In my last post on Uber, I noted that it was burning through cash and that this cash burn, by itself, is neither unexpected nor a bad sign. Since I got quite a few comments on what I said, I decided to make this post just about the causes and consequences of cash burn. In the process, I hope to dispel two myths held on opposite ends of the investing spectrum, the notion on the part of value investors, that a high cash burn signals a death spiral for a business and the equally strongly held belief, at the start-up investing end , that a cash burn is a sign of growth and vitality.

Cash Burn: The what?

Since it is cash burn, not earnings burn, that concerns us, let’s start with the obvious. It is cash flow, not earnings, that is at the heart of a cash burn problem. While many money losing companies have cash burn problems, not all cash burn problems are money losing, and not all money losing companies have a cash burn problem. To understand cash burn, you have to start with a working definition of cash flows and my definition hews closely to what I use in the context of valuing businesses. The free cash flow to the firm is the cash left over after taxes have been paid and reinvestment needs (to maintain existing assets and generate future growth) have been met:

Since it is cash burn, not earnings burn, that concerns us, let’s start with the obvious. It is cash flow, not earnings, that is at the heart of a cash burn problem. While many money losing companies have cash burn problems, not all cash burn problems are money losing, and not all money losing companies have a cash burn problem. To understand cash burn, you have to start with a working definition of cash flows and my definition hews closely to what I use in the context of valuing businesses. The free cash flow to the firm is the cash left over after taxes have been paid and reinvestment needs (to maintain existing assets and generate future growth) have been met:

For mature, going concerns, the after-tax operating income and free cash flow to the firm will be positive (at least on average) and that cash flow is used to service debt payments as well as to provide cash flows to equity in the form of dividends and stock buybacks. Any remaining cash flow, after debt payments and dividends/buybacks, augments the cash balance of the company.

But what if the free cash flow to the firm is negative? That can happen either because a company has operating losses or because it has large reinvestment needs or both occur in tandem. If you have negative free cash flow to the firm, you can draw down an existing cash balance to cover that need and if that turns out to be insufficient, you will have to raise fresh capital, either in the form of new debt or new equity. If this negative cash flow is occasional and is interspersed with positive cash flows in other years, as is often the case with cyclical or commodity companies, you consider it to be a reflection of normal operations of the firm and it should cause few issues in valuation. If, on the other hand, a business has negative cash flows year in and year out, it is said to be burning through cash or having a “cash burn” problem.

To measure the magnitude of the cash spending problem, analysts use a variety of measures. One is to compute the dollar cash spent in a time period, usually a month, and that is termed the Cash Burn rate. Another is to compute the Cash Runway, the time period that it will take for a company to run through its existing cash balance. Thus, a firm with a $1 billion cash balance and a negative cash flow of -$500 million a year has a 2-year Cash Runway. In contrast, another company with a $1 billion cash balance and a negative cash flow of -$ 2 billion a year has only a 6-month Cash Runway.

Cash Burn: The Why?

