On July 21, 2021, I valued Zomato just ahead of its initial public offering at about ₹41 per share. The market clearly had a very different view, as the stock premiered at ₹74 per share and soared into the stratosphere, peaking at ₹169 per share in late 2021. The last few months have been rocky, as the price has been marked down, partly in response to disappointing results from the company, and partly because of macro developments. At close of trading on July 26, 2022, the stock was trading at ₹41.65 per share, and the mood and momentum that worked in its favor for most of 2021 had turned against the company. In this post, I will begin with a quick review of my 2021 valuation, then move on to the price action in 2021 and 2022 and then update my valuation to reflect the company's current numbers.

My IPO Valuation

I valued Zomato, soon after it filed its prospectus for its initial public offering, in July 2021. The details of that valuation are in this post, but to cut a long story short, I argued that an investment on Zomato was a joint bet on India (that economic growth would bring more discretionary income to its people), on Indian eating habits (that Indians would eat out at restaurants more than they have in the past) and on the company (that its business model and first move advantages would give it a dominant market share of the food delivery market). I summarized my valuation in a picture:

I valued the company at close to ₹41, and note that this valuation incorporates the proceeds from the IPO and adjusts the share count for the offering. I argued then that notwithstanding the potential growth in the market, and Zomato's advantageous positioning, it was being over priced for its IPO, at ₹76 per share.

In response to the pushback that I got from those who disagreed with my valuation, with half arguing that I was being way too optimistic about the future and the other half that I was ignoring the potential for growth overseas and in new businesses, I followed up with a second post, where I let readers choose their own story line for Zomato, and came up with a table that linked stories to values:

Using my test of whether a valuation story is possible (the weakest test), plausible (a stronger test) and probable (the acid test), I posited that you could justify a value per share for Zomato of ₹40 - ₹50, per share, with plausible stories, but that valuations that were much higher required pushing the limits of plausible narratives.

The Pricing Game

One reason that I enjoy valuing a company just ahead of its market debut is that there is no market price to bias your analysis; in my experience, the market price operates as magnet, drawing intrinsic valuations towards it. The downside is that without a market price acting as an anchor, your valuations can easily come unmoored from reality. No matter what, having a valuation in hand makes the first day of trading much more interesting, as you wait for the market to pass its own judgment on the stock’s pricing, though that judgment reflects more a pricing game than a value estimate.

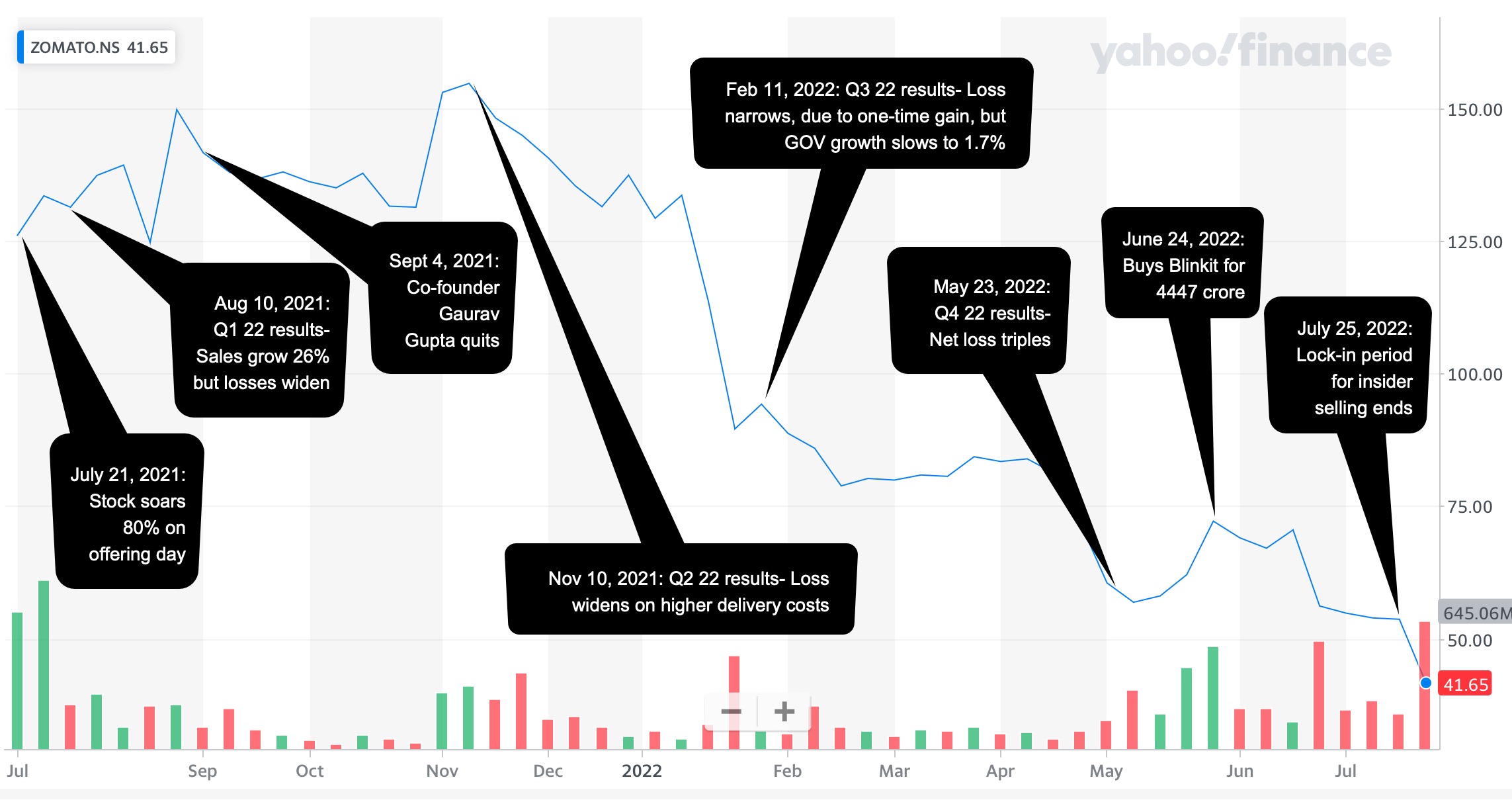

Staying with the theme that it is demand and supply, mood and momentum that determine what happens to a company’s stock in first few months of trading, the buzz that accompanied Zomato’s listing and its standing as one of the first new age Indian companies to go public, spilled over into the first day of trading, as the stock soared 51% over its offering price of ₹76, and rose as high as ₹137 during the trading day. That opening day glow lasted for the rest of 2021, abetted by easy access to risk capital, and the stock maintained its lofty pricing. If you are tempted to attribute the price performance to good news from the company, its earnings reports continued to report escalating losses and one of its co-founders quit in September 2021.

