It was just over two weeks ago that I started my posts on the FANG stocks, starting with Facebook, which I decided to buy, because I felt that notwithstanding its current pariah status, its user base was too valuable to pass by, at the prevailing market price. I then looked at Netflix, a company that has shown a remarkable ability to adapt to the challenges thrown at it, while changing the entertainment business, but is, at least in my view, in a content cost/user cycle that will be difficult to break out of. With Alphabet, the cash cow that is its advertising business is allowing it to invest in the big new markets of tomorrow, and even with low odds and very little substance today, these bets can make or break the investment. That leaves me with the longest listed and perhaps the most intriguing of the four stocks, Amazon, a company whose reach seems to expand into new markets each year.

Revisiting my Amazon past

I valued Amazon for the first time in 1998, as an online book retailer, and much of what I know about valuing young companies today came from the struggles I went through, modifying what I knew in conventional valuation, for the special challenges of valuing a company with no history, no financials and no peer group. Out of that experience was born a paper on valuing young companies, which is still on my website and the first edition of the Dark Side of Valuation, and if you want to see some horrendously wrong forecasts, at least in hindsight, you can check out my valuation of Amazon in that edition.

I valued Amazon for the first time in 1998, as an online book retailer, and much of what I know about valuing young companies today came from the struggles I went through, modifying what I knew in conventional valuation, for the special challenges of valuing a company with no history, no financials and no peer group. Out of that experience was born a paper on valuing young companies, which is still on my website and the first edition of the Dark Side of Valuation, and if you want to see some horrendously wrong forecasts, at least in hindsight, you can check out my valuation of Amazon in that edition.

While I had a tough time justifying Amazon’s valuation, in its dot-com days, I always admired the company and the way it was managed. When I was put off balance by an Amazon product, service or corporate announcement, I re-read Jeff Bezos’ letter to Amazon shareholders from 1997, because it helped me understand (though not always agree with) how Amazon views the business world. In that letter, Bezos laid out what I called the Field of Dreams story, telling his stockholders that if Amazon built it (revenues), they (the profits and cash flows) would come. In all my years looking at companies, I have never seen a CEO stay so true to a narrative and act as consistently as Amazon has, and it is, in my view, the biggest reason for its market success.

I have valued Amazon about once a year every year over its existence, and I have bought Amazon four times and sold it four times in that period. That said, there are two confessions that I have to make. The first is that I have not owned Amazon since 2012, and have thus missed out on its bull run since then. Second, through all of this time, I have consistently under estimated not only the innovative genius of this company, but also its (and its investors') patience. In fact, there have been occasions when I have wondered, staying true to my Field of Dreams theme, whether Shoeless Joe would ever make his appearance.

Amazon’s Market Cap Rise

Amazon’s rise in market capitalization has had more ups and downs than either Google or Facebook, but it has been just as impressive, partly because the company came back from a near death experience after the dot-com bust in 2001.

The more remarkable feature of Amazon’s rise has been the debris it has left in its wake, first with brick and mortar retail in the United States, but more recently in almost every business it has entered, from grocery retail to logistics. These graphs, excerpted from a New York Times article earlier this year, tells the story:

I know that this picture is probably is too compressed for you to read, but suffice to say that no company, no matter how large or established it is is safe, when Amazon enters it's market. Thus, while you can explain away the implosion of Blue Apron, when Amazon entered the meal delivery business, by pointing to its small size and lack of capital, note that the decline in market value at Kroger, Walmart and Target on the date of the Whole Foods acquisition was vastly greater in dollar value terms, and these firms are large and well capitalized. It is also worth noting that the decline in market cap is not permanent and that firms in some of the sectors see a bounce back in the subsequent time periods but generally not to pre-Amazon entry levels. If Amazon represents the light side of disruption, the destruction of the status quo and everything associated with it, in the businesses that it enters, is the dark side.

Amazon: Operating History and Model

Rather than provide an involved explanation for why I call Amazon a Field of Dreams company, I will begin with a chart of Amazon's revenues and operating income that will explain it far more succinctly and better:

1. Amazon Retail/Media

3. Amazon Prime

Investment Judgment

Amazon has clearly delivered on revenue growth, as its revenues have gone from $1.6 billion in 1999 to $177 billion in 2017, but its margins, after an initial improvement, went through an extended period of decline. In most companies, this would be viewed as a sign of a weak business model, but in the case of Amazon, it is a feature of how they do business, not a bug. In effect, Amazon has extended its revenue growth by expanding into new businesses, often selling its products (Kindle, Fire, Prime) at or below cost. That, by itself, is not unique to Amazon, but what makes it different is that it has been able to get the market to go along with its "if we build it, they will come" strategy.