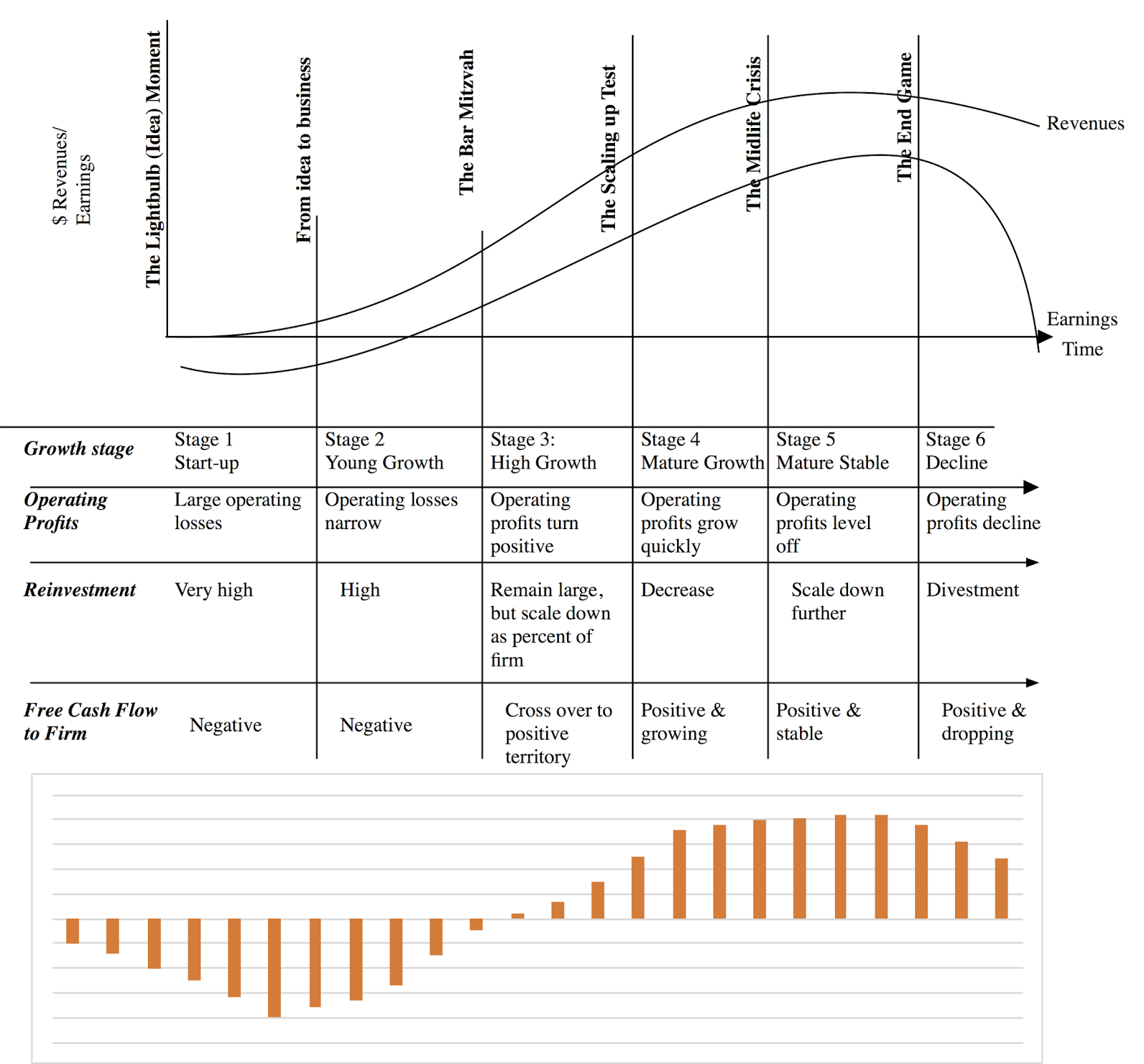

Looking at the definition of cash flows should give you a quick sense of why you get high cash burn values (and ratios) at some companies. If your company is and has been losing money or generating very small earnings for an extended period and it sees high growth potential in the future (and invests accordingly), your cash flows will reflect that reality.

That combination of low operating income/operating losses and high reinvestment is what you should expect to see at many young companies and the resulting negative free cash flow to the firm will be the norm rather than the aberration. As the companies move through the life cycle, the benign perspective on cash burn is that this will cease to be a problem.

As the company scales up, its operating income and margins should increase and as growth starts to scale down (in future years), the reinvestment should start dropping.

As the company scales up, its operating income and margins should increase and as growth starts to scale down (in future years), the reinvestment should start dropping.

Cash Burn: The what next?