In 2022, though, the company's stock rediscovered the laws of gravity, and news stories that would have elicited positive responses in 2021 are having the opposite effect. The most recent plunge in the stock price seems to have been precipitated by Zomato’s acquisition of Blinkit, a grocery delivery company, for $570 million (₹4400 crores), on June 24, 2022 and the expiration of the lock-in period, allowing insiders to sell shares in the company. At close of trading on July 26, Zomato’s stock price was at ₹41.65 per share.

Updating the fundamentals

Though some have suggested that price dropping to my value is vindication of my valuation, I am not part of that group for three reasons. First, it seems skewed to celebrate only your successes and not your failures, and it behooves me to let you know that I also valued Paytm at close to ₹2000 per share, and the stock is currently trading at ₹713. Second, even if nothing in my valuation has changed, the value per share of ₹41 per share was as of July 2021, and if it is a fair assessment, the expected intrinsic value per share in July 2022 should be roughly 11.5% higher (i.e., grow at the cost of equity), yielding about ₹46 in July 2022. Finally, the company and the market have changed in the year since I last valued it, and to make a fair judgment today, the company will have to be revalued.

Company Fundamentals

In the year since my IPO valuation, there have been four quarterly reports from the company, in addition to news stories about governance and the company's legal challenges, and there is a mix of good and bad news in them.

On the good news front, the food delivery market in India has continued to grow over the last year, and Zomato has been able to maintain its market share. In fact, there are signs that the market is consolidating with Zomato and Swiggy controlling 90% of the market share of restaurant deliveries. As a consequence, Zomato's gross order value and revenues have both jumped over the course of the last year:

In addition, the substantial cash that Zomato raised on its IPO is providing it with a cash and liquidity cushion, with cash and short term investments jumping from ₹15,000 in March 2021 to ₹68746 (including short term investments) in March 2022. Since Zomato is a young, money-losing company, and the likelihood of failure acts as a drag on value, this will benefit the company, since it provides not only a cushion for the firm but also eliminates dependence on external capital for the next few years.

On the bad news front, the take rate, i.e., the slice of gross order value (GOV) that Zomato keeps has dropped substantially over the last year, reflecting increased competition in the market, higher delivery costs and Zomato's entry into newer markets (like grocery delivery) with lower revenue sharing. In addition, the growth has come in fits and starts, and given Zomato's active acquisition strategy, it is not clear how much of the revenue growth is organic and how much is acquired. Not surprisingly, the company's losses have ballooned over the last year:

While there was a management narrative of economies of scale and improved contribution margins, the end numbers don't back up either contention, with cost of goods sold rising much faster than revenues and operating and net margins both becoming more negative over the last year. (And no, you cannot add back stock based compensation and come up with an adjusted EBITDA to claim otherwise....) In addition, the Indian government put both Swiggy and Zomato on notice that they may be facing anti-trust action in the future, perhaps opening the door to more competition.

On the still-to-be-decided front, Zomato has continued on a strategy of acquiring small companies to advance its growth agenda, and while many of these acquisitions have been small, its most recent acquisition of Blinkit has raised questions about whether this growth is coming at a reasonable cost. (Again, the contention from management that this is a capital-light company that growth with little investment is not true, since these acquisitions are its true cap ex, making it a capital intensive firm.) The potential conflicts of interest in this acquisition, with a Zomato co-founder's spouse operating as the CEO of Blinkit, also add to the questions. Even if the Blinkit acquisition pans out, it is an open question whether Zomato can continue to deliver growth effectively and efficiently through this acquisition-driven strategy, using its own shares as currency, especially as it scales up. In addition, Zomato is also building a portfolio of equity positions, which do not show up as part of operating assets, and the founders rationalize this behavior by arguing that these are "the building blocks for a robust quick-commerce business in India, and will accelerate digitisation and growth of the food and restaurant industry which accelerates our core food business " (from the 2022 Q4 shareholder discussion). Even if we accept this argument for minority holdings, it will add to the complexity in the firm and make investors and traders more wary, especially in periods of uncertainty.

The Macro Factors

When I valued Zomato in July 2021, the markets (in India and globally) were in the midst of a boom, with abundant supply of risk capital and optimism about economic growth, pushing up the prices of tech companies, generally, and the youngest, most money-losing tech companies, specifically. Those circumstances no longer hold, with two big developments in global markets, both of which I have talked about in previous posts

Inflation returns: Inflation is back in almost every part of the globe, and has unsettled markets. In this post, from May 2022, I noted that financial assets (stocks, bonds) lose value when inflation is higher than expected, and that a decade of low and stable inflation has left investors exposed and vulnerable. The effects of inflation show up first as higher risk free rates, across currencies, and next in higher risk premiums, with both equity risk premiums and default spreads rising. In a follow-up post a couple of weeks later, I looked inflation's effects on individual companies and argued that less-risky companies with pricing power and high gross margins would be less exposed than riskier, money-losing companies. (I will leave it to you to judge where Zomato falls on this continuum.)

Risk Capital flees: In a post at the start of this month, I looked at how the retreat of risk capital, i.e., capital invested in the riskiest assets (from venture capital invested in start ups to investments in the riskiest collectibles) was playing out in higher equity risk premiums in mature markets, and in a later post a few days later, even bigger increases in equity risk premiums in emerging markets. As a company with the bulk of its business in India, Zomato again is more exposed to these developments.

A higher equity risk premium for India (9.08% in July 2022, compared to 6.85% in July 2021) and a higher riskfree rate in rupees (4.78% in July 2022, compared to 4.25% in July 2021) conspire to push up the cost of capital for Zomato (and other Indian companies) by about 1.5-2% from my IPO valuation.

A Zomato Revaluation

Incorporating the updated financials for Zomato (with the doubling of revenues in conjunction with larger operating losses) and the higher cost of capital, from macro developments, I revalued Zomato on July 26, 2022:

Note that my core story for the company has not changed, but its Blinkit acquisition suggests that Zomato is planning a substantial foray into the grocery delivery business (pushing up the total market size currently and in the future), albeit at the expense of a smaller slice of revenues and a smaller market share. The value per share has dropped from ₹40.79 to ₹35.32 per share, with much of the value change from last year is coming from macroeconomic developments, manifested in a higher cost of capital. For this value to be generated, the company will need to stop paying lip service to contribution margins and adjusted EBITDA, and work on reducing growth in its cost of goods sold.

An Action Plan

So, what now? As with my valuation last year, let me emphasize that this is not the valuation of Zomato, but is my valuation and it will inform my decisions on the company. I have a story for Zomato, and valuation inputs that reflect that story, but I could be wrong on both fronts, and as I did last year, I tried to capture these uncertainties in a Monte Carlo simulation:

Oracle Crystal Ball used for simulations

Allowing for the wide ranges of estimates that you can have on the total market for food (restaurant and grocery) delivery in India in 2032 and the uncertainties about Zomato's share of that market and its operating margins, you get a range of values. The median value of ₹34.12 is close to the base case value of ₹35.32, not surprising since the input distributions were centered on my base case input values, and at its current stock price (₹41.65 on July 26), the stock is still at the 70th percentile. That said a few more weeks like the last two will push the price below my median value, and if it does, I would buy Zomato, as part of a diversified portfolio (and not as a stand alone investment).

