I start my valuation classes with a question of whether valuation is an art or a science, and I argue that it is neither; it does not have the precision that characterizes a science and unlike an art, it does come with principles that constrain you on what you can and cannot do. I describe valuation as a craft, where you learn as you value companies, and in the process, there are times where you question how it is practiced, and try to find ways to do it better. I have learned my share of lessons in the four decades that I have practiced valuation, and I have often abandoned standard practices, in the hope of developing better ones. There is no input in valuation where I have found myself questioning existing practices more than in estimating the price of risk in equity markets, i.e., the equity risk premium, and I have wrestled with ways of coming up with alternatives. That endeavor was pushed into high gear by the 2008 market crisis, when I started to pay more attention to how markets price risk, what causes that price of risk to change over time and the limitations in the ways that we estimate that price of risk in financial analysis.

Status Quo and Standard Practice

Leading into 2008, I had long been skeptical about how we approached the estimation of equity risk premiums, essential ingredients in hurdle rates in corporate finance and discount rates in valuation. It was (and still remains) standard practice to look at historical data, almost entirely from the US, on what stocks had earned over treasuries, and use that historical equity risk premium as the best estimate of the equity risk premium for the future, That approach would have yielded an equity risk premiums of between 5.5% to 14.5%, at the start of 2026, depending on the time period used, the way we compute averages and what we use as the riskfree rate.

These historical equity risk premiums are not only backward-looking and very noisy (see the standard errors), but they allow bias to easily creep in, through the choice of equity risk premiums, with bullish (bearish) analysts picking lower (higher) numbers. Disconcertingly, they also move in the wrong direction, falling during crises (as historical returns get updates) and rising during good times.

A Forward-Looking Alternative

To counter the problems that I saw with historical risk premiums, I started estimating forward-looking equity risk premiums, by essentially backing out from stock prices and expected cash flows, the expected return (internal rate of returns) that markets were pricing into stocks.

That approach yields forward-looking equity risk premiums, and while there is estimation error in the expected earnings growth and payout numbers, it yields vastly more precise estimates that are also model-agnostic. Using this approach, the equity risk premium at the start of 2026 was 4.23% (over the US treasury bond rate): Note that this estimation is model-agnostic, and is simply a measure of what markets are pricing in, given expected cash flows at the moment.

Note that this estimation is model-agnostic, and is simply a measure of what markets are pricing in, given expected cash flows at the moment.

Oil is up to over a hundred dollars a barrel and the S&P 500 is down, but so far, the market is not behaving as if it is in crisis mode. The equity risk premium, which started March at 4.37% has risen, but only to 4.51%, over the two weeks. In fact, it is the ten-year US treasury bond that has had the bigger surge, up from 3.97% at close of trading, on February 27, to 4.28% at close of trading, on March 13, indicating inflation fears are trumping other market concerns right now. All of this could change next week or the week after, and I will continue to track the equity risk premiums, by day, until the market settles in.

As you can see, all of these variables can and will change over time, explaining why the ERP should be a volatile number.

As you can see, all of these variables can and will change over time, explaining why the ERP should be a volatile number.

Since a good ERP estimate should have a large positive correlation with actual returns on stocks in future years, the current implied premium does best for the five-year and ten-year return, and the historical risk premium does worst, with actual returns increasing (decreasing) when it decreases (increases). In bad news for market timers, none of the equity risk premium approaches does well at forecasting next year's actual return, and even at the longer time periods, there is significant error in predictions.

Since a good ERP estimate should have a large positive correlation with actual returns on stocks in future years, the current implied premium does best for the five-year and ten-year return, and the historical risk premium does worst, with actual returns increasing (decreasing) when it decreases (increases). In bad news for market timers, none of the equity risk premium approaches does well at forecasting next year's actual return, and even at the longer time periods, there is significant error in predictions.

