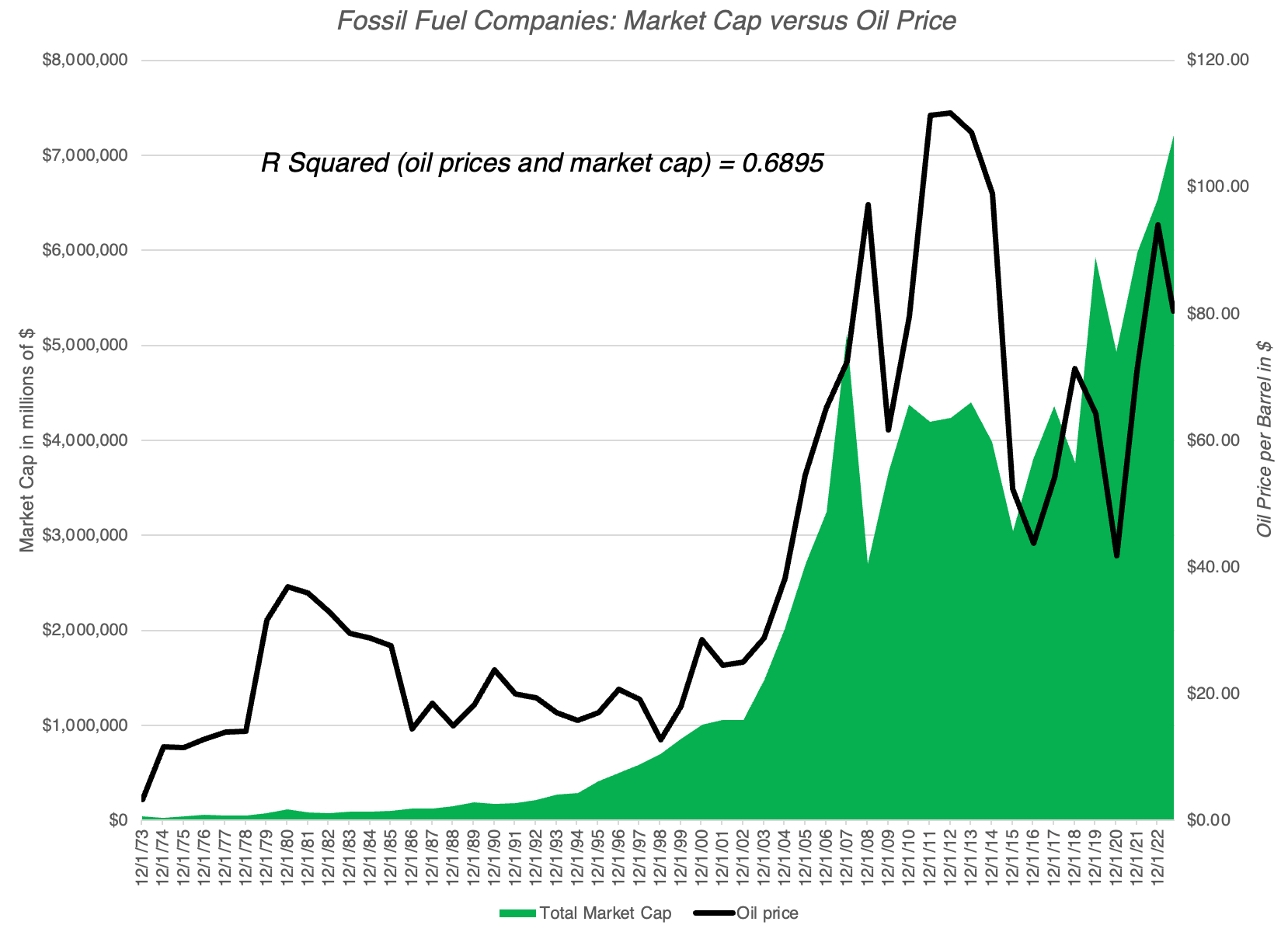

Oil Price Effect: The market capitalization of oil companies is dependent on oil prices, as you can see in the figure below, where the collective market capitalization of fossil fuel companies is graphed against the average oil price each year from 1970 to 2022; almost 70% of the variation in market capitalization over time explained by oil price movements.

To separate impact investing divestment effects from oil price effects, I estimated the predicted market capitalization of fossil fuel companies, given the oil price each year, using the statistical relationship between market cap and oil prices in the twenty five years leading into the forecast year. (I regress market capitalization against average oil price from 1973 to 1997 to estimate the expected market cap in 1998, given the oil price in 1998, and so on, for every year from 1998 to 2023. Note that the only thing you can read these regressions is that market capitalization and oil prices move together, and that there is no way to draw conclusions about causation):

If divestitures are having a systematic effect on how markets are pricing fossil fuel companies, you should expect to see the actual market capitalizations trailing the expected market capitalization, based on the oil price. That seems to be the case, albeit marginally, between 2011 and 2014, but not since then. In short, the divestiture effect on fossil fuel companies has faded over time, with other investors stepping in and buying shares in their companies, drawn by their earnings power.

Pricing: If impact investing is changing investor perceptions about the future growth and termination risk at fossil fuel companies, it should show up in how these companies are priced, lowering the multiples of revenues or earnings that investors are willing to pay. In the chart below, I look at the pricing of fossil fuel companies over time, using EV to sales and EV to EBITDA as pricing metrics:

While the pricing metrics swing from year to year, that has always been true at oil companies, since earnings and revenues vary, with oil prices. However, if impact investing is having a systematic effect on how investors are pricing companies, there is little evidence of that in this chart.

In sum, while it is possible to find individual investors who have become skeptical about the future for fossil fuel companies, that view is not reflective of the market consensus. I do believe that investors are pricing fossil fuel companies now, with the expectation of much lower growth in the future, than they used to, but that is coming as much from these companies returning more of their earnings as cash and reinvesting less than they used to, as it is from an expectation that the days of fossil fuel are numbered. Some impact investors will argue that this is because investors are short-term, but that is a double-edged sword, since it undercuts the very idea of using investing as the vehicle to create social and environmental change.

Operating Impact

Impact investing, in addition to affecting pricing of green energy and fossil fuel companies, can also have effects on how fossil fuel companies perform and operate. On the profitability front, fossil fuel companies seem to have weathered the onslaught of climate change critics, with revenues and profit margins (EBITDA and operating) bouncing back from a slump between 2014 and 2018 to reach historic highs in 2022.

