In my last two posts, I looked first at measures of country risk, both from a default risk and an equity market perspective, and then at stock pricing, using earnings and book value multiples, across developed and emerging markets. In summary, the conclusion that I drew was that the shift away from emerging markets in the last six months may be obscuring a much larger shift towards convergence between emerging and developed markets over the last decade. Thus, we can debate whether this convergence is rational or overdone, but it is quite clear that stock markets around the world have more in common now than they are different. Having said this, it is worth noting that the developed and emerging market categories that I used in the last post, which were based on geographic location, may no longer reflect the reality that there is vastly more diversity within each region than there used to be. In this post, I intend to look at the pricing of stocks, by country, not only to illustrate this diversity but also to look for mis pricing, at a country level, around the globe.

PE Ratios around the globe

The price earnings ratio, notwithstanding its volatility and measurement weaknesses, remains among the most widely used tools in investing. In fact, some global investors still compare PE ratios across countries and often direct their money towards countries with low PE ratios, on the presumption that this must indicate "cheapness".

To put this approach into practice, I first computed PE ratios in June 2013, by country. During the computation, I noted a couple of phenomena, which while unsurprising, are still worth emphasizing. The first is that almost 60% of all companies globally have negative earnings and PE ratios are thus not meaningful for these companies. The second is that there are significant outliers, with a few companies with exceptionally high PE ratios (usually because earnings have dropped to close to zero) pulling the averages to high numbers, especially in countries with relatively few companies. To get a more representative value, I computed the PE ratio based on aggregate values for market capitalization and net income. Put simply, I summed up the market capitalization of all the companies in a market and divided by the total net income of all companies in a market. This aggregate value is not as sensitive to outliers and reflects more closely a weighted average of the companies in the market, with values representing the weights.

The heat map below allows you to compare PE ratios across countries, and within regions.

Note that the countries with the lowest PE ratios (in yellow and orange) are also among the world's riskiest (a large swath of Africa, Venezuela (Latin America) and Eastern Europe). Put differently, these countries look cheap, but they have good reasons to be cheap. The bulk of developed markets have PE ratios between 10 and 15, with the weighted PE ratio at 10.49 for Germany, 12.81 for Japan and 14.27 for the US. Surprisingly, Mexico and Chile have the highest weighted PE ratios, with Mexico at 18.04 and Chile at 18.64. There are also large sections of the world where PE ratios cannot be computed, either because earnings information is not available or because earnings are negative.

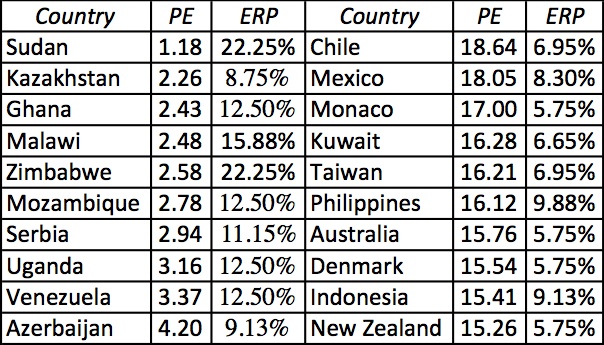

If most of the low PE countries are high risk and the bulk of the high PE countries are low risk, we have to use more finesse in looking for cheap and expensive markets. In fact, a cheap market would offer a combination of a low PE and low risk and an expensive market would be one with high PE and high risk. To look for those mismatches, I combined the PE ratio dataset with the equity risk premiums estimated in the prior blog post and generated a list of the ten countries with the highest and lowest PE ratios, with accompanying equity risk premiums.

Of the ten countries with the lowest PE ratios, only two (Kazakhstan and Azerbaijan) had equity risk premiums less than 10% and I cam not tempted to invest in either country (given their dependence on commodity prices and political risk profiles). There are more interesting countries on the highest PE list, though a couple reflect commodity price volatility; the drop in copper prices, for instance, has hit Chilean company earnings harder than it has market capitalizations.