If you are a trader, you are playing a different game entirely, and Zomato's value is not part of that game. You are gauging mood and momentum, which at the moment are extremely negative for the stock, and trying to get ahead of a shift back to the positive. To make that judgment, you will be better served poring over charts, looking at price and volume movements, consulting with an astrologer, or even visiting your favored temple, church or mosque.

Conclusion

I know that some of you did buy Zomato shares in their glory days in 2021 and are either continuing to hold, hoping for a come back, or have sold, and are licking your wounds. I am sorry for your loss, but please don't attribute to conspiracies (where insiders, founders and backers play the role of villains) what can be better explained by greed, and its capacity to cloud judgment. No matter how tempted you are to blame the financial news, journalists, equity research analysts and others for your decision to buy Zomato at its heights, that decision was ultimate yours and the first step in becoming a good investor is taking ownership of your decisions. Put bluntly, if you live by momentum, you die by it. Your consolation prize is that you have lots of company in this market (from Cathie Wood at Ark to the thousands of investors who put their money in Bitcoin, NFTs and other cryptos), and this too shall pass!

There are three topics that you can write or talk about that are almost guaranteed to draw a audience, stocks (because greed drives us all), sex (no reason needed) and salvation. I am not an expert on the latter two, and I am not sure that I have that much that is original to say about the first. That said, in my niche, which is valuation, many start with the presumption that almost every topic you pick is boring. Obviously, I do not believe that, but there are some topics in valuation that are tough to care about, unless they are connected to real events or current news. One issue that I have always wanted to write about is the potential for a feedback loop between price and value (I can see you already rolling your eyes, and getting ready to move on..), but with the frenzy around GameStop and AMC, you may find it interesting. Specifically, a key question that many investors, traders and interested observers have been asking is whether a company, whose stock price and business is beleaguered, can take advantage of a soaring stock price to not just pull itself out of trouble, but make itself a more valuable firm. In other words, can there be a feedback loop, where increasing stock prices can pull value up, and conversely, could decreasing prices push value down?

Price, Value and the Gap

For the third time in three posts, I am going to fall back on my divide between value and price. Value, as I have argued is a function of cash flows, growth and risk, reflecting the quality of a company's business model. Price is determined by demand and supply, where, in addition to, or perhaps even overwhelming, fundamentals, you have mood, momentum and revenge (at least in the case of GameStop) thrown into the mix. Since the two processes are driven by different forces, there is no guarantee that the two will yield the same number for an investment or a company at a point in time:

Put simply, you can have the price be greater than value (over valued), less than value (under valued) or roughly the same (fairly valued). The last scenario is the one where markets are reasonably efficient, and in that scenario, the two processes do not leak into each other. In terms of specifics, when a stock's value is roughly equal to its price:

Issuing new shares at the market price will have no effect on the value per share or the price per share, dilution bogeyman notwithstanding.

Buying back shares at the market price will have no effect on the value per share or price per share of the remaining shares, even though the earnings per share may increase as a result of decreased share count.

I know these implications sound unbelievable, especially since we have been told over and over that these actions have consequences for investors, and so much analysis is built around assessments of accretion and dilution, with the former being viewed as an unalloyed good and latter as bad.

The Feedback Loop

In the real world, there are very few people who believe in absolute market efficiency, with even the strongest proponents of the idea accepting the fact that price can deviate from value for some or many companies. When this happens, and there is a gap between price and value, there is the potential for a feedback loop, where a company's pricing can affects its value. That loop can be either a virtuous one (where strong pricing for a company can push up its value) or a vicious one (where weak pricing for a company can push down value). There are three levels at which a gap between value and price can feed back into value:

Perception: While nothing fundamentally has changed in the company, a rise (fall) in its stock price, makes bondholders/lenders more willing to slacken (tighten) constraints on the firm and increase (decrease) the chances of debt being renegotiated. It also affects the company's capacity to attract or repel new employees, with higher stock prices making a company a more attractive destination (especially with stock-based compensation thrown into the mix) and lower stock prices having the opposite effect.

Implicit effects: When a company's stock price goes up or down, there can be tangible changes to the company's fundamentals. If a company has a significant amount of debt that is weighing it down, creating distress risk, and some of it is convertible, a surge in the stock price can result in debt being converted to equity on favorable terms (fewer shares being issued in return) and reduce default risk. Conversely, if the stock price drops, the conversion option in convertible debt will melt away, making it almost all debt, and pushing up debt as a percent of value. A surge or drop in stock prices can also affect a company's capacity to retain existing employees, especially when those employees have received large portions of their compensation in equity (options or restricted stock) in prior years. If stock prices rise (fall), both options and restricted stock will gain (lose) in value, and these employees are more (less) likely to stay on to collect on the proceeds.

Explicit effects: If a company's stock price rises well above value, companies will be drawn to issue new shares at that price. While I will point out some of the limits of this strategy below, the logic is simple. Issuing shares at the higher price will bring in cash into the company and it will augment overall value per share, even though that augmentation is coming purely from the increase in cash. Companies can use the cash proceeds to pay down debt (reducing the distress likelihood) or even to change their business models, investing in new models or acquiring them. If a company's stock price falls below value, a different set of incentives kick in. If that company buys back shares at that stock price, the value per share of the remaining shares will increase. To do this, though, the company will need cash, which may require divestitures and shrinking the business model, not a bad outcome if the business has become a bad one.

I have summarized all of these effects in the table below:

These effects will play out in different inputs into valuation, with the reduction in distress risk showing up in lower costs for debt and failure probabilities, the capacity to hire new and keep existing employees in higher operating margin, the issuance or buyback of shares in cash balances and changes in the parameters of the business model (growth, profitability). Looking at the explicit effect of being able to issue shares in the over valued company or buy back shares in the under valued one, there are limits that constrain their use:

Regulations and legal restrictions: A share issuance by a company that is already public is a secondary offering, and while it is less involved than a primary offering (IPO), there are still regulatory requirements that take time and require SEC approval. Specifically, a company planning a secondary offering has to file a prospectus (S-3), listing out risks that the company faces, how many shares it plans to issue and what it plans to use the proceeds for. That process is not as time consuming or as arduous as it used to be, but it is not instantaneous; put simply, a company that sees its stock price go up 10-fold in a day won't be able to issue shares the next day.

Demand, supply and momentum: If the price is set by demand and supply, increasing the supply of shares will cause price to drop, but the effect is much more insidious. To the extent that the demand for an over valued stock is driven by mood and momentum, the very act of issuing shares can alter momentum, magnifying the downward pressure on stock prices. Put simply, a company that sees it stock price quadruple that then rushes a stock issuance to the market may find that the act of issuing the shares, unless pre-planned, May itself cause the price rise to unravel.