The combination of higher operating margins and lower reinvestment should generate a cross over point where cash flows turn positive and these positive cash flow will carry the value. Rather than talking in abstractions, let me use the numbers in my August 2016 Uber valuation to illustrate. The story that I am telling in these numbers is of a going concern and success, with high revenue growth accompanied by improving operating margins as the first leg, followed by declining growth (and reinvestment) converting negative cash flows to positive cash flows in the second leg and a steady state of high earnings and cash flows reflected in a going concern value in the final phase.

The combination of higher operating margins and lower reinvestment should generate a cross over point where cash flows turn positive and these positive cash flow will carry the value. Rather than talking in abstractions, let me use the numbers in my August 2016 Uber valuation to illustrate. The story that I am telling in these numbers is of a going concern and success, with high revenue growth accompanied by improving operating margins as the first leg, followed by declining growth (and reinvestment) converting negative cash flows to positive cash flows in the second leg and a steady state of high earnings and cash flows reflected in a going concern value in the final phase.

The life cycle story that I have laid out is the benign one, where after its start-up pains, a young company turns the corner, starts generating profits and ultimately turns cash flows around. Before you buy into the fairy talk that I have told you, you should consider a more malignant version of this story. In this one, the firm starts off as a growth firm with negative margins and high reinvestment (and cash burn). As the revenues increase over time and the company scales up, the cost structure continues to spiral out-of-control and the margins become more negative over time, rather than less. In fact, with reinvestment creating an additional drain on the cash flows, your free cash flow will be negative for extended and very long time periods and you are on the pathway to venture capital hell. To illustrate what the cash flows would look like in this malignant version of cash burn, I revisited the Uber valuation and changed two numbers. I reduced the operating margin (targeted for year 10) from 20% down to 5% (making ride sharing a commoditized business) and increased reinvestment to match a typical US company (by setting the sales to capital ratio to two, instead of three). The effects on the cash flows are dramatic.

So, when is cash burn likely to be value destructive or fatal? If the company operates in a market place, where competition keeps pushing product prices down and the costs of delivering these products continue to rise, it is already on a course to report bigger and bigger losses, even before considering reinvestment. If this company reinvests for growth and the product market conditions do not change (i.e., price cutting and rising costs are expected to continue), it is likely that the reinvestment will not deliver the earnings required to justify that investment. Here, there is no light at the end of the tunnel, as negative cash flows will generally become more negative over time and even when they do turn positive, will be insufficient to cover the burden of negative cash flows in earlier time periods.

Cash Burn: So what?

Though stories about young companies and their cash burn problems abound, there are few that try to make the connection between cash burn and value other than to point to it as a survival risk. To make the connection more explicit, it is worth thinking about why and how cash burn affects the value of an enterprise.

- Dilution Effect: A company has to raise cash to burn through it and if that cash is raised from fresh equity, as it inevitably has to be for young growth companies, the existing owners of the business will have to give up some of their ownership of the company. If you are an equity investor, the greater the cash burn in a company, the less of the company you will end up owning, even if it survives and prospers.

- Growth Effect: The dilution effect presumes that there are capital providers who will be supply the cash needed to keep the firm going through its cash burn days, but what if that presumption is incorrect? The best case scenario for the firm, when capital dries up, is that it is able to rein in discretionary spending (which will include all reinvestment for growth) until capital becomes available again. In the meantime, though, the company will have to scale back its growth plans.

- Distress Effect: The more dangerous consequence of capital drying up for a young firm with negative free cash flows Is that the firm’s survival is put at risk. This will be the case if the company is unable to meet its operating cash flow needs, even after cutting discretionary capital spending to zero. In this scenario, the firm will have to liquidate itself and given its standing, it will have to settle for a fraction of its value as a going concern.

In intrinsic valuation, both of these effects can and should be captured in your intrinsic value.

- The dilution effect manifests itself as negative cash flows in the early years and a drop in the present value of cash flows. For instance, in my Uber valuation, the present value of the expected cash flows for the first seven years, all negative, is $4.4 billion. While the positive cash flows thereafter more than compensate for this, I am in effect reducing the value of Uber by about 20% for these negative cash flows and this reduction can be viewed as a preemptive discounting of my equity stake in the company for future dilution.