A key development over the last decade, as profits have returned, is that fossil fuel companies are returning much of cash flows that they are generating to their shareholders in the form of dividends and buybacks, notwithstanding the pressure from activist impact investors that they reinvest that money in green energy projects:

In one development that impact investors may welcome, fossil fuel companies are collectively investing less in exploration for new fossil fuel reserves in the last decade than they did in prior ones:

If you couple this trend of exploring less with the divestitures of fossil fuel reserves, over the last decade, there is a basis for the argument that fossil fuel companies are reducing their fossil fuel presence, and some impact investing advocates may be tempted to declare victory. After all, if the objective is to reduce fossil fuel production, does it not advance your cause if less money is being spent exploring for coal, oil and gas?

Before claiming a win, though, there is a dark side to this retreat by public fossil-fuel companies, and that comes from private equity investors and privately-owned (or government-owned) oil companies stepping into the breach; many of the divestitures and sales of fossil fuel assets by publicly traded companies have been to private buyers, and the assets being divested are often among the dirtiest (from a climate-change perspective) of their holdings.. Over the last decade, some of private equity’s biggest players have invested well over $1.1 trillion in fossil fuel, with the investments ranging the spectrum.

Source: Pitchbook

While there was an uptick in investments in renewables in 2019 and 2020, the overwhelming majority of private equity investments during the decade were in fossil fuels. In the process, private equity firms like the Carlyle Group and KKR have become major holders of fossil fuel reserves, and there are a few private buyers who have profited from buying abandoned and castoff oil wells from oil companies, pressured to sell by impact investors. While climate change advocates are quick to point to this public-to-private transition of fossil fuel assets as a flaw, they fail to recognize that it is is a natural side-effect of an approach that paints publicly traded fossil fuel firms as villains and shuns their investments, while continuing to be dependent on fossil fuels for meeting energy needs.

The success or failure of impact investing, when it relates to climate change, ultimately comes from the changes it creates in how energy is produce and consumed, and it is on this front that the futility of the movement is most visible. While alternative energy sources have expanded their production, it has not been at the expense of oil consumption, which has barely budged over the last decade.

Fairly or unfairly, the pandemic seems to have done more to curb oil consumption than all of impact investing's efforts over the last decade, but the COVID effect, which saw oil consumption drop in 2020 has largely faded.

Taking a global and big-picture perspective of where we get our energy, a comparison of energy sources in 1971 and 2019 yields a picture of how little things have changed:

Fossil fuel, which accounted for 86.6% of energy production in 1971, was responsible for 80.9% of production in 2019, with almost all of that gain from coming from nuclear energy, which many impact investors viewed as an undesirable alternative energy source for much of the last decade. Focusing on energy production just in the US, the failure of impact investing to move the needle on energy production can be seen in stark terms:

Fossil fuels account for a higher percent of overall energy produced in the United States today than they did ten or fifteen years ago, with gains in solar, wind and hydropower being largely offset by reductions in nuclear energy. If this is what passes for winning in impact investing, I would hate to see what losing looks like.

I have tried out variants of this post with impact investing acquaintances, and there are three broad responses that they have to its findings (and three defenses for why we should keep trying):

Things would be worse without impact investing: It is impossible to test this hypothetical, but is it possible that our dependence on fossil fuels would be even greater, without impact investing making a difference? Of course, but that argument would be easier to make, if the trend lines were towards fossil fuels before impact investing, and moved away from fossil fuels after its rise. The data, though, suggests that the biggest shift away from fossil fuels occurred decades ago, well before impact investing was around, primarily from the rise of nuclear energy, and that impact investing's tunnel vision on alternative energy has actually made things worse.

It takes time to create change: It is true that the energy business is an infrastructure business, requiring large investments up front and long gestation periods. It is possible that the effects of impact investing are just not being felt yet, and that they are likely to show up later this decade. This would undercut the urgency argument that impact investors have used to induce their clients to invest large amounts and doing it now, and if they had been more open about the time lag from the beginning, this argument would have more credibility today.

Investing cannot offset consumption choices: If the argument is that impact investing cannot stymie climate change on its own, without changes in consumer behavior, I could not agree more, but changing behavior will be painful, both politically and economically. I would argue that impact investing, by offering the false promise of change on the cheap, has actually reduced the pressure on politicians and rule-makers to make hard decisions on taxes and production.

Even conceding some truth in all three arguments, what I see in the data is the essence of insanity, where impact investors keep throwing in more cash into green energy and more vitriol at fossil fuels, while the global dependence on fossil fuels increases.

Impact Investing: Investing for change

Much of what I have said about impact investing's quest to fight climate change can be said about the other societal problems that impact investors try to address. Poverty, sexism, racism and inequality have had impact investing dollars directed at them, albeit not on the same scale as climate change, but are we better off as a society on any of these dimensions? To the response that doing something is better than being doing nothing, I beg to differ, since acting in ways that create perverse outcomes can be worse than sitting still. To end this post on a hopeful note, I believe that impact investing can be rescued, albeit in a humbler, more modest form.

With your own money, pass the sleep test: If you are investing your own money, your investing should reflect your pocketbook as well as your conscience. After all, investors, when choosing what to invest in, and how much, have to pass the sleep test. If investing in Exxon Mobil or Altria leads you to lose sleep, because of guilt, you should avoid investing in these companies, no matter how good they look on a financial return basis.

With other people's money, be transparent and accountable about impact: If you are investing other people’s money, and aiming for impact, you need to be explicit on what the problem is that you are trying to solve, and get buy in from those who are investing with you. In addition, you should specify measurement metrics that you will use to evaluate whether you are having the impact that you promised.

Be honest about trade offs: When investing your own or other people's money, you have to be honest with yourself not only about the impact that you are having, but about the trade offs implicit in impact investing. As someone who teaches at NYU, I believe that NYU's recent decision to divest itself of fossil fuels will not only have no effect on climate change, but coming from an institution that has established a significant presence in Abu Dhabi, it is an act of rank hypocrisy. It is also critical that those impact investors who expect to make risk-adjusted market returns or more, while advancing social good, recognize that being good comes with a cost.

Less absolutism, more pragmatism: For those impact investors who cloak themselves in virtue, and act as if they command the moral high ground, just stop! Not only do you alienate the rest of the world, with your I-care-about-the-world-more-than-you attitude, but you eliminate any chances of learning from your own mistakes, and changing course, when your actions don't work.

Harness the profit motive: I know that for some impact investors, the profit motive is a dirty concept, and the root reason for the social problems that impact investing is trying to address. While it is true that the pursuit of profits may underlie the problem that you are trying to solve, the power from harnessing the profit motive to solve problems is immense. Agree with his methods or not, Elon Musk, driven less by social change and more by the desire to create the most valuable company in the world, has done more to address climate change than all of impact investing put together.