Value transfer, not value creation: Even if you get past the regulatory and demand/supply obstacles, and are able to issue the shares at the high price, it is important that you not operate under the delusion that you have created value in that stock issuance. The increase in value per share that you get comes from a value transfer, from the shareholders who buy the newly issued shares at too high a price to the existing shareholders in the company.

Cash and trust: If you can live with the value transfer, there is one final hurdle. The new stock issuance will leave the company with a substantial cash balance, and if the company's business model is broken, there is a very real danger that managers, rather than follow finding productive ways to fix the model, will waste the cash trying to reinvent themselves.

With buybacks, the benefits of buying shares back at below value are much touted, and Warren Buffett made this precept an explicit part of the Berkshire Hathaway buyback program, but buybacks face their own constraints. A large buyback may require a tender offer, with all of the costs and restrictions that come with them, the act of buying back stock may push the price up and beyond value. The value transfer in buybacks, if they occur at below fair value, also benefit existing shareholders, but the losers will be those shareholders who sold their shares back. Finally, a buyback funded with cash that a company could have used on productive investment opportunities is lost value for the company.

Reality Check

With that long lead in, we can address the question that many of those most upbeat about GameStop and AMC were asking last week. Can the largely successful effort, at least so far, in pushing up stock prices actually make GameStop or AMC a more valuable company? The answer is nuanced and it depends on the company:

Perception: For the moment, the rise in the stock price has bought breathing room in both companies, as lenders back off, but that effect is likely to be transient. Perception alone cannot drive up value.

Implicit effects: On this dimension, AMC has already derived tangible benefits, as $600 million in convertible debt will become equity, making the company far less distressed. For those Redditors primed for revenge against Wall Street, it is worth noting that the biggest beneficiary in this conversion is Silver Lake, a hedge fund that invested in these bonds in the dark days for the company. GameStop's debt is more conventional borrowing, and while bond prices have gone up, the benefits don't accrue as directly to the company.

Explicit effects: On this dimension again, AMC is better positioned, having already filed a prospectus for a secondary offering on December 11, well ahead of the stock run-up. In that offering, AMC filed for approval for issuance of up to 178 million additional shares, from time to time, primarily to pay down debt. If the stock price stays elevated, and that is a big if, AMC will be able to issue shares at a price > value and increase its value per share. It is unclear whether GameStop has the time to even try to do this, especially if the stock price rise dissipates in days or weeks, rather than months.

To incorporate the feedback loop, I had modified my base case GameStop valuation (not the best case that you saw in my last post), and allowed for two additional inputs: new shares issued and an issuance price. Note that the value per share that I get with no additional shares issued is $28.17, and you can see how that value per share changes, for different combinations of issuance share numbers and issuance share prices:

Note that if the issuance occurs at my estimate of intrinsic value of $28.17, the share issuance has no effect on value per share, since the increase in share count offsets the increased cash balance exactly. Even in the more upbeat scenarios, where the company is able to issue new shares at a price above this value, let's be clear that the game that is playing out is value transfer. To see this, take the most extreme scenario, where GameStop is able to issue 50 million new shares (increasing their share count from 65.1 million to 115.1 million) at a stock price of $200, viable perhaps on Friday (when the stock traded about $300) but not today, the value effect and transfer can be seen below:

The value transfer can be intuitively explained. If new shareholders pay well above value, that increment accrues to existing shareholders. Since the new shareholders are buying the shares voluntarily, you may be at peace with this transfer, but if these new shareholders are small individual investors drawn in by the frenzy, the entire notion of this price run-up being a blow for fairness and justice is undercut.

Investing Endgames!

The anger and sense of unfairness that animated many of those who were on the buying end of GameStop and AMC last week has roots in real grievances, especially among those who came of age in the midst or after the 2008 crisis. I understand that, but investing with the intent of hurting another group, no matter how merited you think that punishment is, has two problems. The first is that markets are fluid, with the winners and losers from an investing episode representing a quickly shifting coalition, The people who are helped and hurt are not always the people that you set out to help or hurt. The second is that if you truly want to punish a group that you think is deserving of punishment, you have to find a way to do damage to their investment models. Hurting some hedge funds, say the short sellers in GameStop, while helping others, like Silver Lake, will only cause investors in these funds to move their money from losing funds to winning funds. Thus, the best revenge you can have on funds is to see investors collectively pull their money out of funds, and that will happen if they under perform as a group.

I generally try to stay out of fights, especially when they become mud-wrestling contests, but the battle between the hedge funds and Reddit investors just too juicy to ignore. As you undoubtedly know, the last few days have been filled with news stories of how small investors, brought together on online forums, have not only pushed up the stock prices of the stocks that they have targeted (GameStop, AMC, BB etc.), but in the process, driven some of the hedge funds that have sold short on these companies to edge of oblivion. The story resonates because it has all of the elements of a David versus Goliath battle, and given the low esteem that many hold Wall Street in, it has led to sideline cheerleading. Of course, as with everything in life, this story has also acquired political undertones, as populists on all sides, have found a new cause. I don't have an axe to grind in this fight, since I don't own GameStop or care much about hedge funds, but I am interested in how this episode will affect overall markets and whether I need to change the ways in which I invest and trade.

Short Sales and Squeezes

I know that you want to get to the GameStop story quickly, but at the risk of boring or perhaps even insulting you, I want to lay the groundwork by talking about the mechanics of a short sale as well as how short sellers can sometimes get squeezed. When most of look at investing, we think of stocks that we believe (based upon research, instinct or innuendo) will go up in value and buying those stocks; in investing parlance, if you do this, you have a "long" position. For those of you tempted to put all of Wall Street into one basket, it is worth noting that the biggest segment of professional money management still remains the mutual fund business, and mutual funds are almost all restricted to long only positions. But what if you think a stock is too highly priced and is likely to go down? If you already own the stock, you can sell it, but if you don't have a position in the stock and want to monetize your pessimistic point of view, you can borrow shares in the stock and sell them, with an obligation to return the shares at a unspecified point in time in the future. This is a “short” sale, and if you are right and the stock price drops, you can buy the shares at the now "discounted" price, return them to the original owner and keep the difference as your profit.

Short sellers have never been popular in markets, and that dislike is widely spread, not just among small investors, but also among corporate CEOs, and many institutional investors. In fact, this dislike shows up not only in restrictions on short selling in some markets, but outright bans in others, especially during periods of turmoil. I don't believe that there is anything inherently immoral about being a pessimist on markets, and that short selling serves a purpose in well-functioning markets, as a counter balance to relentless and sometimes baseless optimism. In fact, mathematically, all that you do in a short sale, relative to a conventional investment, is reverse the sequence of your actions, selling first and buying back later.