The mild uptick in profitability in the last three years has been fueled by Amazon's web services (AWS) business, offering cloud and other internet related services to other businesses, and that can be seen in the graph below, showing revenues and operating profits broken down by segment:

|

| Amazon 10K |

Over the last five years. AWS has accounted for an increasing slice of revenues for Amazon, but it is still small, accounting for 10% of all revenues in 2017. On operating income, though, it has had a much bigger impact, accounting for all of Amazon's profitability in 2017, with AWS generating $4,331 million in operating profits and the rest of Amazon, reporting an operating loss of $225 million.

To back up my earlier claim that Amazon's low profits are by design, and not an accident, let's look at two expenses that Amazon has incurred over this period that are treated as operating expenses, and are reducing operating profit for the company, but are clearly designed as investments for the future. The first is in technology and content, which include the investments in technology that are driving the growth in the AWS business and content, for the media business. The second is in net shipping costs, the difference between what Amazon collects in shipping fees from its customers and what it pays out, which can be viewed as the investment is making in building up Amazon Prime.

|

| Amazon 10K |

Not only are the technology/content and net shipping costs a large portion of overall expenses, amounting to 18.32% of revenues in 2017, but they have increased over time. The operating margin for Amazon would have been over 20%, if it had not incurred these expenditures, but with those higher, the company would have had far less revenues, no AWS business and no Amazon Prime today. To value Amazon today, I think it makes sense to break it up into at least three parts, with the first being its retail/media business globally, the second its AWS business and finally, Amazon Prime. In the table below, I attempt to deconstruct Amazon's numbers to estimate how much each of these arms is generated as revenues and created in operating expenses in 2017, as a prelude to valuing them.

Note that I had to make some estimates and judgment calls in allocating revenues to Amazon Prime, where I have counted only the incremental revenues from Amazon Prime members, and in allocating content costs. For Amazon Prime, for instance, I have used an assumption that Prime members spend $600 more than non-Prime members, to estimate incremental revenues, and added the $9.7 billion in subscription premiums that Amazon reported in 2017. The net shipping costs have been fully allocated to Amazon Prime and all of the operating expenses that Amazon reported for AWS are assumed to be technology and content. The remaining expenses are allocated across AWS and Amazon Retail/Media, in proportion to their revenues. In my judgment, both Amazon Retail/Media and AWS generated operating profits in 2017, but the latter was much more profitable, with a pre-tax operating margin of 24.81%. Amazon Prime was a money loser in 2017, but its margins are less negative than they used to be, and at 100 million members, it may be poised to turn the corner.

Amazon Business Model

If there are any secrets in Amazon's business model, they are dispensed when you read Amazon's 10K, which is remarkably forthcoming about how the company approaches business. In particular, the company emphasizes three key elements in its business model:

- Focus on Free Cash Flow: I tend to be cynical when companies talk about free cash flows, since most use self serving definitions, where they add "stuff" to earnings to make their cash flows look more positive. Amazon does not seem to take the same tack. In fact, it not only nets out capital expenditures and working capital needs, as it should, but it even nets out acquisitions (such as the $13.2 billion it spent on Whole Foods) to get to free cash flow.

- Manage working capital investment: Perhaps remembering times as a start-up when mismanaging inventory brought it to its knees, the company is focused on keeping its investment in working capital as low as possible, though that does sometimes involve strong arming suppliers.

- Use Operating leverage: Amazon is clearly conscious about its cost structure, recognizing that its revenue growth can give it significant advantages of economies of scale, when it comes to fixed costs.

There are two additional features to the company that I would add, from my years observing the company.

- Patience: I have never seen a company show as much patience with its investments as Amazon has, and while there are some who would argue that this is because of it's large size and access to capital, Amazon was willing to wait for long periods, even when it was a small company, facing a capital crunch. I believe that patience is embedded in the company's DNA and that the Bezos letter in 1997 explains why.

- Experimentation: In almost every business that Amazon enters, it has been willing to try new things to shake up the status quo, and to abandon experiments that do not work in favor of experiments that do.

There is no scarier vision for a company than news that Amazon has entered its business. If you are in that besieged company, how do you survive the Amazon onslaught? We know what does not work:

- Imitation: You cannot out-Amazon Amazon, by trying to sell below cost and wait patiently. Even if you are a company with deep pockets, Amazon can out-wait you, since it is not only how they do business and they have investors who have accepted them on their terms.

- Cost Cutting: There are companies, especially in the US brick and mortar retail space, that thought they could cut costs, sell products at Amazon-level prices and survive. By doing so, they speeded their decline, since the poorer service and limited inventory that followed alienated their core customers, who left them for Amazon.

- Whining: Companies under the Amazon threat often resort to whining not only about fairness (and how Amazon breaks the rules) but also about how society overall will pay a price for Amazon domination. There are seeds of truth in both argument, but they will neither slow nor stop Amazon from continuing to put them out of business.