I started this post with two presumptions, that the social problems being addressed by impact investors are real and that impact investors have good intentions, and if that is indeed the case, I think it is time that impact investors face the truth. After 15 years, and trillions invested in its name, impact investing, as practiced now, has made little progress on the social and environmental problems that it purports to solve. Is it not time to try something different?

A few days ago, I valued Instacart ahead of its initial public offering, and noted that the reception that the stock gets will be a good barometer of where risk capital stands in the market, right now. After a buzzy open, when the stock jumped from its offering price of $30 a share to $42, the stock has quickly given up those gains and now trades at below to its offer price. In this post, I will look at another initial public offering, Birkenstock, that is likely to get more attention in the next few weeks, given that it is targeting to go public at a pricing of about €8 billion, for its equity, in a few weeks. Rather than make this post all about valuing Birkenstock, and comparing that value to the proposed pricing, I would like to use the company to discuss how intangible assets get valued in an intrinsic valuation, and why much of the discussion of intangible valuation in accounting circles is a reflection of a mind-set on valuation that often misses its essence.

The Value of Intangible Assets

Accounting has historically done a poor job dealing with intangible assets, and as the economy has transitioned away from a manufacturing-dominated twentieth century to the technology and services focused economy of the twenty first century, that failure has become more apparent. The resulting debate among accountants about how to bring intangibles on to the books has spilled over into valuation practice, and many appraisers and analysts are wrongly, in my view, letting the accounting debate affect how they value companies.

The Rise of Intangibles

While the debate about intangibles, and how best to value them, is relatively recent, it is unquestionable that intangibles have been a part of valuation, and the investment process, through history. An analyst valuing General Motors in the 1920s was probably attaching a premium to the company, because it was headed by Alfred Sloan, viewed then a visionary leader, just as an investor pricing GE in the 1980s was arguing for a higher pricing, because Jack Welch was engineering a rebirth of the company. Even a cursory examination of the the Nifty Fifty, the stocks that drove US equities upwards in the early 1970s, reveals companies like Coca Cola and Gilette, where brand name was a significant contributor to value, as well as pharmaceutical companies like Bristol-Myers and Pfizer, which derived a large portion of their value from patents. In fact, IBM and Hewlett Packard, pioneers of the tech sector, were priced higher during that period, because of their technological strengths and other intangibles. Within the investment community, there has always been a clear recognition of the importance of intangibles in driving investment value. In fact, among old-time value investors, especially in the Warren Buffet camp, the importance of having "good management' and moats (competitive advantages, many of which are intangible) represented an acceptance of to how critical it is that we incorporate these intangible benefits into investment decisions.

With that said, it is clear that the debate about intangibles has become more intense in the last two decades. One reason is the perception that intangibles now represent a greater percent of value at companies and are a significant factor in more of the companies that we invest in, than in the past. While I have seen claims that intangibles now account for sixty, seventy or even ninety percent of value, I take these contentions with a grain of salt, since the definition of "intangible" is elastic, and some stretch it to breaking point, and the measures of value used are questionable. A more tangible way to see why intangibles have become a hot topic of discussion is to look at the evolution of the top ten companies in the world, in market capitalization, over time:

In 1980, IBM was the largest market cap company in the world, but eight of the top ten companies were oil or manufacturing companies. With each decade, you can see the effect of regional and sector performance in the previous decade; the 1990 list is dominated by Japanese stocks, reflecting the rise of Japanese equities in the 1980s, and the 2000 list by technology and communication companies, benefiting from the dot-com boom. Looking at the top ten companies in 2020 and 2023, you see the dominance of technology companies, many of which sell products that you cannot see, often in production facilities that are just as invisible.