Paper

That approach yields forward-looking equity risk premiums, and while there is estimation error in the expected earnings growth and payout numbers, it yields vastly more precise estimates that are also model-agnostic. Using this approach, the equity risk premium at the start of 2026 was 4.23% (over the US treasury bond rate):

ERP Estimation during Crises

Unlike historical equity risk premiums, these implied premiums are sensitive to market gauges of fear and greed, and change, as those change. In fact, I computed the ERP, by day, during the 2008 market crisis, and you can see the shifts during that 14-week period below:

Note that the crisis started with the equity risk premiums at 4.2% on September 12, 2008m but almost doubled over the next two months, as stocks went into free fall. To me, these implied equity risk premiums made far more intuitive sense, rising as market fears about banks and the economy rose.

I have continued with the practice of estimating equity risk premiums, by day, during market crises (real or perceived). Here, for instance, is my assessment of the UK market in 2016 in the weeks leading up to the Brexit vote, the market reaction to COVID and the global economic shutdown in 2020, and how the tariffs roiled markets last year. In fact, as we wrestle with an war and oil price induced market shock in March 2026, I started my daily estimates for the ERP on March 1 and will report on how that price has changed over the last two weeks, in the next section.

Equity Risk Premiums - Lessons Learned

The process of estimating implied equity risk premiums on a continuing basis is driven less by intellectual curiosity and more by my need for these numbers, when I value companies. That process has taught me three lessons about equity risk premiums, and I have responded by altering my practices.

1. The equity risk premium is a dynamic and shifting number, and a good estimate of the premium should reflect this volatility. Using an equity risk premium that is different from the implied equity risk premium makes every valuation a joint judgment on what you think about the company and what you think about the market. Put simply, sticking with a 4% equity risk premium during a crisis, when the implied risk premium has surged to 6% will lead you to find most companies to be undervalued, almost entirely because you think that the market is undervalued (not the company). In my view, a company valuation should be market-neutral, and the only way you can get there is by using a current implied equity premium.

My response: Rather than compute the implied equity risk premium at the start of every year, and using that premium over the course of the year, I shifted to computing the equity risk premium for the S&P 500 at the start of every month, in September 2008. I report those numbers on my entry page to my website (damodaran.com) and use them to value companies during the course of the month. You can find these monthly equity risk premium estimates by going to this link.

2. The implied equity risk premium is a consolidated metric for market pricing, and every debate or discussion about whether the market is under or over priced can be reframed as a debate about whether the implied equity risk premium is too low (over pricing), just right (fairly priced) or too high (under pricing). Since the implied ERP incorporates the level of interest rates, expected growth and cash payout, it is a more complete assessment of the market than looking at dividend yields and earnings yields (or variants of PE ratios), two widely used proxies for market pricing. In this post, I took an extended look at how these different measures of equity risk premiums measure up, in terms of predicting future equity returns.

My response: I have been open about my discomfort with timing markets, but when I am asked what I think of the overall market (Is it too high? Is it a bubble?), I first measure the current equity risk premium and then assess it against history. I used this technique to assess US equities at the start of this year in a post, with the accompanying graph:

My conclusion, at the start of 2026, was that while stocks were richly priced using almost every conventional metric (high PE ratios, low dividend yields), the implied equity risk premium was in line with what US stocks have generated over the last 65 years. That said, I did note that 2025 was a tumultuous year, with tariffs making the news and the post-war dollar-centric global economic system starting to fray, and argued that the market seems to be too sanguine about catastrophic risk. Almost on cue, two weeks ago, bombs started falling in the Middle East, and US equities and bonds have been struggling to price in the effects of higher oil prices. In keeping with my practice of estimating equity risk daily, during troubled times, I did compute the implied ERP for the S&P 500 every day, during the last two weeks (Feb 27- March 13):

Oil is up to over a hundred dollars a barrel and the S&P 500 is down, but so far, the market is not behaving as if it is in crisis mode. The equity risk premium, which started March at 4.37% has risen, but only to 4.51%, over the two weeks. In fact, it is the ten-year US treasury bond that has had the bigger surge, up from 3.97% at close of trading, on February 27, to 4.28% at close of trading, on March 13, indicating inflation fears are trumping other market concerns right now. All of this could change next week or the week after, and I will continue to track the equity risk premiums, by day, until the market settles in.