It is true that short sellers face a problem that their long counterparts generally do not, and that is they have far less control over their time horizons. While you may be able to sell short on a very liquid, widely traded stock for a longer period, on most stocks, your short sale comes with a clock that is ticking from the moment you initiate your short sale. Consequently, short sellers often try to speed the process along, going public with their reasons for why the stock is destined to fall, and they sometimes step over the line, orchestrating concerted attempts to create panic selling. While short sellers wait for the correction, they face multiple threats, some coming from shifts in fundamentals (the company reporting better earnings than expected or getting a cash infusion) and some from investors with a contrary view on the stock, buying the stock and pushing the stock price up. Since short sellers have potentially unlimited losses, these stock price increases may force them to buy back shares in the market to cover their short position, in the process pushing prices up even more. In a short squeeze, this cycle speeds up to the point that short sellers have no choice but to exit the position.

Short squeezes have a long history on Wall Street. In 1862, Cornelius Vanderbilt squeezed out short sellers in Harlem Railroad, and used his power to gain full control of the New York railroad business. During the 20th century, short sales ebbed and flowed over the decades, but lest you fall into the trap of believing that this is a purely US phenomenon, the short sale with the largest dollar consequences was the one on Volkswagen in 2008, when Porsche bought enough shares in Volkswagen to squeeze short sellers in the stock, and briefly made Volkswagen the highest market cap company in the world. Until this decade, though, most short squeezes were initiated and carried through by large investors on the other side of short sellers, with enough resources to force capitulation. In the last ten years, the game has changed, for a number of reasons that I will talk about later in this post, but the company where this changed dynamic has played out most effectively has been Tesla. In the last decade, Tesla has been at the center of a tussle between two polarized groups, one that believes that the stock is a scam and worth nothing, and the other that is convinced that this is the next multi-trillion dollar company. Those divergent viewpoints have led to the former to sell short on the stock, making Tesla one of the most widely shorted stocks of all time, and the latter buying on dips. There have been at least three and perhaps as many as five short squeezes on Tesla, with the most recent one occurring at the start of 2020. With Tesla, individual investors who adore the company have been at the front lines in squeezing short sellers, but they have had help from institutional investors who are also either true believers in the company, or are too greedy not to jump on the bandwagon.

The Story (so far)

This story is still evolving, but the best way to see it is to pick one company, GameStop, and see how it became the center of a feeding frenzy. Note that much of what I say about GameStop could be said about AMC and BB, two other companies targeted in the most recent frenzy.

A Brief History

GameStop is a familiar presence in many malls in the United States, selling computer gaming equipment and games, and it built a business model around the growth of the gaming business. That business model ran into a wall a few years ago, as online retailing and gaming pulled its mostly young customers away, causing growth to stagnate and margins to drop, as you can see in this graph of the company’s operating history:

Leading into 2020, the company was already facing headwinds, with declining store count and revenues, and lower operating margins; the company reported net losses in 2018 and 2019.

The COVID Effect

In 2020, the company, like most other brick and mortar companies, faced an existential crisis. As the shutdown put their stores out of business, the debt and lease payments that are par for the course for any brick-and-mortar retailer threatened to push them into financial distress. The stock prices for the company reflected those fears, as you can see in this graph (showing prices from 2015 through the start of 2021):

Looking at the graph, you can see that if GameStop is a train wreck, it is one in slow motion, as stock prices have slid every year since 2015, with the added pain of rumored bankruptcy in 2019 and 2020.

A Ripe Target and the Push Back

While mutual funds are often constrained to hold only long positions, hedge funds have the capacity to play both sides of the game, though some are more active on the short side than others. While short sellers target over priced firms, adding distress to the mix sweetens the pot, since drops in stock prices can put them into death spirals. The possibility of distress at GameStop loomed large enough that hedge funds entered the fray, as can be seen in the rising percentage of shares held by short sellers in 2020:

Note that short seller interest in GameStop first picked up in 2019, and then steadily built up in 2020. Even prior to the Reddit buy in, there were clearly buyers who felt strongly enough to to push back against the short sellers, since stock prices posted a healthy increase in the last few months of 2020. To show you how quickly this game has shifted, Andrew Left, one of the short sellers, put out a thesis on January 21, where he argued that GameStop was in terminal decline, and going to zero. While his intent may have been to counter what many believed was a short squeeze on the stock in the prior two days, it backfired by drawing attention to the squeeze and drawing in more buyers. That effect can be seen in the stock price movements and trading volume in the last few days:

This surge in stock prices was catastrophic for short sellers, many of whom closed out (or tried to close out) their short positions, in the process pushing up prices even more. Melvin Capital and Citron, two of the highest profile names on the short selling list, both claimed to have fully exited their positions in the last few days, albeit with huge losses. On January 27 and 28, regulators and trading platforms acted to curb trading on GameStop, ostensibly to bring stability back to markets, but traders were convinced that the establishment was changing the rules of the game to keep them from winning. GameStop, which had traded briefly at over $500/share was trading at about $240 at the time this post was written.

A Value Play?

When you have a pure trading play, as GameStop has become over the last few weeks, value does not even come into play, but there are investors, who pre-date the Redditors, who took counter positions against the short sellers, because they believed that the value of the company was higher. At the risk of ridicule, I will value the company, assuming the most upbeat story that I can think of, at least at the moment:

Note that this valuation is an optimistic one, assuming that probability of failure remains low, and that GameStop makes it way back to find a market in a post-COVID world, while also improving its margins to online retail levels. If you believe this valuation, you would have been a strong buyer of GameStop for much of last year, since it traded well below my $47 estimate. After the spectacular price run up in the last two weeks, though, there is no valuation justification left. To see why, take a look at how much the value per share changes as you change your assumptions about revenues and operating margins, the two key drivers of value.

Even if GameStop is able to more than double its revenues over the next decade, which would require growth in revenues of 15% a year for the next five years, and improve its margins to 12.5%, a supreme reach for a company that has never earned double digit margins over its lifetime, the value per share is about half the current stock price. Put simply, there is no plausible story that can be told about GameStop that could justify paying a $100 price, let alone $300 or $500.

The Backstory

To put the GameStop trading frenzy in perspective, let's start with the recognition that markets are not magical mechanisms, but represent aggregations of human beings making investment judgments, some buying and some selling, for a variety of reasons, ranging from the absurd to the profound. It should therefore not come as a surprise that the forces playing out in other aspects of human behavior find their way into markets. In particular, there are three broad trends from the last decade at play here:

A loss of faith in experts (economic, scientific, financial, government): During the 20th century, advances in education, and increasing specialization created expert classes in almost every aspect of human activity, from science to government to finance/economics. For the most part, we assumed that their superior knowledge and experience equipped them to take the right actions, and with our limited access to information, we often were kept in the dark, when they were wrong. That pact has been shattered by a combination of arrogance on the part of experts and catastrophic policy failures, with the 2008 banking crisis acting as a wake up call. In the years since, we have seen this loss of faith play out in economics, politics and even health, with expert opinion being cast aside, ignored or ridiculed.

An unquestioning worship of crowd wisdom, combined with an empowering of crowds: In conjunction, we have also seen the rise of big data and the elevation of "crowd" judgments over expert opinions, and it shows up in our life choices. We pick the restaurants we eat at, based on Yelp reviews, the movies we watch on Rotten Tomatoes and the items we buy on customer reviews. Social media has made it easier to get crowd input (online), and precipitate crowd actions.

A conversion of disagreements in every arena into the personal and the political: While we can continue to debate the reasons, it remains inarguable that public discourse has coarsened, with the almost every debate, no matter in what realm, becoming personal and political. I can attest to that from just my personal experiences, especially when I post on what I call "third rail" topics, specifically Tesla and Bitcoin, in the last few years.

As I look at the GameStop episode play out, I see all three of these at play. One reason that the Redditors targeted GameStop is because they viewed hedge funds as part of the "expert" class, and consequently incapable of getting things right. They have used social media platforms to gather and reinforce each others' views, right or wrong, and then act in concert quickly and with extraordinary efficiency, to move stock prices. Finally, even a casual perusal of the comments on the Reddit thread exposes how much of this is personal, with far more comments about how this would teach hedge funds and Wall Street a lesson than there were about GameStop the company.

The End Game

I am a realist and if you are one of those who bought GameStop or AMC in recent days, I know that there is only a small chance that you will be reading this post, since I am probably too old (my four children remind me of that every day), too establishment (I have been teaching investing and valuation for 40 years) and too expert to be worth listening to. I accept that, though if you are familiar with my history, you should know that I have been harsh on how investing gets practiced in hedge funds, investment banks and even Omaha. The difference, I think, between our views is that many of you seem to believe that hedge funds (and other Wall Streeters) have been winning the investment sweepstakes, at your expense, and I believe that they are much too incompetent to do so. In my view, many hedge funds are run by people who bring little to the investment table, other than bluster, and charge their investors obscene amounts as fees, while delivering sub-standard results, and it is the fees that make hedge fund managers rich, not their performance. It is for that reason that I have spent my lifetime trying to disrupt the banking and money management business by giving away the data and the tools you need to do both for free, as well as pretty much everything I know (which is admittedly only a small subset) about investing in my classes. My sympathies lie with you, but I wonder what your end game is, and rather than pre-judge you, I will offer you the four choices:

GameStop is a good investment: That may be a viable path, if you bought GameStop at $40 or $50, but not if you paid $200 or $300 a share. At those prices, I don’t see how you get value for your money, but that may reflect a failure of my imagination, and I encourage you to download my spreadsheet and make your own judgments.

GameStop remains a good trade: You may believe that given your numbers (as individual investors), you can sell the stock to someone else at a higher price, but to whom? You may get lucky and be able to exit before everyone else tries to, but the risk that you will be caught in a stampede is high, as everyone tries to rush the exit doors at the same time. In fact, the constant repetition of the mantra that you need to hold to meet a bigger cause (teach Wall Street a lesson) should give you pause, since it is buying time for others (who may be the ones lecturing you) to exit the stock. I hope that I am wrong, but I think that the most likely end game here is that AMC, GameStop and Blackberry will give back all of the gains that they have had from your intervention and return to pre-action prices sooner rather than later.

Teach hedge funds and Wall Street a lesson: I won't patronize you by telling you either that I understand your anger or that you should not be angry. That said, driving a few hedge funds out of business will do little to change the overall business, since other funds will fill the void. If this is your primary reason, though, just remember that the money you are investing in GameStop is more donation to a cause, than an investment. If you are investing tuition money, mortgage savings or your pension fund in GameStop and AMC, you are impoverishing yourself, trying to deliver a message that may or may not register. The biggest threat to hedge funds does not come from Reddit investor groups or regulators, but from a combination of obscene fee structures and mediocre performance.

Play savior: It is possible that your end game was selfless, and that you were trying to save AMC and GameStop as companies, but if that was the case, how has any of what’s happened in the last two weeks help these companies? Their stock prices may have soared, but their financial positions are just as precarious as they were two weeks ago. If your response is that they can try to issue shares at the higher prices, I think of the odds of being able to do this successfully are low for two reasons. The first is that planning a new share issuance takes time, requiring SEC filings and approval. The second is that the very act of trying to issue new shares at the higher price may deflate that price. In a perverse way, you might have made it more difficult for GameStop and AMC to find a pathway to survive as parts of larger companies, by pushing up stock prices, and making them more expensive as targets.

If you are in this game, at least be clear with yourself on what your end game is and protect yourself, because no one else will. The crowds that stormed the Bastille for the French Revolution burned the prison and killed the governor, but once done, they turned on each other. Watch your enemies (and I know that you include regulators and trading platforms in here), but watch your friends even more closely!

Market Lessons

If you are not a hedge fund that sold short on the targeted stocks, or a trader who bought in on other side, are there any consequences for you, from this episode? I do think that we sometimes read too much into market events and episodes, but this short period has some lessons.

Flattening of the Investment World: Borrowing a term from Tom Friedman, I believe that the investment world has flattened over the last few decades, as access to data and powerful tools widens, and trading eases. It should come as no surprise then that portfolio managers and market gurus are discovering that they no longer are the arbiters of whether markets are cheap or expensive, and that their path of least resistance might come from following what individual investors do, rather than lead them. In a prior post, I pointed to this as one reason why risk capital stayed in the game in 2020, confounding many long-term market watchers, who expected it to flee.

Emptiness of Investment Expertise: Professional money management has always sold its wares (mutual funds, hedge funds, investment advice) as the products of deep thinking and serious analysis, and as long as the processes stayed opaque and information was scanty, they were able to preserve the delusion. In the last few decades, as we have stripped away the layers, we have discovered how little there is under the surface. The hand wringing on the part of money managers about the momentum trading and absence of attention to fundamentals on the part of Redditors strikes me as hypocritical, since many of these money managers are themselves momentum players, whose idea of fundamentals is looking at trailing earnings. My prediction is that this episode and others like it will accelerate the shift from active to passive investing, especially on the part of investors who are paying hefty fees, and receiving little in return.

Value ≠ Price: I won’t bore you again with my distinction between value and price, but it stands me in good stead during periods like this one. During the last week, I have been asked many times how I plan to change the way I value companies, as a result of the GameStop story, and my answer is that I don’t. That is not because I am stuck in my ways, but because almost everything that is being talked about (the rising power of the individual investors, the ease of trading on apps like Robinhood, the power of social media investing forums to create crowds) are factors that drive price, not value. It does mean that increasing access to data and easing trading may have the perverse effect of causing price to vary more, relative to value, and for longer periods. My advice, if you are an investor who believes in fundamentals, is that you accept this as the new reality and not drive yourself in a frenzy because you cannot explain what other people are paying for Tesla, Airbnb or Zoom.