- When I discount the negative cash flows back to today and assume that Uber has no chance of game-ending failure, I am assuming that Uber has and will continue to have access to capital, partly because of its size and partly because existing investors have too much to lose if the company goes into death throes. If you believe these assumptions to be too optimistic, you can adjust the valuation in two ways. The first is by putting a cap on how much new capital the firm can raise each year, which will also operate as a constraint on future growth. The other is by allowing for a probability that the firm will fail, either because capital markets shut down or cash flows are more negative than expected. In my Lyft valuation in September 2015, for instance, I allowed for a 10% probability of this occurring and assumed that equity investors would get close to nothing if it did, effectively reducing my valuation today.

In pricing, how does it show up? In a young company, pricing usually involves forecasting revenues or earnings in a future time period, applying a multiple, at which you believe the company will be priced by a potential buyer or the market in an IPO, to these revenues and pricing and then discounting back that end price to today using a target rate of return.

As you can see, there is no explicit adjustment for cash burn in this equation. While you could bring in the effect of negative cash flows, just as you did in intrinsic valuation, by discounting them back to today and netting out against the pricing, doing that removes one of the biggest reasons why investors and analysts like pricing, which is that it is simple. The only adjustment mechanism left is the target rate of return and, in my view, it becomes the mechanism that venture capitalists and investors use to deal with cash burn concerns. Given that these target rates of return also carry the weight of reflecting failure risk, it should come as no surprise that VC target rates of return for investment look high (at 30%, 40% or even 50%) relative to rates used for established companies.

As you can see, there is no explicit adjustment for cash burn in this equation. While you could bring in the effect of negative cash flows, just as you did in intrinsic valuation, by discounting them back to today and netting out against the pricing, doing that removes one of the biggest reasons why investors and analysts like pricing, which is that it is simple. The only adjustment mechanism left is the target rate of return and, in my view, it becomes the mechanism that venture capitalists and investors use to deal with cash burn concerns. Given that these target rates of return also carry the weight of reflecting failure risk, it should come as no surprise that VC target rates of return for investment look high (at 30%, 40% or even 50%) relative to rates used for established companies.

An Investor Checklist for Cash Burn

If you are an investor in a company, public or private, that is burning through cash, you may be wondering at this point what you would look at to determine whether a company’s cash burn is benign or malignant and whether it is on a glide path to glory or a Hari Kari mission. Here are some things to consider:

- Understand why the company is burning through cash: Looking back at the constituents of free cash flows, there are multiple paths that can lead to negative free cash flows. The most benign scenario is one where a money making company reports negative cash flows because of large reinvestment. Not only is this negative cash flow a down payment for future growth but it is also discretionary, insofar as managers can scale back reinvestment if capital becomes scarce. The most dangerous combination is a money losing company that reinvests very little, since there is little potential for a growth payoff and management will be helpless if capital freezes up.

- Diagnose the operating business: While there is often a lot of noise around the numbers, you still have to make your best judgments about the profitability of the underlying business. In particular, you want to focus on the pricing power that your company has and the economies of scale in its cost structure. The most benign scenario on this dimension is one where the company has significant pricing power and a cost structure that benefits from scale, allowing for margin improvement over time.

- Gauge management skills: Managing a cash-burning company does require management to keep costs under control, while reinvesting to generate growth and to take care of short term cash flow problems, while mapping out a long term strategy. The best case scenario for investors is that the company is run by a management team that works within the cash flow constraints of today while mapping out pathways to profitability over time. The worst case scenario is that the company is managed by those who view negative cash flows as a badge of honor and a sign of growth rather than a temporary problem to overcome.

- Growth/Reinvestment trade off: Since reinvesting for future growth can be a big reason for negative cash flows, to assess the payoff in value terms, you have to both estimate how much growth will be created and its value effect. In its most value-creating form, reinvestment will generate high growth coupled with high returns and its most value-destructive form, reinvestment will drain cash flows while generating low growth and poor profits.