While there is no one template for what works, here are some strategies, drawn from looking at companies that have survived Amazon, that improve your odds:

- Tilt the game: You can try to get governments and regulators to buy into your warnings of monopoly power and societal demise and to regulate or restrict Amazon in ways that allow you to continue in business.

- Play to your strengths: If you have succeeded as a company before Amazon came into your business, you had competitive advantages and core customers who generated that success. Nourishing your competitive advantages and bringing your core customers even closer to you is key to survival, but that will require that you live through some financial pain (in the form of higher costs).

- And to Amazon's weaknesses: Amazon's favored markets have high growth and low capital intensity, and when they get drawn into markets that demand more capital investment, like logistics, it is because they were forced into them. If you can move the terrain to lower growth, higher capital intensity businesses, you can improve your odds of surviving Amazon.

None of these choices will guarantee success or even survival, and there are times where you may have to seek partnerships and joint ventures to make it through, and if all else fails, you can try some witchcraft.

Valuing Amazon

In my prior iterations, I tried to value Amazon as a consolidated company, arguing that it was predominantly a retail company with some media businesses. The growth of AWS and the substantial spending on Amazon Prime has led me to conclude that a more prudent path is to value Amazon in pieces, with Amazon Retail/Media, AWS and Amazon Prime, each considered separately.

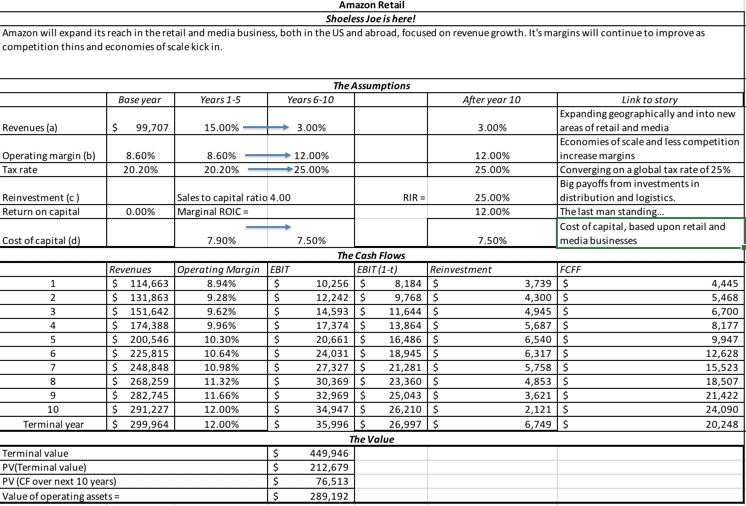

1. Amazon Retail/Media

To value the heart of Amazon, which still remains its retail and media business, I used the revenues and operating margin that I estimated based upon my allocation at the end of the last section as my starting point, and assumed that Amazon will be able to continue growing revenues at 15% a year for the next five years, while also improving its operating margin (currently 9.09%, with technology and content costs capitalized) to 12%. The revenue growth assumption is built on Amazon's track record of being able to grow and the improved margin reflect expected economies of scale. The resulting value is shown below:

|

| Download spreadsheet |

Based upon my assumptions, the value that I attach to the retail/media business is about $289 billion. The key driver of value is the operating margin improvement, built into the story.

2. AWS

If Amazon's reported numbers are right, this division is the profit machine for the company, generating an operating margin of close to 25%, while revenues grew 42.88% in 2017. While I believe that this business will stay high growth and profitable, it is also one where Amazon faces strong competitors in Microsoft and Google, just to name two, and both revenue growth rates and margins will come under pressure. I assume revenue growth of 25% a year for the next 5 years, with operating margin declining to 20% over that period. The value is shown below:

|

| Download spreadsheet |

The value that I estimate for AWS is about $139 billion. The key for value creation is finding a mix of revenue growth and operating margin that keeps value up, since going for higher growth with much lower margins will cause value to dissipate.

3. Amazon Prime

To value Amazon Prime, I use the same technique that I used last year to value it, starting with a value of a Prime member, and building up to the value of Prime, by forecasting growth in Prime membership and corporate costs (mostly content). I updated the Prime membership number to 100 million (from the 85 million that I used last August) and used the 2017 financial statements to get more specific on both content costs and on the cost of capital. The value is shown below:

|

| Download spreadsheet |

Based upon the layers of assumptions that I have made, especially on shipping costs growing at a rate lower than membership rolls, the value that I estimate for Amazon Prime is about $73 billion. The key input here is shipping costs, since failing to keep it in control will cause the value to very quickly spiral down to zero.

Amazon, the Company

With all three pieces completed, I bring them together in my valuation of the company, incorporating the total debt outstanding in the company of $42,730 (including capitalized operating leases) and cash of $30.986 million, to arrive at a value per share of $1019.