In the next few weeks, I predict that we will hear talk of regulatory changes intended to protect investors from their own excesses. If the regulators have their way, it will get more difficult to trade options and borrow money to buy shares, and I have mixed feelings about the efficacy of these restrictions. I understand the motivation for this talk, but I think that the best lessons that you learn about risk come from taking too much or the wrong risks, and then suffering the consequences.

In my last eight posts, I looked at aspects of corporate behavior from investments to financing to dividend policy, using the data that I collected at the start of 2019, to examine what companies share in common, and what makes them different. In summary, I found that the rise in risk premiums in both equity and bond markets in 2018 have pushed up costs of equity and capital, that companies across the globe are finding it difficult to generate returns on their investments that exceed their costs of funding, and that many of them, especially in mature businesses, are returning more cash, much of it in the form of buybacks. Since all of the companies in my data set are publicly traded, there is one final number that I have not addressed directly in my posts so far, and that is the market pricing of these companies. In this post, I complete my data update series, by looking at how pricing varies across companies, sectors and geographies, and what lessons investors can draw from the data.

Value versus Price: The Difference

I have posted many times on the between the value of an asset and its' pricing, but I don't think it hurts to revisit that difference. The determinants of value are simple, although not always easy to estimate. Whether you are valuing start-up businesses, emerging market firms, or commodity companies, the values are driven by expected cash flows, growth, and risk. Although a discounted cash flow valuation is often the tool that we used to give form to these fundamentals, in the form of cash flows, growth rates in these cash flows, and discount rates, it is not the only pathway to intrinsic value. The determinants of price are demand and supply, and while fundamentals do affect both, mood and momentum are also strong forces in pricing. These “animal spirits,” as behavioral economists might tag them, can not only cause price to diverge from value, but also require different tools to be used to assess the right pricing for an asset. With many assets and businesses, pricing an asset usually involves standardizing a price (a multiple), finding similar or comparable assets that are already priced in the marketplace, and controlling for differences. The picture below, which I have used many times before, captures the two processes:

The reason that I reuse this picture so much is because, to me, it is an all-encompassing snapshot of every conceivable investment philosophy that exists in the market:

Efficient Marketers: If you believe that markets are efficient, the two processes will generate the same number, and any gap that exists will be purely random and quickly closed.

Investors: If you are an investor, whether value or growth, and you truly mean it, your view is that the pricing process, for one reason or the other, can deliver a price different from your estimate of value and that the gap that exists will close, as the price converges to value. The difference between value and growth investors lies in where you think markets are most likely to make mistakes (in valuing existing assets or growth opportunities) and correct them. In essence, you are as much a believer in efficient markets as the first group, with the only difference being that you believe markets become efficient after you have taken your position on a stock.

Traders: If you are a trader, you start off with either the presumption that there is no such thing as intrinsic value, or that it exists, but that no one can estimate it. You play the pricing game, effectively using your skills at gauging momentum and forecasting the effects of corporate news on prices, to buy at a low price and sell at a high price.

Market participants are most exposed to danger when they are delusional about the game that they are playing. Many portfolio managers, for instance, claim to be investors, playing the value game, while using pricing screens (PE and growth, PBV and ROE) and adding to their holdings of momentum stocks. Many traders seem to think that they will be viewed as deeper and more accomplished if they talk the value talk, while using charts and technical indicators in the closet, to make their stock picks.

The Pricing Process

The essence of pricing is attaching a number to an asset or company, based upon how similar assets and companies are being priced in the market. To get insight into how to price an asset, a business or a company, you should break down the pricing process into steps:

You may be a little puzzled by the first step in the process, where I standardize the price, but the reason is simple. You cannot compare price per share across companies, since it is a function of the share count, which can be changed overnight in a stock split. To standardize prices, you scale them to some variable that all of the assets in the peer group share. With real estate properties, you divide the price of each property by its square footage to arrive at a price/square foot that can be compared across properties. With businesses, you scale pricing to an operating variable, with earnings being the most obvious choice, but it can be revenues, cash flows or book value. Note that any multiple that you find on a stock or company is embedded in this definition, ranging from PE ratios to EV/EBITDA multiples to revenue multiples, and even beyond, to market price per subscriber or user. The second step in the process, i.e., finding similar assets and companies, should make clear the fact that this is a process that requires subjective judgments and is open to bias, just as is the case in intrinsic valuation. If you are pricing Nvidia, for instance, you determine how narrowly or broadly you define the peer group, and which companies to deem to be "similar". The third step int he process requires controlling for differences across companies. Put simply, if the company that you are pricing has higher growth or lower risk or better returns on its investments on it projects that the companies in the peer group, you have to adjust the pricing to reflect it, either subjectively, as many analysts do, with story telling, or objectively, by bringing in key variables into the estimation process.

Pricing the Markets in January 2019

Rather than taking you through multiple after multiple, and overwhelming with pictures and tables on each one, I will list out what I learned by looking at the pricing of all publicly traded stocks around the world, in early 2019, in a series of pricing propositions.

Pricing Proposition 1: Absolute rules don't belong in a relative world!

Paraphrasing Einstein, everything is relative, if you are pricing companies. Is a PE ratio of five low? Not if half the stocks in the market trade at less than five. Is an EV/EBITDA of forty high? Perhaps in some sectors, but not if you are comparing high growth companies in a highly priced sector. Old time value investing is filled with rules of thumb, and many of these rules are devised around absolute values for PE or PEG ratios or Price to Book, at odds with the very notion of pricing. If you want to make pricing statements about what comprises cheap or expensive, you should be looking at the distribution of the multiple across the market. Thus, to form pricing rules on US stocks at the start of 2019, I looked the distribution of current, forward and trailing PE ratios for US stocks on January 1, 2019:

At the start of 2019, a low trailing PE ratio for a US stock would have been 6.09, if you used the lowest decile or 10.36, if you moved to the first quartile, and a high PE ratio, using the same approach, would have been 27.31, with the third quartile, or 53.70, with the top decile. Lest I be accused of picking on value investors, they are not the only or even the biggest culprits, when it comes to absolute rules. Private equity investors and LBO initiators have built their own set of screens. I have lost count of the number of times I have heard it said that an EV to EBITDA less than six (or five or seven) must mean that a company is not just cheap, but a good candidate for leverage, but is that true? To answer the question, I looked at the EV to EBITDA multiples across companies, across regions of the world.

If you wield a pricing bludgeon and declare all companies that trade at less than six times EBITDA to be cheap, you will find about half of all stocks in Russia to be bargains. Even globally, you should hav no trouble finding investments to make with this rule, since almost one quarter of all companies trade at less than six times EBITDA. My point is not that that you cannot have rules of thumb, since they do exist for a reason, but that those rules, in a pricing world, have to be scaled to the data. Thus, if you want to define the first decile as your measure of what comprises cheap, why not make it the first decile? That would mean that an EV to EBITDA multiple less than 5.16 would be cheap in the US on January 1, 2019, but that number would have to recalibrated as the market moves up or down.