Price to Book Ratios

The price to book ratio is often a less volatile and more reliable measure of pricing in a market. While accounting choices can affect book value, the effects of these choices are more muted than on earnings. As with PE ratios, I computed both the average price to book ratios and price to book ratios based upon aggregate market capitalization and book equity and decided to use the latter as the indicator of overall pricing. The map below provides comparisons of the aggregate price to book ratio across the globe:

Unlike PE ratios, there seems to be little relationship between the dispersion of price to book ratios across the globe and country risk. Some of the highest price to book ratios are in the riskiest countries: Namibia, Indonesia and Venezuela all have price to book ratios that exceed 2.50 and are all high risk countries.

As with PE ratios, a naive strategy of directing your money to the countries with the lowest price to book ratios may be dangerous, since these low multiples of book value can be explained by low returns on equity. The following is a list of the ten countries with the highest and lowest price to book ratios:

Note that the countries with the highest price to book ratios also tend to have very high returns on equity, whereas some of the countries on the lowest price to book ratios have negative or low returns on equity. There are some mismatches, especially on the low PBV list, with Zimbabwe, Lebanon and Russia joining Kazakhstan and Azerbaijan as markets with low price to book ratios and high returns on equity. In addition to all the caveats about hidden (and not so hidden) risks, it is also worth noting that some of these markets have only a handful of listings and no or low liquidity.

Enterprise Value to EBITDA multiples

Some investors and analysts take issue with equity multiples, arguing that they do not account for overall value and leverage. Consequently, I estimated enterprise value to EBITDA multiples for individual countries, using both simple averages and aggregated values. The resulting global map of EV to EBITDA multiples is below:

This map more closely corresponds to the PE map, with riskier countries having lower EV to EBITDA multiples (with Mongolia being an exception). The median value across the globe is 8.03, with the United States (8.45), Australia (8.59), India (9.48) and China (9.99) trading above the value and much of Western Europe trading below.

Just as I balanced PE ratios against risk and PBV against ROE, I brought in return on invested capital (ROIC) into the comparison of EV/EBITDA multiples, on the assumption that higher ROIC is more likely to accompany higher EV/EBITDA multiples. Again, the list of countries with the highest and lowest EV/EBITDA multiples, with ROIC for each, is in the list below:

Unlike with equity multiples, the relationship between ROIC and EV/EBITDA is in the inverse of expectations, with countries with the higher (lower) returns on invested capital having the lowest (highest) EV/EBITDA multiples.

Wrapping up

At the end of the comparisons of equity and enterprise value multiples, I must confess that I feel little inclination to make abrupt asset allocation judgments based upon any of these multiples. It is true that some markets seem to offer better risk and return trade offs than others, but these markets seem to come with warning labels (about political or commodity price risk). It is also possible that I am missing some hidden patterns here and you are welcome to download the dataset containing my estimates of both average and aggregate values, by country.

Notwithstanding the noise in the numbers, I am glad that I was able to look at the numbers across countries. I feel a little more informed about how stocks are being priced across the globe and how investors are pricing in the most extraordinary and unusual risks in some markets. I also realize how much I have left to learn about how stocks are priced in countries with non-traditional risks and will keep working at filling in the gaps in my knowledge.

- Rediscovering risk in emerging markets: A country risk premium update

- Developed versus Emerging Markets: Convergence or Divergence?

- Market Multiples: Global Comparison and Analysis

- Global Businesses and Country Risk: Investment Challenges and Opportunities (Still to come)

29 comments:

Really enjoyed an insightful and well laid out piece of research. Keep up the stellar work and look forward to further musings

Good post Professor. I was wondering if you could post an update on your valuation of AAPL and the impact of their share repurchase program on its value.

Great post! It would be interesting to look at EVA for the same sample of markets. In such a volatile environment it would be interesting to see who is actually covering their costs. A good way to look at things, don't you think?

Thank you Professor!

I did a similar analysis a few years ago for a consultancy.

My key conclusion was that equity markets in individual countries are so biased by their sector coverage, it is difficult to make any meaningful comparison comparing equity markets like this.

E.g. most of Russian stocks are oil or natural resource-based. Therefore it makes no sense to compare PEs and ROICs to those of the NASDAQ.

Perhaps a sectoral comparison would be more valuable - the tech sector in London vs tech sector in China; the retail sector in Chile vs retail on NYSE.

etc etc

There is no doubt this is a very valuable analyze but i can not pass thru before i asking you some questions. For example, i am really interested to know how did you get to the values for Romanian market. Other way said, i would like to know which are those 400 companies that are on the base of your analyze (i have a couple of doubts regarding the market capitalization value that you work with). I would really appreciate an answer. Best regards.

Very interesting & insightful article on global stock market scenario, was wondering and if you could explain how did you arrive at those numbers and analysis of indian stock market?

This is good for the international market trders, and very useful to all traders.......

Equity-tips

Yet another insightful post on global markets, Thanks professor!

Great post professor, a very informative post on global markets. Just what I needed!

Hey Professor, I was wondering why it's the case that EV/EBITDA and ROIC have an inverse relationship.

It is really nice and very useful to all visitor....

stock-tips

Great post.Thank you professor.

Nice post & this is very useful information about price comparison

this is very useful and informatic.....

commodity tips

Dear Prof.,

I was wondering if you could add a column of interest payments for the countries in the worksheet with raw country data. High EV/Ebitda can imply high valuation by investors, but also high book value of debt vis a vis market value of equity (distress). I was trying to estimate market value of debt of the countries.

I think that I need coupon payments (interest expense), yield and avg. maturity of debt to approximate its market value. I can estimate the yield by the credit spread of the country from your country spread file (country credit rating minus 2 or 3 ratings to reflect average corporate, lets say). Lets say that I assume duration as 3 years. If I have interest expense, Market Value of debt can be estimated. I want to calculate EV with Market Value of debt and then see its relation with RoIC, ROE, etc.

Also, in the sheet with raw country data if I calculate latest Book Value of Debt as EV - Mar Cap (column z - column y), it comes to be substantially lower than the value of debt mentioned for CY 2012 (column v) for almost all the countries. I am not sure if I am reading it right.

Thank you very much for the post.

Hello Professor,

Was going through your valuation sheets on apple and i have a query. What do you mean by Revenues against country/region which is dispayed on the sheet 'Cost of capital worksheet' against every country/region. Would really appreciate you taking your time off to answer my query.

You can do spreadsheets but you have no understanding of how stock market works and how investors value companies.

Partially because you lack the imagination and forward thinking required to spot successful companies of future today, Which is what investing and markets are all about. Discounting the future.

You are limited to spreadsheets and number crunching which almost anyone can do.

Stick to teaching. They don't fire bad teachers.

Great post!

Wow! Your new truck is perfect for a family get away and amazing adventures! I bet you can drive it on a highway or even in a very rocky road with ease because of its body lift! I always dreamt of owning a truck because I love traveling, and it has every space that I need for my luggage. :D Have a great trip!

sanpete county tax lien sales auction

tax forclousures auctions

neuce county texas tax liens

What is the source of your data?

Very special article

Many human benefit from these threads and specifically about medicine

I will continue to search for other topics on this site to achieve Interest

Thanks to those in charge of the site

Surely, This website is a informative and fundamental website about financial market . I like your website very surely. Many many thanks for published this website. If you want more informastion about stock charts to visit stock charts a majority of these supply you with a lot more advice about program not to mention challenge ranges, as well as allows you to tweak the tends to buy, provides, not to mention stop-losses. Post look at about three frequent choice methods not to mention his or her common graph and or chart timeframes.

It feels like I’ve come across this blog before on but immediately after browsing at some of the material I figured out that it’s new to me.

Still, I’m gonna bookmark this blog and begin coming here regularly.

review jual sepatu | ulasan jual sepatu online | jual sepatu online | jual sepatu murah online | rekomen jual sepatu | rekomendasi toko sepatu | jual sepatu terbaik | review jual sepatu online | jual sepatu online | jual rumah pekanbaru | jual toko pekanbaru | sewa apartement pekanbaru | jual tanah pekanbaru | sewa kos pekanbaru | hotel murah di jakarta | madu hutan | jual sepatu adidas | jual sepatu vans | jual sepatu new balance

I have enjoyed reading your articles. It is well written. It looks like you spend a large amount of time and effort in writing the blog. I am appreciating your effort. You can visit my website

Stock market response analysis

Good, this is a good post. nhac cho funring

WiseGuyReports.com: The leading provider of market research reports, Market forecast and industry analysis on products, markets and companies worldwide. Sample Report:

Post a Comment