- Capital Market A firm with a cash burn problem is more depending upon capital markets for its survival, since a closing of these markets may be sufficient to put the firm into receivership. It is no surprise, therefore, that cash burning companies that have larger cash balances or more established capital providers are viewed more positively than cash burning companies that have less cash and have less access to capital.

This checklist requires subjective judgments along the way and you will be wrong sometimes, in spite of your best efforts. That should not stop you from trying.

The Bottom Line

If you are an investor in a company that is burning through cash, don't panic! If your investments are in young companies, it is exactly what you should expect to see though you should do your due diligence, examining the reasons for the cash burn in and the soundness of the underlying business model. If you are an old-time value investor, weaned on large dividends, positive cash flows and margin of safety, you may find yourself avoiding companies that have these cash burn problems but be glad that there are investors who are less risk averse than you are and willing to bet on these companies.

YouTube video

Posts on valuing young companies

If you are an investor in a company that is burning through cash, don't panic! If your investments are in young companies, it is exactly what you should expect to see though you should do your due diligence, examining the reasons for the cash burn in and the soundness of the underlying business model. If you are an old-time value investor, weaned on large dividends, positive cash flows and margin of safety, you may find yourself avoiding companies that have these cash burn problems but be glad that there are investors who are less risk averse than you are and willing to bet on these companies.

YouTube video

Posts on valuing young companies

- Blood in the Shark Tank: Pre-money, Post-money and Play-money Valuations

- Billion Dollar Tech Babies: A Blessing of Unicorns or a Parcel of Hogs

- The Bonfire of Venture Capital: The Good, Bad and Ugly Side of Cash Burn

7 comments:

Extremely insightful sir. I believe this technique can also be used to identify whether an established company is about to fail. The negative cash flows would be caused due to an adverse industry scenario (long term shift in industry), or an aggressive investment strategy which does not give sufficient ROI.

Fantastic post! Would have liked for you to expand on the dilution effect. I believe another issue with the "dilution effect" is the diluting effects on earnings. If shares were offered at astronomical valuations; then, a shareholder would welcome new shareholders, as each new issue would generate tangible value. The problem arises when shares are issued at a steep discount, given the relatively early stages of the Company. Thoughts?

Hi Prof. Damodaran, thanks for the very helpful post. Would you treat Biotech start-ups as a special case in any way? There, two fundamental and critical unknowns are the Phase 2/3 results, and prospects for FDA approval / denial. The clinical trial results, in particular, seem to be unpredictable as a general rule. Thank you in advance for any thoughts on this.

Hello Prof.Damodaran, Thank you for the great post. I suppose we also have to consider the potential exit value of the firm. For companies operating in spaces where the value of the talent, IP or the network is very unique, the cash burn may be a wrong metric. Like jet.com for instance where the sale price more than justified the cash burn. My point is that there are some areas where the company may be able to get a good ROI even with high cash burn and low growth.

Uber reportedly lost $1.27 Bn the first half of 2016.

Mr. Damodaran, so you're saying that the future dilution effect is already included with the negative cash flows and one should not divide the company value by the future number of shares to calculate the value per share, but instead should divide the company value by the current number of shares? It seems counterintuitive, and there's very little material about this online; yet value per share is what matters the most (unless it's a whole company M&A transaction).

Regards,

Vit

I believe the analyst should be extremely careful so not to as double count the cash burn situation.

If a company is burning cash I would consider the growth effect and adjust the cost of capital accordingly, which would have a direct effect on FCFF.

Interested as I am in the firm as a going concern, as opposed to its liquidation value, I would likely assess the probability of a cash shortage and that would lead to an estimated cost of capital for future CF, but if I discount further the value of negative CF there's a risk of double dipping on the cash burn situation.

Prof Damodaran rightly mentions that analysts appreciate simplicity but sometimes we must go the extra mile for the sake of trying to be more precise.

Great article.

Post a Comment