Pricing Proposition 2: Markets have a great deal in common, when it comes to pricing, but the differences can be revealing!

Much is made about the differences across global equity markets, and especially about the divide between emerging and developed market companies, when it comes to pricing, with delusions running deep on both sides. Emerging market analysts are convinced that stocks are priced very differently, and often more irrationally, in their local markets, leaving them free to devise their own rules for their markets. Conversely, developed market analysts often bring perspectives about what comprises high, low or average pricing ratios, built up through decades of exposure to US and European markets, to emerging markets and find them puzzling. The data tells a different story, with pricing ratios around the world having distributional characteristics that are surprisingly similar across different parts of the world:

While the levels of PE ratios vary across regions, with Chinese stocks having the highest median PE ratios (20.63) and Russian and East European stocks the lowest (9.40), they all have the same asymmetric look, with a peak to the left (since PE ratios cannot be lower than zero) and a tail to the right (there is no cap on PE ratios). That asymmetry, which is shared by all pricing multiples, is the reason that you should always be cautious about any pricing argument that is built on comparisons to the average PE or PBV, since those numbers will be skewed upwards because of the asymmetry. While it is true that markets share common characteristics, when it comes to pricing, the differences in levels are also worth paying attention to, when investing. A global fund manager who ignores these differences, and picks stocks based upon PE ratios alone, will end up with a portfolio that is dominated by African, Midde East and Russian stocks, not a recipe for investing success.

Pricing Proposition 3: Book value is the most overrated metric in investing

I have never understood the reverence that some investors seem to hold for book value, as revealed in the number of investing adages built around it. Stocks that trade at less than book value are considered cheap, and companies that build up book value are considered to be value creating. At the root of the "book value" focus are two assumptions, sometimes stated but often implicit. The first is that the book value is a measure of liquidation value, an estimate of what investors would get if they shut down the company today and sold its assets. The second is that accountants are consistent and conservative in estimating asset value, unlike markets, which are prone to mood swings. Both assumptions are built on foundations of sand, since book value is not a good measure of liquidation value in most sectors, and accountants are both inconsistent and slow-moving, when it comes to estimating and adjusting book value. Again, to get perspective, let's look at the price to book ratios around the world, at the start of 2019:

If you believe that stocks that trade at less than book value are cheap, you will again find lots of bargains in the Middle East, Africa and Russia, but even in markets like the United States, where less than a quarter of all companies trade at less than book value, they tend to be clustered in industries that are in capital intensive (at least as defined by accountants) and declining businesses.

Note that among the US industries with the fewest stocks that trade at less than book value are a large number of technology and consumer product companies, with utilities and basic chemicals being the only surprises. On the list of US industry groups with the highest percentage of stocks that trade at less than book value are oil companies (at different stages of the business), old time manufacturing companies and life insurance. If you pick your stocks based upon low price to book, in January 2019, your portfolio will be weighted with companies in the latter group, a prospect that should concern you.

Pricing Proposition 4: Most stocks that look cheap deserve to be cheap!

There are traders who have little time for fundamentals, arguing that they have little or no role to play in day to day movements of stock prices. That is probably true, but fundamentals do have significant explanatory power, when it comes to why some companies trade at low multiples of earnings or book value and others are high multiples. To understand the link, I find it most useful to go back to a simple intrinsic value model, and with simple algebraic manipulation, make it a model for a pricing multiple. The picture below shows the paths you would take with an equity multiple (Price to Book) and an enterprise value (EV/Sales) to arrive at their determinants:

Now what? If you buy into the intrinsic view of a price to book ratio, it should be higher for firms that earn high returns on equity, have higher growth and lower risk, and lower for firms that earn low returns on equity, have lower growth and higher risk. Does the market price in fundamentals? For the most part, the answer is yes, as you can see even in the tables that I have provided in this post so far. Russian stocks have the lowest PE ratios, but that reflects the corporate governance concerns and country risk that investors have when investing in them. Chinese stocks in contrast have the highest PE ratios, because even with stepped down growth prospects for the country, they have higher expected growth than most developed market companies. Looking at stocks with the lowest price to book ratios, Middle Eastern stocks have a disproportionate representation because they earn low returns on equity and the industry groupings with the lowest price to book (oil industry groups, steel etc.) also share that feature. Pricing, done right, is therefore a search for mismatches, i.e., companies that look cheap on a pricing multiple without an obvious fundamental that explains it. This table captures some of the mismatches:

Multiple

Key Driver

Valuation Mismatch

PE ratio

Expected growth

Low PE stock with high expected growth rate in earnings per share

PBV ratio

ROE

Low PBV stock with high ROE

EV/EBITDA

Reinvestment rate

Low EV/EBITDA stock with low reinvestment needs

EV/capital

Return on capital

Low EV/capital stock with high return on capital

EV/sales

After-tax operating margin

Low EV/sales ratio with a high after-tax operating margin

Pricing Proposition 5: In pricing, it is not about what "should be" priced in, but "what is" priced in!

In the last proposition, I argued that markets for the most part are sensible, pricing in fundamentals when pricing stocks, but there will be exceptions, and sometimes large ones, where entire sectors are priced on variables that have little to do with fundamentals, at least on the surface. This is especially true if the companies in a sector are early in their life cycles and have little to show in revenues, very little (or even negative) book value and are losing money on every earnings measure. Desperation drives investors to look for other variables to explain prices, resulting in companies being priced based upon website visitors (at the peak of the dot com boom), numbers of users (at the start of the social media craze) and numbers of subscribers.

I noted this phenomenon, when I priced Twitter ahead of its IPO in 2013, and argued that to price Twitter, you should look at its user base (about 240 million at the time) and what markets were paying per user at the time (about $130) to arrive at a pricing of $24 billion, well above my estimate of intrinsic value of $11 billion for the company at a time, but much closer to the actual pricing, right after the IPO. It is therefore neither surprising nor newsworthy that venture capitalists and equity research analysts are more focused on these pricing metrics, when assessing how much to pay for stocks, and companies, knowing this, play along, by emphasizing them in their earnings reports and news releases.

Conclusion

I do believe in intrinsic value, and think of myself more as an investor than a trader, but I am not a valuation snob. I chose the path I did because it works for me and reflects my beliefs, but it would be both arrogant and wrong for me to argue that being a trader and playing the pricing game is somehow less worthy of respect or returns. In fact, the end game for both investors and traders is to make money, and if you can make money by screening stocks using PE ratios or technical indicators, and timing your entry/exit by looking at charts, all the more power to you! If there is a point to this post, it is that a great deal of pricing, as practiced today, is sloppy and ignores, or throws away, data that can be used to make pricing better.