At $1,460/share, on April 25, the stock is clearly out of my reach right now. Given that I have not been able to justify buying the stock at any time in the last five years, as it rose from $250/share to $1500, my suggestion is that you do you don't take my word, and that you make your own judgment. You can download the spreadsheets that I have for Amazon Retail/Media, AWS and Amazon Prime at the end of this post, and change those assumptions of mine that you think are wrong.

Investment Judgment

The FANG stocks represent great companies, but of the four, I think that Amazon has the most fearsome business model, simply because its platform of disruption and patience can be extended to almost any other business, one reason why every company should view Amazon as a potential competitor. I know that the old value adage is that if you buy quality companies and hold them forever, they will pay for themselves, but I don't believe that! There are good companies that can be bad investments and bad companies that can be terrific investments, as I noted in this post. Amazon has fallen into the first category for much of the last five years and continues to do so, at today's market price. But good things come to those who wait, and I know that there be a time and a price at which it will be back in my portfolio.

Post-post Update: I deliberately posted this before the earnings report, and the report that came out about two hours after the post was a blockbuster, with higher revenue growth than expect, a doubling of net income and an increase in the stock price of close to $100/share in the after market. Incorporating the effects into the valuations will have to wait until the full quarterly report is available, but the biggest part of the report, for me, was the increase in Prime Membership fees to $119/year. You can modify the Amazon Prime valuation spreadsheet to reflect the increase in membership feels to $119/year (from $99/year). Doing so increases the value of Prime to almost $116 billion, increasing value per share by almost $100/share.

Post-post Update: I deliberately posted this before the earnings report, and the report that came out about two hours after the post was a blockbuster, with higher revenue growth than expect, a doubling of net income and an increase in the stock price of close to $100/share in the after market. Incorporating the effects into the valuations will have to wait until the full quarterly report is available, but the biggest part of the report, for me, was the increase in Prime Membership fees to $119/year. You can modify the Amazon Prime valuation spreadsheet to reflect the increase in membership feels to $119/year (from $99/year). Doing so increases the value of Prime to almost $116 billion, increasing value per share by almost $100/share.

YouTube Video

Data Links

Related Blog Posts

Blog Posts on Tech Takedown

2 comments:

Dear Professor,

I always look forward to your Blogs. However, when it comes to Amazon, I do believe your assumptions are incorrect. Here are my cents:

First, the breakdown is inaccurate, a better breakdown would be: AWS, Advertising, Physical Stores, Subscriptions & Online Sales. Online Sales have to be split into 1P and 3P or third party making GMV much higher than Rev.

Please checkout Amazon seller referral fees and other fees at https://services.amazon.com/selling/pricing.html

Many of these fees drop straight to profit.

I would love to hear your feedback.

First, a great write up. Some thoughts though.

1) Amazon has more debt than you have considered. See Note 6 to 10k which has capital and finance lease commitments of $8.4 b and $4.7 b respectively. These are in addition to capitalization of operating leases.

2) You have not capitalized its advertising costs, any reason? Last year it spent $6.3 b on that.

2) Do you reckon Amazon will be able to sustain 12% as perpetual operating margin on its retail business?

3) Without taking any credit from Bezos, Amazon has been one lucky business, for no other business has been given such a long time by the market to sort of show positive cash flows. I am not sure whether it will be able to bring itself to generate consistent, sufficient cash flows to justify the market price in future as well. It will continue to have very high capex and acquisitions in the coming years too which means significant free cash flows will have to wait, and wait. It spent $11 b in capex last year, and $14 in acquisitions. It will probably have more acquisitions once in say, 3 years.

It's a great business though, but a terrible investment on value terms. Heck, investors have always been able to make money despite that.

4) Not sure whether net shipping costs are to be taken as investment for future. They are so unlike advertising and R&D costs. It is a tough call.

5) If expected rate of return is 7.9% leading to 7.5%, I think S&P-500 index should be able to deliver that including dividends. Why bet on a single business?

6) Amazon as a business has been tricking investors. Its only business that is making real money is AWS and has decent growth potential to generate free cash flows. Why mix this unrelated business with retail? Spin it off and then let's see how markets will price Amazon retail. Note 11 segment information shows assets employed on each business. Although not the best allocation, it shows how much AWS is making on capital, and how long its international business has to go.

7) Finally, Amazon's best bet is international operations. It failed in China. It is looking for something different in India. With Walmart trying to team up with Flipkart, it will be interesting to see the fight. Amazon will have to spend billions in that market.

I think you have said it correctly, it is actually a field of dreams, of perpetual dreams. And only dreamers have been able to make money out of it. I cannot dream that far enough, for I have to actually see the cash rolling in before I can think of taking a piece of that field.

Thanks for the post.

Post a Comment