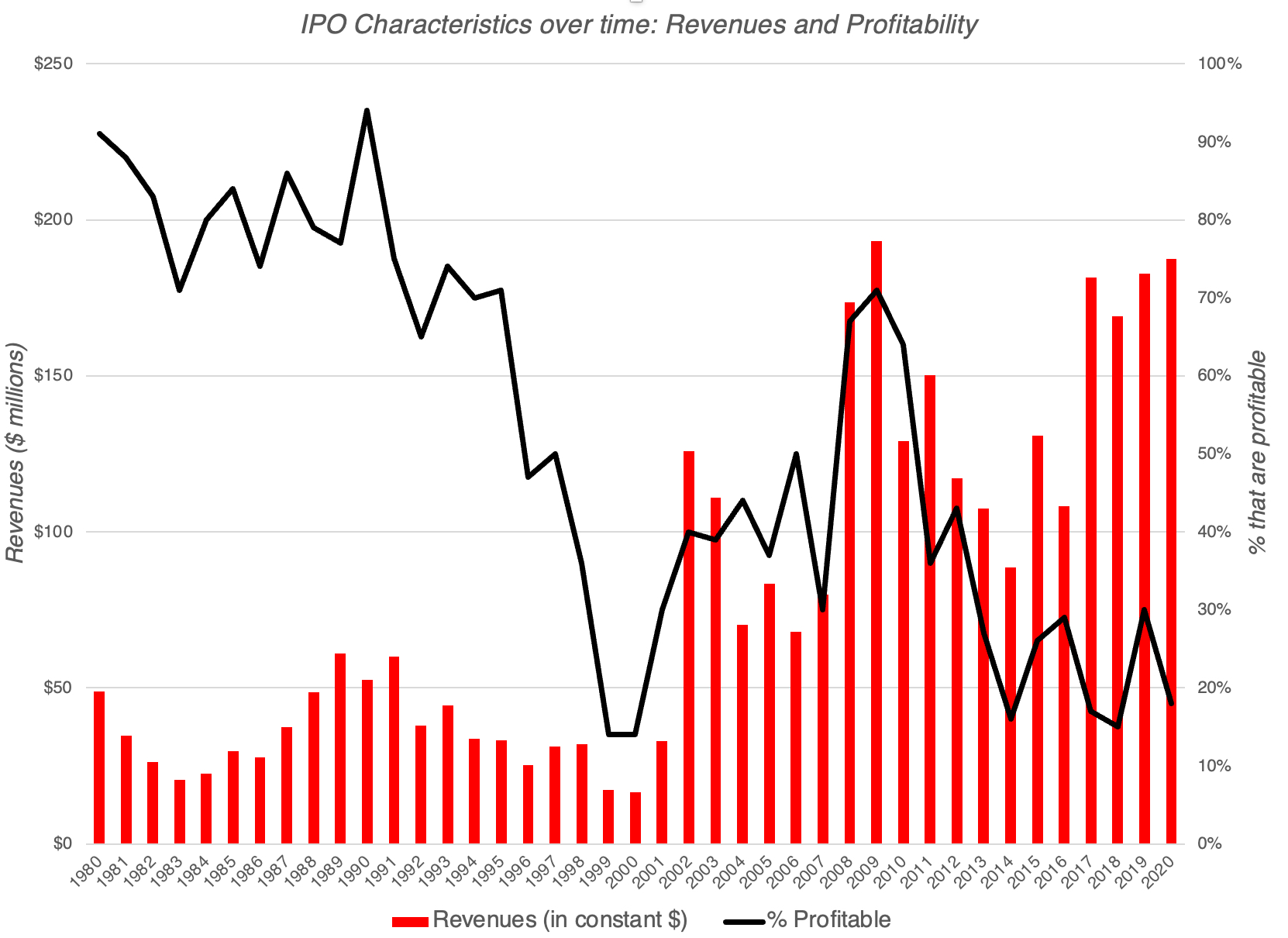

The other development that has pushed the intangible discussion to the forefront is a sea change in the characteristics of companies entering public markets. While companies that were listed for much of the twentieth century waited until they had established business models to go public, the dot-com boom saw the listing of young companies with growth potential but unformed business models (translating into operating losses), and that trend has continued and accelerated in this century. The graph below looks at the revenues and profitability of companies that go public each year, from 1980 to 2020:

As you can see, the percent of money-making companies going public has dropped from more than 90% in the 1980s to less than 20% in 2020, but at the same time, while also reporting much higher revenues, reporting the push by private companies to scale up quickly. In valuing these companies, investors and analysts face a challenge, insofar as much of the values of these firms came from expectations of what they would do in the future, rather than investments that they have already made. I capture this effect in what I call a financial balance sheet:

While you can value assets-in-place, using historical data and the information in financial statements, in assessing the value of growth assets, you are making your best assessments of investments that these companies will make in the future, and these investments are formless, at least at the moment.

The Accounting Challenge with Intangibles

The intangible debate is most intense in the accounting community, with both practitioners and academics arguing about whether intangibles should be "valued", and if so, how to bring that value into financial statements. To see why the accounting consequences are likely to be dramatic, consider how these choices will play out in the balance sheet, the accountants' attempt to encapsulate what a business owns, what it owes and how much its equity is worth.

There are inconsistencies in how accountants measure different classes of assets, and I incorporate them into my picture above, leaving the intangible assets section as the unknown: Any changes in accounting rules on measuring the value of intangibles, and bringing them on the balance sheet, will also play out as changes on the other side of the balance sheet, primarily as changes in the value of assessed or book equity. Put simply, if accountants decide to bring intangible assets like brand name, management quality and patent protection into asset value will increase the value of book equity, at least as accountants measure it, in that company.

In their attempt to bring intangible assets on to balance sheets, accountants face a barrier of their own creation, emanating from how they treat the expenditures incurred in building up these assets. To understand why, consider how fixed assets (such as plant and equipment and equipment) become part of the balance sheet. The expenditures associated with acquiring these fixed assets are treated as capital expenditures, separate from operating expenses, and only the portion of that expenditure (depreciation or amortization) that is assumed to be related to the current year's operations is treated as an operating expense. The unamortized or un-depreciated portions of these capital expenses are what we see as assets on balance sheets. The expenses that result in intangible asset acquisitions are, for the most part, not treated consistently, with brand name advertising, R&D expenses and investments in recruiting/training, the expenses associated with building up brand name, patent protection and human capital, respectively, being treated as operating, rather than capital, expenses. As a consequence of this mistreatment, I have argued that not only are the biggest assets, mostly intangible, at some companies kept off the balance sheet, but their earnings are misstated:

There are ways in which accounting can fix this inconsistency, but it will result in an overhaul of all of the financial statements, and companies and investors balk at wholesale revamping of accounting numbers (EBITDA, earnings per share, book value) that they have relied on to price these firms.

So, how far has accounting come in bringing intangible assets on to balance sheets? One way to measure progress on this issue is to look at the portion of the book value of equity at US companies that comes from tangible assets, in the chart below:

Looking across all US firms from 1980 to 2022, the portion of book value of equity that comes tangible assets has dropped from more than 70% in 1998 to about 30% in 2022. That would suggest that intangible assets are being valued and incorporated into balance sheets much more now than in the past. Before you come to that conclusion, though, you may want to consider the breakdown of the intangible assets on accounting balance sheets, which I do in the graph below:

Over the last 25 years, as intangible assets have risen in value, goodwill has been, by far, the biggest single component of that value, accounting for about 60% of all intangibles on US corporate balance sheets; the jump in 2001 came from a change in accounting rules on acquisitions, when pooling was banned and companies were forced to recognize goodwill on all acquisitions. So what? I have long argued that goodwill is not an asset, intangible or not, but more a plug variable, signifying the difference between the price paid to acquire a target company and its book value, with adjustments for fairness, and designed to make balance sheets balance. Thus, much of the talk about intangibles in accounting has been just that, talk, with little of real consequence for balance sheets.

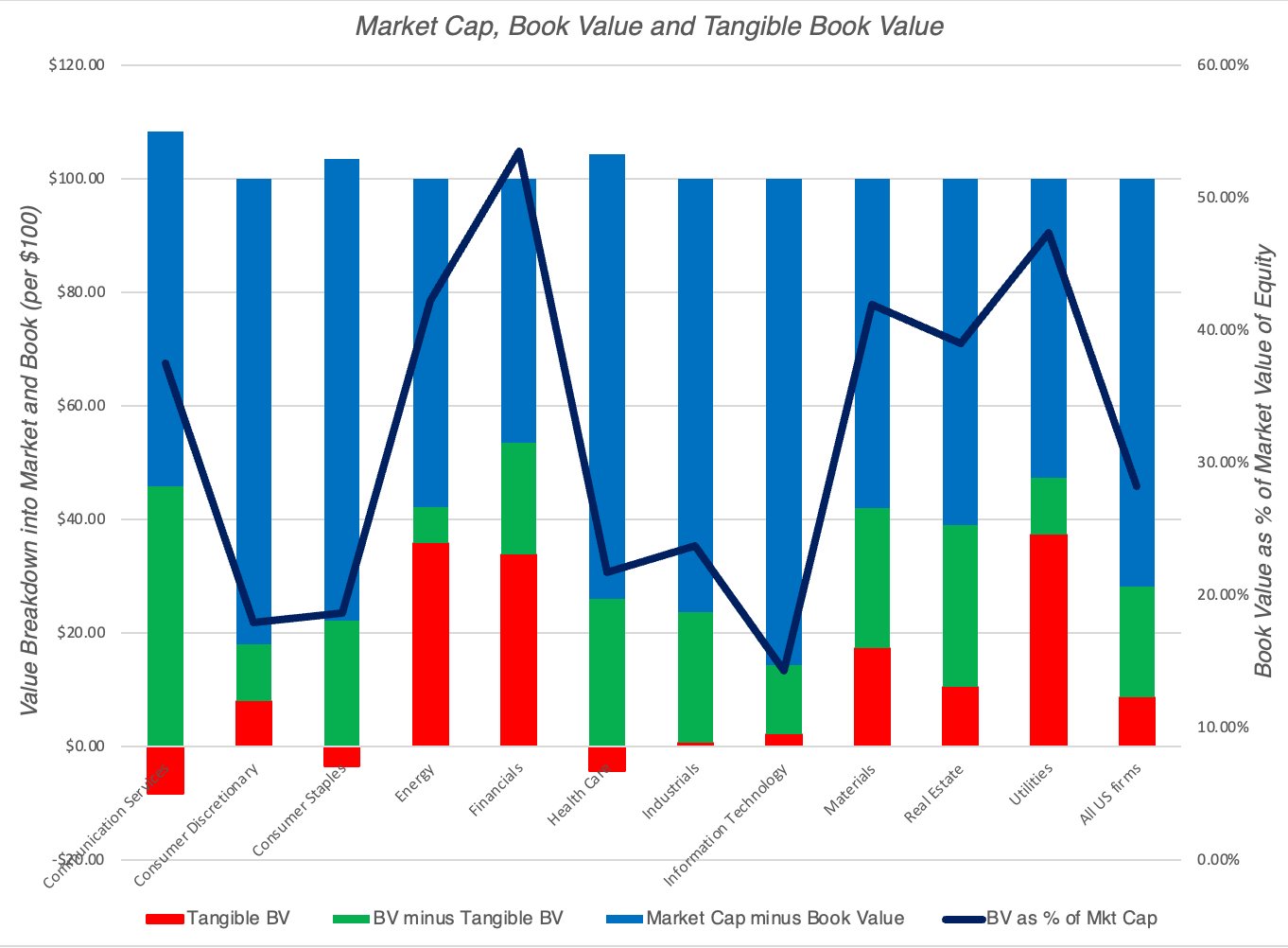

There is another measure that you can use to see the futility, at least so far, of accounting attempts to value intangibles. In the graph below, I look at the aggregated market capitalization of companies, in 2022, which should incorporate the pricing of intangibles by the market, and compare that value to book value (tangible and intangible), by sector, reflecting accounting attempts to value these same intangibles.

The sectors where you would expect intangible assets to be the largest portion of value are consumer products (brand name) and technology (R&D and patents). These are also the sectors with the lowest book values, relative to market value, suggesting that whatever accountants are doing to bring in intangibles in these companies into book value is not having a tangible effect on the numbers.

In sum, the accounting obsession with intangibles, and how best to deal with them, has not translated into material changes on balance sheets, at least with GAAP in the United States. It is true that IFRS has moved faster in bringing intangible assets on to balance sheets, albeit not always in the most sensible ways, but even with those rules in place, progress on bringing intangible assets onto balance sheets has been slow. To be frank, I don't think accounting rule writers will be able to handle intangibles in a sensible way, and the barriers lie not in rules or models, but in the accounting mindset. Accounting is backward-looking and rule-driven, making it ill equipped to value intangibles, where you have no choice, but to be forward looking, and principle-driven.

The Intrinsic Value of Intangibles

I have been teaching and writing about valuation for close to four decades now, and I have often been accused of giving short shrift to intangible assets, because I don't have a session dedicated to valuing intangibles, in my valuation class, and I don't have entire books, or even chapters of my books, on the topic. While it may seem like I am in denial, given how much value companies derive from assets you cannot see, I have never felt the need to create new models, or even modify existing models, to bring in intangibles. In this section, I will explain why and make the argument that if you do intrinsic valuation right, intangibles should be, with imagination and very little modification of existing models, already in your intrinsic value.

To understand intrinsic value, it is worth starting with the simple equation that animates the estimation of value, for an asset with n years of cash flows:

Thus, the intrinsic value of an asset is the present value of the expected cash flows on it, over its lifetime. When valuing a business, where cash flows could last for much longer (perhaps even forever), this equation can be adapted:

In this equation, for anything, tangible or not, has to show up in either the expected cash flows or in the risk (and the resulting discount rate); that is my "IT" proposition. This proposition has stood me in good stead, in assessing the effect on value of just about everything, from macro variables like inflation to buzzwords like ESG.

Using this framework for assessing intangible assets, from brand name to quality management, you can see that their effect on value has to come from either higher expected cash flows or lower risk (discount rates).To provide more structure to this discussion, I reframe the value equation in terms of inputs that valuation analysts should be familiar with - revenue growth, operating margins and reinvestment, driving cash flows, and equity and debt risk, determining discount rates and failure risk.

In the picture, I have highlight some of the key intangibles and which inputs are mostly likely to be affected by their presence.

It is the operating margin where brand name, and the associated pricing power, is likely have its biggest effect, though it can have secondary effects on revenue growth and even the cost of capital.

Good management, another highly touted intangible, will manifest in a business being able to deliver higher revenue growth, but also show up in margins and reinvestment; the essence of superior management is being able to find growth, when it is scarce, while maintaining profitability and not reinvesting too much.

Connections to governments and regulators, an intangible that is seldom made explicit, can affect value by reducing failure risk and the cost of debt, while increasing growth and or profitability, as the company gets favorable treatment on bids for contracts.

This is not a comprehensive list, but the framework applies to any intangible that you believe may have an effect on value. This approach to intangibles also allows you to separate valuable intangibles from wannabe intangibles, with the latter, no matter how widely sold, having little or no effect on value. Thus, a company that claims that it has a valuable brand name, while delivering operating margins well below the industry average, really does not, and the effect of ESG on value, no matter what its advocates claim, is non-existent.

It is true that this approach to valuing intangibles works best for a company with a single intangible, whether it be brand name or customer loyalty, where the effect is isolated to one of the value drivers. It becomes more difficult to use for companies, like Apple, with multiple intangibles (brand name, styling, operating system, user platform). While you can still value Apple in the aggregate, breaking out how much of that value comes from each of the intangibles will be difficult, but as an investor, why does it matter?

The Birkenstock IPO: A Footwear company with intangibles

If you have found this discussion of intangibles abstract, I don't blame you, and I will try to remedy that by applying my intrinsic value framework to value Birkenstock, just ahead of its initial public offering. As a company with multiple intangible components in its story, it is well suited to the exercise, and I will try to not only estimate the value of the company with the intangibles incorporated into the numbers, but also break down the value of each of its intangibles.

The Lead In

Birkenstock is primarily a footwear company, and to get perspective on growth, profitability and reinvestment in the sector, I looked at all publicly traded footwear companies across the globe. the table below summarizes key valuation metrics for the 86 listed footwear companies that were listed as of September 2023.

In the aggregate, the metrics for footwear companies are indicative of an unattractive business, with more than half the listed companies seeing revenues shrink in the decade, leading into 2022 and more than quarter reporting operating losses. However, many of these companies are small companies, with a median revenue at $170 million, struggling to stay afloat in a competitive product market. Since Birkenstock generated revenues of $1.4 billion in the twelve months leading into its initial public offering, with an expectation of more growth in the future, I zeroed in on the twelve largest companies in the apparel and footwear sector, in market capitalization, and looked at their operating metrics:

As you can see, these companies look very different from the sector aggregates, with solid revenue growth (median compounded growth rate of 8.66% a year, for the last decade) and exceptional operating margins (gross margins close to 70% and operating margins of 24%). Each of the companies also has a recognizable or many recognizable brand names, with LVMH and Hermes topping the list. In this business, at least, brand name seems to be dividing line between success and mediocrity, and having a well-recognized brand name contributes to growth and profitability. It is this grouping that I will draw on more, as I look valuing Birkenstock.

Birkenstock's History

In my work on corporate life cycles, I talk about how companies age, and how importance it is that they act accordingly. Generally, as a company moves across the life cycle, revenue growth eases, margins level off and there is less reinvestment. As a business that has been around for almost 250 years, Birkenstock should be a mature or even old company, but it has found a new lease on life in the last decade.

Birkenstock was founded in 1774 by Johann Adam Birkenstock, a Germany cobbler, and it stayed a family business for much of its life. In the decades following its founding, the company modified and adapted its footwear offerings, catering to wealthy Europeans in the growing German spa culture in the 1800s, and modifying its product line, adding flexible insoles in 1896 and pioneering arch supports in 1902. During the 1920s and 1930s, the company carved out a market around comfort and foot care, partnering with physicians and podiatrists, offering solutions for customers with foot pain. In 1963, the company introduced its first fitness sandal, the Madrid, and sandals now represent the heart of Birkenstock's product line.

Along the way, serendipity played a role in the company's expansion. In 1966, a Californian named Margot Fraser, when visiting her native Germany, discovered that Birkenstocks helped her tired and hurting feet, and she convinced Karl Birkenstock to try selling the company's sandals in California. It is said that Karl advanced her credit, and helped her persuade reluctant California retailers to carry the company’s unconventional footwear in their stores. That proved timely, since people protesting against the war and society's ills latched on to these sandals, making them them symbolic footwear for the rebellious. in the 1990s, the brand had a rebirth, when a very young Kate Moss wore it for a cover story, and it became a hot brand, especially on college campuses. Today, Birkenstock gets more than 50% of its revenues in the United States, with multiple celebrities among its customers. The company's prospectus does a good job painting a picture of both the product offerings and customer base, leading into the IPO, and I have captured those statistics in the picture below:

Unlike some in its designer and brand name peers, the company’s products are not exorbitantly over priced and the company’s best seller, the Arizona, sells for close to $100. While the company sells more shoes to women than men, it sells footwear to a surprisingly diverse customer base, in terms of income, with 20% of its sales coming from customers who earn less than $50,000 a year, and in terms of age, with almost 40% of its revenues coming from Gen X and Gen Z members.

For much of its history, Birkenstock was run as a family business, capital constrained and with limited growth ambitions, perhaps explaining its long life. The turning point for the company, to get to its current form, occurred in 2012, when the family, facing internal strife, turned control of the company over to outside managers, choosing Markus Bensberg, a company veteran, and Oliver Reichert, a consultant, as co-CEOs of the company. Reichert, in particular, was a controversial pick since he was not only an outsider, but one with little experience in the shoe business, but the choice proved to be inspired. With an assist again from serendipity, when Phoebe Philo exhibited a black mink-lined Arizona on a Paris catwalk in 2012, leading to collaborations with high-end designers like Dior, the company has found a new life as a growth company, with revenues rising from €200 million in 2012 to more than €1.4 billion in the twelve months leading into the IPO, representing an 18.2% compounded annual growth rate over the decade:

The surge in revenues has been particularly pronounced since 2020, the COVID year, with different theories on why the pandemic increased demand for the product; one is that people working from home chose the comfort of Birkenstocks over uncomfortable work shoes. The company's growth has come with solid profitability, and the table below shows key profit metrics over the last three years:

Note that the company's operating and gross margins, at least in the last two years, match up well with the operating margins of the large, brand name apparel & footwear companies that we highlighted in the last section. It may be early to value brand name, but the company certainly has been delivering margins that put it in the brand name group.

The strong growth since 2020 provide a strong basis for why the company is planning its public offering now, but there is another factor that may explain the timing. In 2021, the family sold a majority stake in the firm to L. Catterton, an LVMH-backed private equity firm, at an estimated value in excess of €4 billion Euros. That deal was funded substantially with debt, leaving a debt overhang of close to €2 billion, in 2023; the prospectus states that all of of the company's proceeds from the offering will be used to pay down this debt. That said, the pricing for the offering has increased since news of it was first floated in July, with €6 billion plus pricing in initial reports increasing to €8 billion in early September and to €9.2 billion in the most recent news stories. The company has picked up anchor investors along the way, with the Norwegian sovereign fund planning to buy €300 million of the initial offering.

Birkenstock's Intangibles

Birkenstock is a good vehicle for identifying and valuing intangibles, since it has so many of them, with some more sustainable and more valuable than others:

Brand Name: It is undeniable that Birkenstock not only has a brand name, in terms of recognition and visibility, but has the pricing power and operating margins to back up that brand name. However, as is often the case, the building blocks that gave rise to the brand name are complex and varied. The first is the uniqueness of the footwear makes the company stand out, with people people either hating its offerings (ugly, clunky, clog) or loving it. Unlike many footwear companies that attempt to copy the hottest styles, Birkenstock marches to its own drummer. The second is that the company's focus on comfort and foot health, in designing footwear, as well as the use of quality ingredients, is matched by actions. In fact, one reason that the company makes almost all of its shoes still in Germany, rather than offshoring or outsourcing, is to preserve quality, and sticks with time-tested and quality ingredients, is to preserve this reputation. The third is that unlike some of the companies on the big brand name list, Birkenstock's are not exorbitantly over priced, and has a diverse (in terms of income and age) customer base. In short, its brand name seems to have held up well over the generations.

Celebrity Customer Base: As I noted earlier, especially as Birkenstocks entered the US market, they attracted a celebrity clientele, and that has continued through today. Birkenstock attracts celebrities in different age groups, from Gwyneth Paltrow & Heidi Klum to Paris Jackson & Kendall Jenner, and more impressively, it does so without paying them sponsorship fees. If the best advertising is unsolicited, Birkenstock clearly has mastered the game.

Good Management: I tend be skeptical about claims of management genius, having discovered that even the most highly regarded CEOs come with blind spots, but Birkenstock seems to have struck gold with Oliver Reichert. Not only has he steered the company towards high growth, but he has done so without upsetting the balance that lies behind its brand name. In fact, while Birkenstock has entered into collaborative arrangements with other high profile brand names like Dior and Manolo Blank, Reichert has also turned down lucrative offers to collaborate with designers that he feels undermine Birkenstock's image.

The Barbie Buzz: For a company that has benefited from serendipitous events, from Margot Fraser's introduction of its footwear to Americans in 1966 to Phoebe Philo's sandals on the Paris catwalk in 2012, the most serendipitous event, at least in terms of its IPO, may have been the release of the Barbie movie, this summer. Margot Robbie's pink Birkenstock sandals in that movie, which has been the blockbuster hit of the year, hyper charged the demand for the company's footwear. It is true that buzzes fade, but not before they create a revenue bump and perhaps even increase the customer base for the long term.

For the moment, these intangibles are qualitative and fuzzy, but in the next section, I will try to bring them into my valuation inputs.

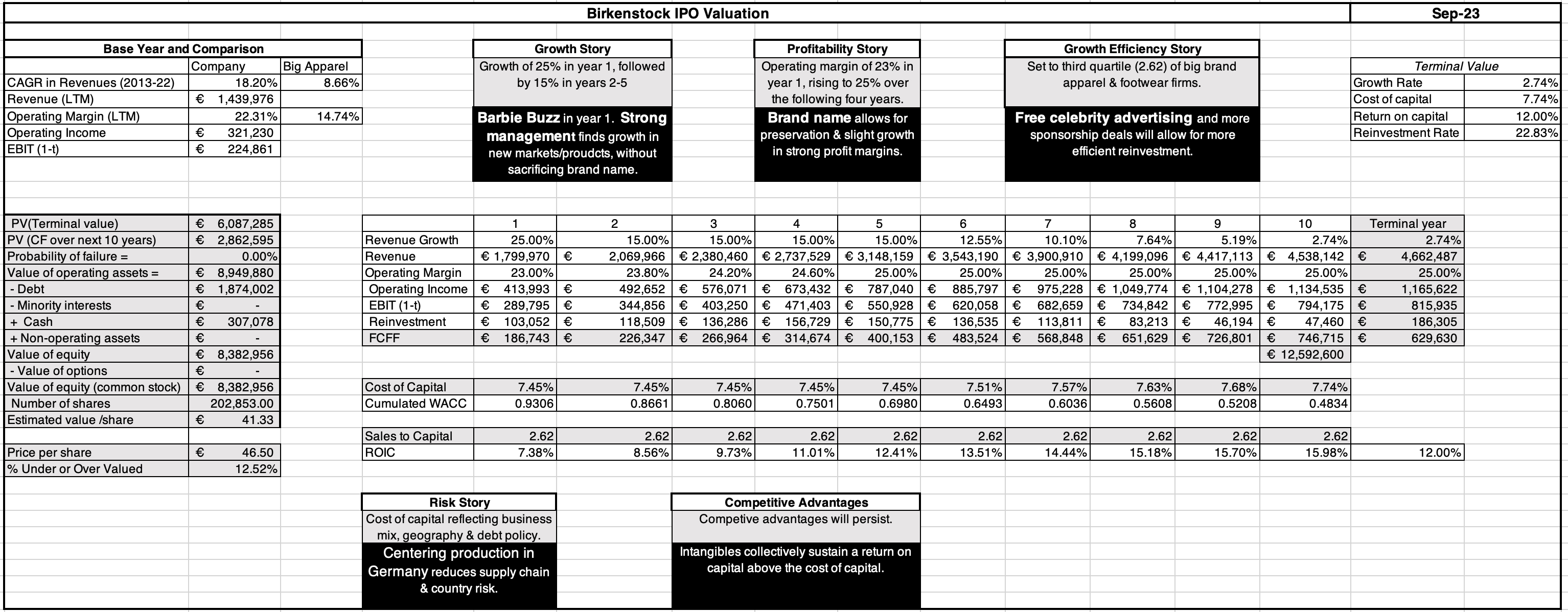

Birkenstock Valuation

My Birkenstock valuation is built around an upbeat story of continued high growth and sustained operating margins, with the details below:

Revenue Growth: The company is coming into the IPO, with the wind at its back, having delivered a compounded annual growth rate of 18.2% in revenues in the decade leading into the offering. That said, its revenues now are €1.4 billion, rather than the €200 million they were in 2012, and growth rates will come down to reflect the larger scale. While the average CAGR in revenues for big brand apparel & footwear firms has been 8.66%, I believe that Oliver Reichert and the management team that runs Birkenstock will continue their successful history of opportunistic growth, and be able to triple revenues over the next decade. This will be accomplished with an assist from the Barbie Buzz in year 1 (pushing the growth rate to 25% over the next year) and a compounded growth rate of 15% a year in the following four years.

Profitability: Birkenstock has had a history of strong operating margins, driven by its brand name and visibility. In the twelve months leading into the IPO, the company reported a pre-tax operating margin of 22.3%, and its margins over the last decade have hovered around 20%. I believe that the strength of the brand name will sustain and perhaps even slightly increase operating margins for the company, with the margin increasing to 23%, over the next year, and to 25% over the following four years.

Reinvestment: Birkenstock has been circumspect in investing for growth, over its history, showing reluctance to move away from its reliance on its German workforce, and in making acquisitions. It has also not been a big spender on brand advertising, using its celebrity clientele as a key component of building and growing its brand I believe that the celebrity clientele effect will allow the company to continue on its path of efficient growth, delivering €2.62 for every euro invested, matching the third quartile of big brand apparel firms.

Risk: The Catterton acquisition of a majority stake in Birkenstock in 2021 was funded with a significant amount of debt, but the proceeds from the offering are expected to be utilized in paying down debt. The company should emerge from the offering with a debt load on par with other brand name apparel & footwear companies, and the concentration of its production in Germany will reduce exposure to supply chain and country risk.

IPO Proceeds: News stories suggest that Birkenstock is planning to offer about 21.5 million shares to the public, and use the proceeds (estimated to be €1 billion, at the €45 offering price) to pay down debt. In conjunction, Catterton plans to sell about the same number of shares at the offering as well, reducing its stake in the company, and cashing out on what should be a big win for the private equity player.

To see how these inputs play out in value, I have brought them together in the (dense) valuation picture below. With each of the inputs, I have highlighted both the numbers that I am using, as well as highlighting how much intangibles contribute to each input:

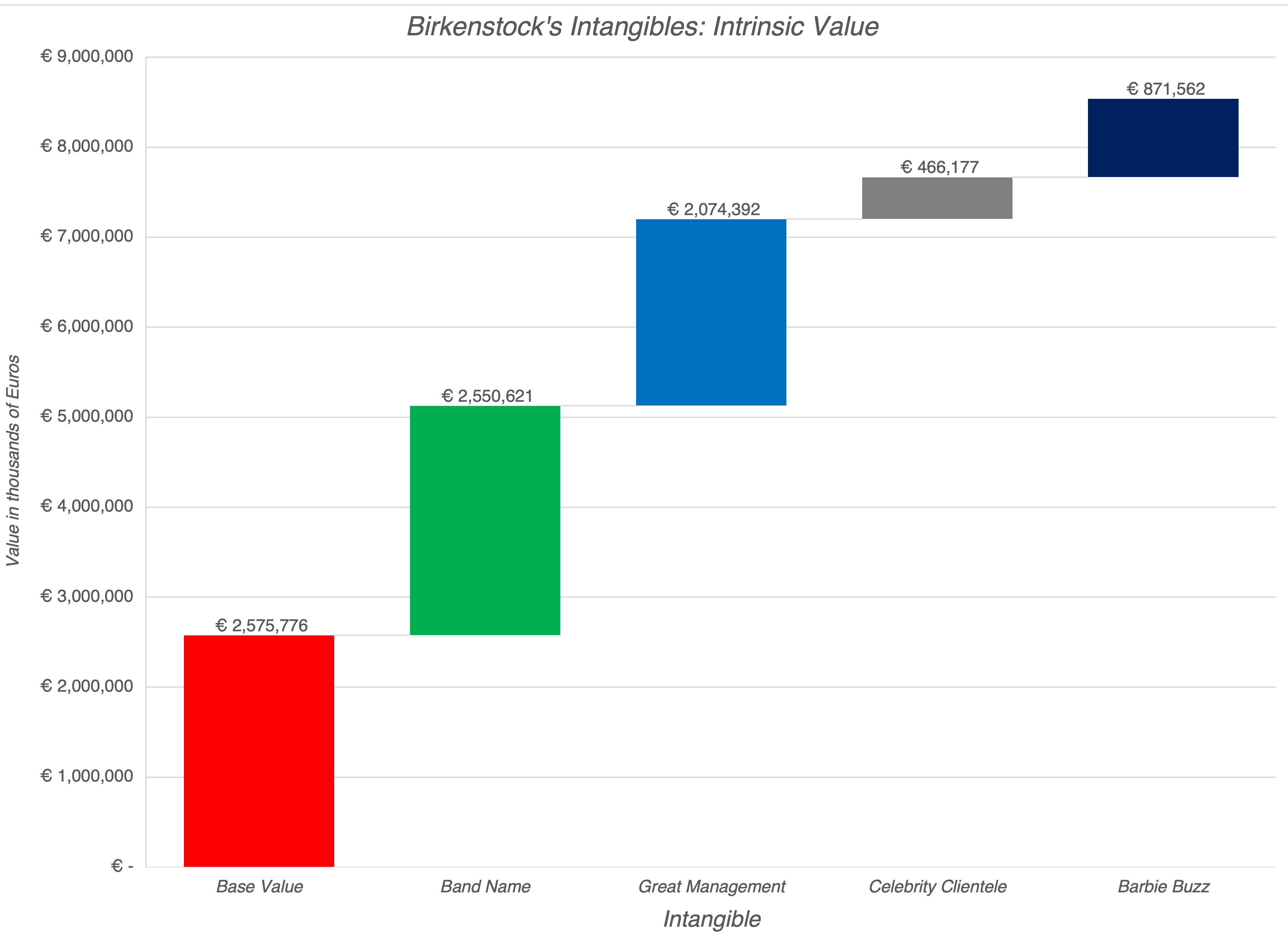

The value that I estimate for Birkenstock, with my inputs on growth, profitability and risk, is about €8.38 billion, about 10% less than the rumored offering pricing, but still well within shouting distance of that number. In case you are tempted to use the company's many intangibles as the explanation for the difference, note that I have already incorporated them into my inputs and value. To make explicit that effect, I have isolated each intangible and its effect on value in the table below:

To value each intangible, I toggle the input that reflects the intangible on and off to determine how much it changes value. The intangible that has the biggest effect on value is brand name, followed by the strength of the management team, with the Barbie Buzz and Celebrity Effects lagging. Another way of visualizing how these intangibles play into value is to build up to estimated value of equity of €8.38 billion in pieces:

These value judgments are based upon my estimates, and they are, of course, open for debate. For instance, you might argue that the effect of good management on revenue growth is more or less than my estimate, or even that the effects spill over into other inputs (cost of capital, margins and reinvestment), but that is a healthy debate to have.

Pricing Factors

It is undeniable that the Birkenstock IPO will be priced, not valued, and the question of how the stock will do is just as much dependent, perhaps more so, on market mood and momentum, as it is on the fundamentals highlighted in the valuation.

Looking at news about the company, the timing works well, since the company is coming into the market on a wave of good publicity. Almost every news story that I have read about the company paints a positive picture of it, with laudatory mentions of Oliver Reichert and the company's products, intermixed with pictures of not only Barbie's pink Birkenstock but a host of other celebrities.

It is the market mood that is working against the company, at least at the moment that I am writing this post (October 6, 2023). As I wrote in my post on bipolar markets just a few days ago, the market mood has soured, with the optimism that we had dodged the bullet that was so widely prevalent just a few weeks ago replaced with the pessimism that dark days lie ahead for the global economy and markets.

At its offering pricing of €9.2 billion (€45 to €50 per share), the company and its bankers seem to be betting that the good vibes about the company will outweigh the bad vibes in the market, but that is gamble. As someone who has tried and rejected the Arizona sandal, I am unlikely to be a customer for Birkenstock footwear, but this is a company with a truly unique brand name and a management team that understands the delicate balance between utilizing a brand name well and overdoing it. It is, in my view, a reach at €45 or €50 per share, but if the market turns sour, and the stock drops to below €40, I would be a buyer.