3. The equity risk premium is an essential ingredient into almost every part of financial analysis, incorporated into hurdle rates in corporate finance, discount rates in valuation and in expected returns on equity in financial planning. Given this centrality, I was surprised how little attention it has received from both academics and practitioners, when I looked for references. There is very little usable academic research on equity risk premiums specifically, though there is a great deal on asset pricing and risk. As for practitioners, they have, for the most part, relied on historical risk premiums, and often obtain these premiums from services that summarize the historical data. When I took my first finance class, the historical risk premiums came from data from Ibbotson Associates, that contained annual return data on stocks, bonds and bills. That data was acquired by Duff and Phelps, where it became part of a voluminous book on cost of capital, but much of what that book had to say about equity risk premiums reflected slicing and dicing the historical data, hoping to get further insights, and for the most part failing, because of the noisiness in the data. The US historical data is now in the hands of Kroll, but there is little of value that be extracted by doing deeper and deeper mining expeditions on historical return data. In fact, if you are a fan of historical equity risk premiums (I am not, as you can guess), my suggestion would be to use the Credit Suisse Yearbook, which looks at historical equity risk premiums in 20 markets over more than a hundred years, and does not suffer from the selection bias of focusing on just US data.

My response: I am a practitioner and I decided, for my own understanding, to pull together everything I knew about equity risk premiums into a paper that I wrote in early 2009, and shared online that year. Practitioners seemed to find it useful, and I have updated that paper every year since, at the start of the year. It has grown over time, as I have sought to pull together new findings on equity risk premiums and incorporate changes in markets, and my seventeenth annual update is now ready. I have to confess that at this point, much of the change is data-driven, with tables and graphs updated to include the most recent year's data, but I hope you still find it useful. The paper resides on the social science research network (SSRN), an Elsevier-run platform for working papers in the social sciences. Unlike most of the other papers on that platform, I have no interest is ever publishing this paper, but you are welcome to download not just the paper, but all of the data that goes with the paper.

Equity Risk Premiums - The 2026 Edition

If you do get a chance to download the paper, I should warn you ahead of time that it long (153 pages), unexciting and entirely directed at practitioners. It is modular, though, and it is broadly broken down into the following sections:

1. The Determinants of Equity Risk Premiums: Given that equity risk premiums represent the price of risk in the market, it should come as no surprise that almost everything that happens in the market, political or economic, affect its level. The picture below summarizes the determinants, and you can find more details in the paper:

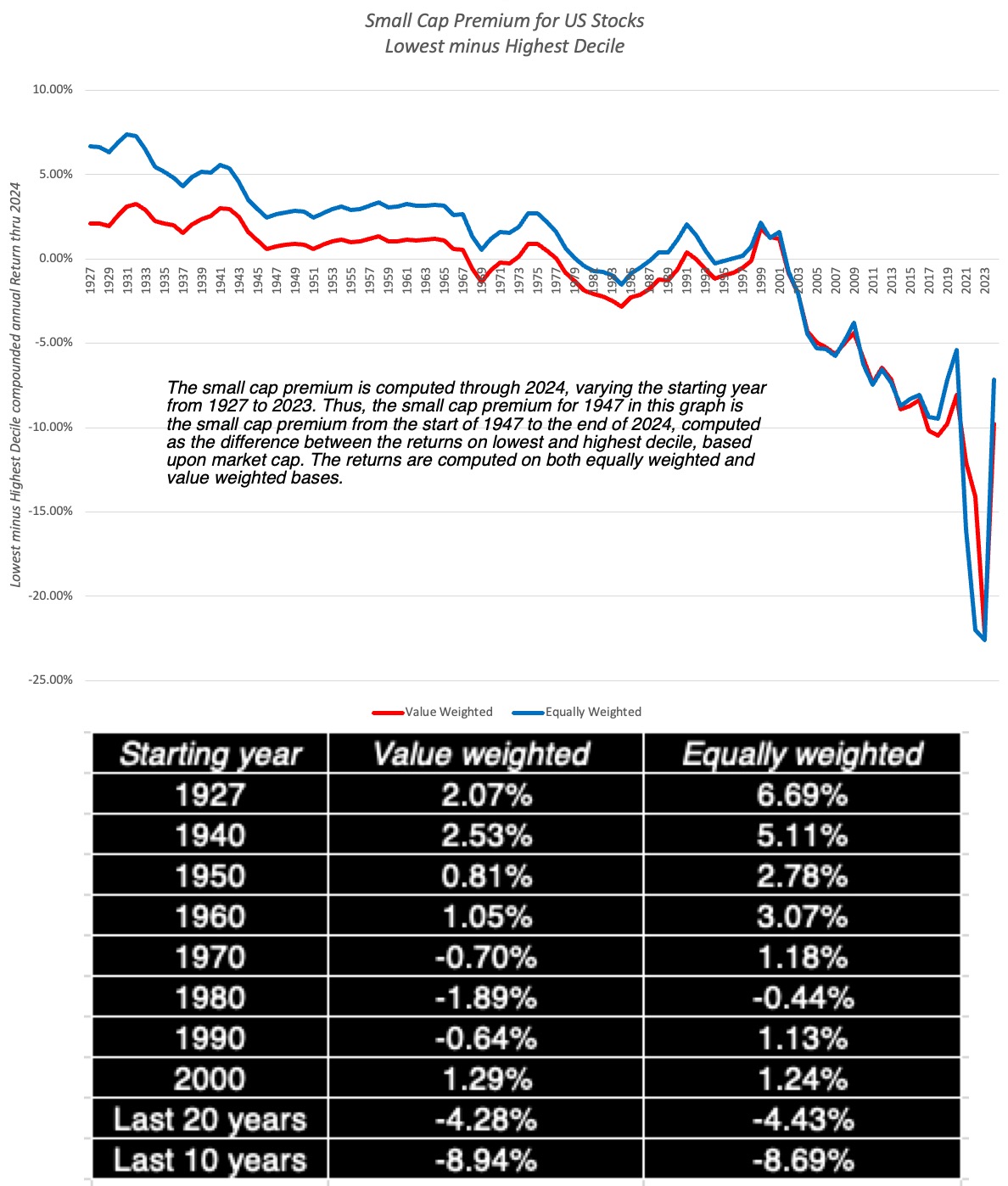

2. Historical Equity Risk Premiums (and spin offs): I spend a section of the paper discussing historical equity risk premiums, examining the statistical properties that make it a faulty approach, and why a belief in mean reversion has made it the status quo. While most of the historical equity risk premiums that you see reported in practice come from the US and are based upon the Ibbotson data going back to 1926, I also look at historical data that goes back further (to 1871) as well as historical premiums in the rest of the world. The historical data on returns in the US has also been mined by services to extract premiums that have been earned by subsets of stocks, and since these premiums often get used by practitioners, I look at the efficacy of these premiums. I specifically look at the small cap premium, a widely used add on in valuation, and not that not only has it been noisy over the entire time period (1926-2025), but that it has disappeared since 1981:

The fact that the small cap premium endures in practice is a testimonial to how once bad practices become embedded in valuation, they never leave.

3. Equity Risk Premiums, by country: While I do have a companion paper that explores country risk in detail, that I update in the middle of the year, I describe my process for estimating equity risk premiums, by country, starting with a mature market premium, and then adding on additional premiums, based on country default risk spreads (based on ratings and sovereign CDS spreads).

4. Implied Equity Risk Premiums and Alternatives: In this section, I start with a description of an intrinsic value model for the market, and use that model to illustrate what you would need to assume for the dividends yield or earnings yield to become reasonable proxies for the equity risk premiums; for the latter, for instance, you have to assume either that there is no earnings growth or that if there is growth, it is value neutral. I then use the full version of the model, allowing for higher growth and cash payout that includes buybacks, to derive my implied equity risk premium estimates. I also look at how my implied equity risk premium estimates relate to other risk proxies (default spreads on bonds, VIX etc.) and how they change over time, as the riskfree rate changes.

5. Efficacy of ERP Estimates: The test of whether an equity risk premium estimate is a good one is in the data, since equity risk premiums measure expectations of what investors hope to earn on equities in future periods. In the last section of the paper, I examine the predictive efficacy of alternative measures of equity risk premiums, by looking at their correlation with actual stock market returns in the next year, the next five years and the next ten years: