As we get deeper into earnings season for the third quarter of 2022, the biggest negative surprises are coming from technology companies, with the tech giants leading the way. Investors, used to a decade of better-than-expected earnings and rising stock prices at these companies, have been blindsided by unexpected bad news in earnings reports, and have knocked down the market capitalization of these companies by hundreds of billions of dollars in the last few weeks. Facebook (or Meta, if you prefer its new name), in particular, has been in the eye of the storm, down more than 75% from the trillion-dollar market capitalization that it enjoyed just over a year ago. In its last earnings report, the company managed to disappoint almost every segment of the market, shocking growth investors with a drop in quarterly revenues, and value investors with a sharp decline in earnings and cash flows. In the days after the report, the reaction has predictably fallen into the extremes, with one group arguing that this is the beginning of the end for the company's business and the other suggesting that this is the time to buy the stock, as it prepares for a new growth spurt.

Having valued and invested in Facebook multiple times in the last decade, I will throw my two cents in, but rather than make the earnings report the center of attention, I will use the company's recent travails to talk about three issues that I think are big issues not only at Facebook, but for the entire market. In this first post, I will use the investor debate about Facebook to talk about corporate governance, what it is, why it matters and how I think governance disclosure research, rules and scoring services have lost the script in the last two decades. In the next post, I will use Facebook's most recent earnings surprise to talk about inconsistencies in how accountants categorize corporate spending, and why these inconsistencies can skew investors perceptions of corporate profitability and financial health. In the third and final post, I will argue that Facebook's troubles with the market have as much to do with a failure of narrative, as they are about disappointing numbers, and present a template for what the company needs to do, to reclaim the high ground.

Facebook: Filling in the Background

It is worth noting that in good times, when earnings are rising and stock prices are upward bound, investors do not seem to have much interest in corporate governance, and it is only when the numbers start to move against them, that they rediscover the importance of the topic. To understand why talk about corporate governance at Facebook has been muted for much of its corporate life, and why it is a prime topic of conversation now, let's retrace Facebook's journey, over the last decade, from a young VC-backed private company to a high-profile public company.

The Market Journey

Facebook is a young company, at least in chronological time, having been public for just over a decade. I have written about the firm many times, over that period, starting with a valuation that I did of the company in 2012, just ahead of it going public. On May 12, 2012, Facebook's debuted in financial markets, with a capitalization of $104 billion, making it one of the most valuable IPOs of all time. After a rough start, with its stock price halving by August 2012, the company embarked on an extraordinary run in markets, adding almost $900 billion to its market capitalization to briefly breach a trillion dollars in July 2021. In a post in 2020, I highlighted how much of the increase in US equity values in the 2010-2019 decade was because of the FANGAM stocks (Facebook, Amazon, Netflix, Google, Apple and Microsoft):

Since July 2021, Facebook's market standing has fallen precipitously, with its market capitalization down to less than $250 billion (down more than 75% from its high) on October 27, after its most recent earnings report. As Facebook's market capitalization has collapsed, it is worth stepping back and gaining perspective about its market performance in the long term.

- Buy and hold returns: If you had bought shares in Facebook on its first trading day, you would have paid $38.12, and if you had held the stock through October 27, 2022, when it was trading at $93/share, that would have translated into a cumulative return of 144%. That would have left you lagging the 181% price appreciation that you would have earned on the S&P 500 during the period, and even more so, if you consider the fact that you would have earned no dividends on Facebook, while generating about a 2% dividend yield, every year on the index.

- Current standing: At a roughly $250 billion market capitalization, Facebook is a large market-cap company, but it has lost its standing among the largest market cap companies in the world that if occupied for an extended period during the last decade.

- Trader's game: Along the way, Facebook has had its ups and downs, and a savvy trader who was able to time entry and exit into the stock at the right times, would have made a killing on the stock. I know that can be said of any stock, but the swings in fortune are much greater at companies like Facebook, making them them the preferred habitat for traders of all stripes.

The Operating Journey

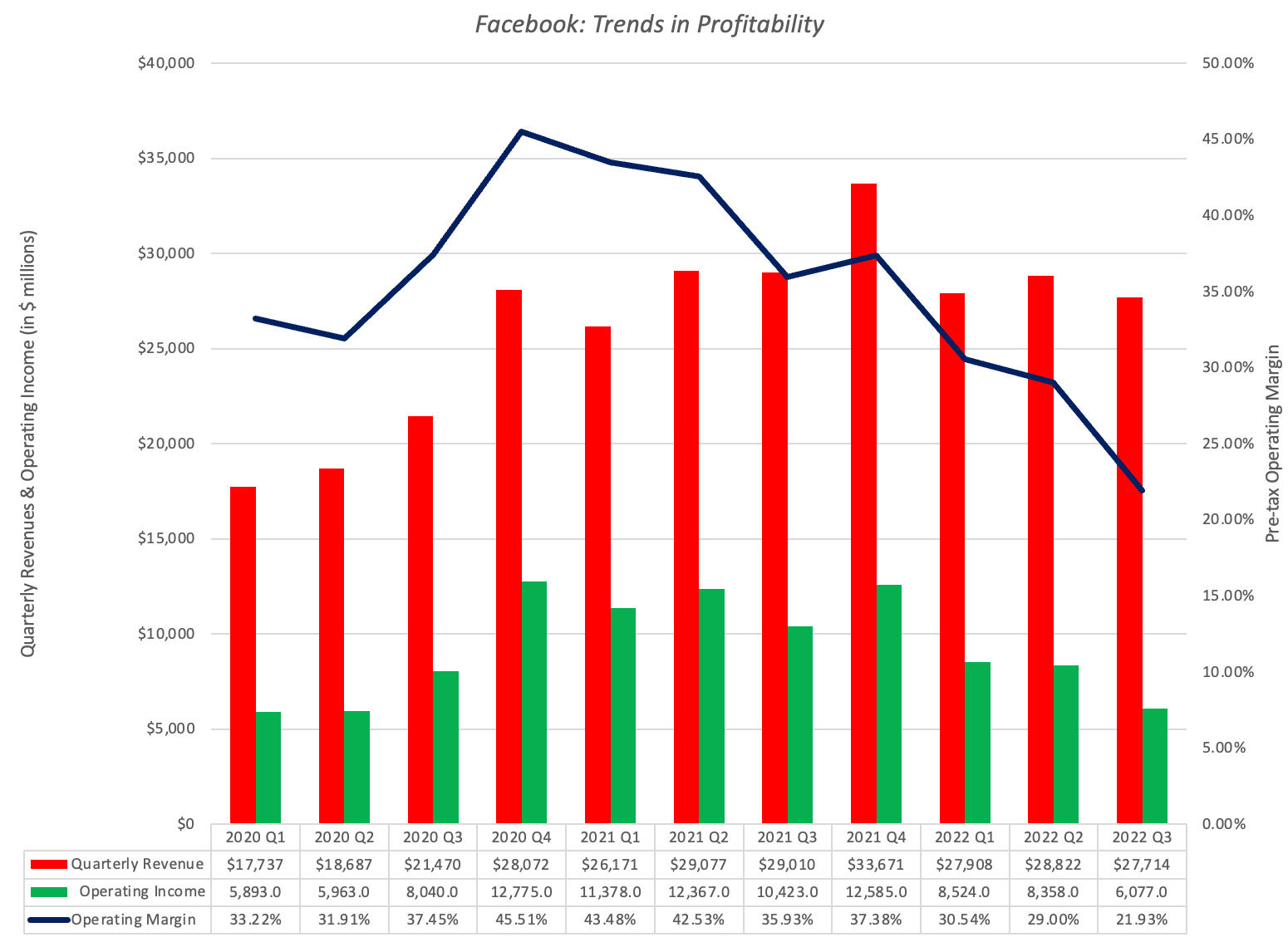

The drop in Facebook's stock price that has occurred in 2022 is part of a larger story of a decline in tech companies during the year. For many value investors, the tech stock drop has been vindication that no sector, no matter how favored, can fight gravity in the long term, but they would be making a mistake if they bundle Facebook in with younger tech companies, many of which have unformed business models and an inability to be profitable. Through its entire life, one of Facebook's most impressive features has been its capacity not only to generate profits but very large profits, as you can see in the chart below:

Note that Facebook, then it went public, had revenues of only $3.7 billion, but it generated an operating margin of 47.3%, with its online advertising model. In the decade since, its has been able to scale up revenues dramatically, with revenues reach $118 billion in 2021, while preserving sky-high margins, close to 40% in 2021. In short, Facebook has been a profit and cash machine for its entire public market life, and there is more to this company than traders pushing up stock prices on momentum.

It is this historical context of high growth, albeit slowing as the company scales up, and consistently high operating margins, that should explain investor reactions to last week's earnings report. There were at least two negative surprises in the report that led to investor reassessment:

- Flat revenues: While revenue growth has been slowing in recent quarters, and investors would perhaps have lived with single digit growth, especially with advertising spending slowing, they were blindsided when the company reported its second consecutive year-on-year quarterly revenue decline . The company's contention was that the decline was driven by a slowing down in online advertising revenues at the firm, mirroring similar slowdowns at other online advertising platforms.

That said, there is clearly more to it than an industry-wide slowdown, since the drop in revenues at Facebook has been larger than the drops seen across the sector; Google, for instance, reported a third quarter year-on-year revenue growth rate of 6% in October 2022. - Drop in operating margins: The bigger shock in the most recent earnings report, in my view, was the collapse in operating margins.

While the decline in operating income in the first two quarters of 2022 mirror drops in revenues in those quarters, the decline in the third quarter cannot be explained by lower revenues in that quarter. The company attributed the decline in operating income to its Reality Labs unit, which houses its VR headsets, with reported revenues of $285 million and an operating loss of $3.67 billion in the third quarter of 2022.

The Troubles

While 2022 has been a particularly difficult year for Facebook, the troubles at the company date back to 2018, when it was revealed that Cambridge Analytica, a UK-based data service with political clients, had acquired and utilized Facebook data on tens of millions of users. In the aftermath, Facebook faced both political and investing backlash, with its stock price dropping by more than 10% and there were some doomsayers who argued that its business model was irretrievably broken, because of the privacy challenges. At the time, I pointed to the hypocrisy of critics complaining about Facebook's privacy lapses on their Facebook pages, and argued that the company would weather the scandal, albeit with scars. In the months after, that view was vindicated as Facebook spent billions on tightening security, while continuing to grow revenues and report sky-high margins, and the market responded by pushing up its stock price once again.

While Facebook was able to deal with the privacy challenge, relatively unscathed in economic terms, there are three other problems that the company is facing that will not be as easily overcome:

- Online Ad Market Leveling off: Facebook is an online advertising company, and for much of its early years, it benefited from growth in the online advertising market, largely at the expense of traditional advertising (newspapers, television etc.). As online advertising approaches two-thirds of all advertising, that growth is now leveling off, and as one of the two largest players (and beneficiaries) of the market, Facebook is facing a growth crunch.

- Online advertising is cyclical: As online advertising has grown over the last decade, one of the questions has been whether it, like all advertising historically, is cyclical. Prior to this year, there were some who argued that online advertising would be more resilient than traditional advertising, in the face of economic shocks, but this year's developments have shown otherwise. As economic growth has slowed and concerns about a recession have risen, revenue growth has dropped at all of the companies in this space has declined. The conclusion is that online advertising is cyclical, and if we are in the midst of an economic slowdown, the companies in this space will feel the pain.

- Reputation effects: While Facebook made it through the privacy challenges with revenue growth and profitability intact, it is undeniable that the company's reputation took a beating. In my view, this toxicity, as much as the desire to enter a new market in the Metaverse, explains why Facebook changed its name to Meta in November 2021.

In fact, it is this trifecta of developments (a maturing online ad market, exposure to economic cyclicality and reputation damage), in conjunction with Facebook's disappointing operating numbers that has led investors to reassess its worth, and mark down its price.

Corporate Governance

As stock prices have dropped this year, not only is there an increased focus on earnings and cash flows, as I noted in my last post, but there seems to also be an reawakening among investors about the importance of corporate governance, as can be seen in this article about Facebook. Having seen these awakenings many times over the last 30 years, I am cynical that anything productive will come out of these discussions, since we seem to have lost sight of what corporate governance is and why it matters to investors.

The Stakeholders

To set the stage for understanding corporate governance, it is best to start with a recognition of the different stakeholders in a publicly traded company:

- In what types of firms is this conflict of interest greatest? If the conflict of interest that is at the heart of corporate governance is that between the owners of a business and those who manage that business, it will begin when private businesses seek out capital from external sources, as founder and venture capital interests can diverge. These conflicts will expand, as companies go first go public, and the interests of insiders and founders, who run the firm, can be at odds with the interests of outside shareholders. As companies age, founders will move on and get replaced by professional managers, and these managerial interests can clearly be at odds with those of shareholders, with boards of directors, in theory, watching out for the latter. In short, conflicts of interest exist at almost all businesses, though the nature of the conflict will change as companies go from private to public, and as they age.

- When the interests of shareholders and corporate decision-makers diverge, what are the consequences for the company? When the interests of decision makers or managers at a business diverge from those of its owners, it is inevitable that there will be decisions made that advance the interests of the former at the expense of the latter. With private business that access venture capital, founders may make decisions (on product design, business models, marketing) that venture capitalists may not find to their liking. With public companies that are run by founders/insiders, the decisions made by inside shareholders to advance their interests may not align with the interests of outside shareholders. In older public companies, the investing, financing and dividend decisions that managers make may by in direct opposition to what shareholders would like them to do.

- What are the checks on these conflicts of interest? In each of the scenarios described above, it is true that there are mechanisms that exist to keep these conflicts in check. In private firms with venture capital investors, VC investors are often actively involved in management, and, if they have the power, have few compunctions about pushing out founder/managers who don’t serve their interests. In public companies, with insiders and founders in charge, the only recourse that outside shareholders often have, if they feel their interests are being ignored, is to sell and move on, hoping that the resulting drop in stock prices causes a change in course. In theory, the boards of directors at these companies are supposed to protect shareholder interests, but that protection is sporadic and often ineffective.

The Essence of Corporate Governance

After five decades of research in corporate governance, my sense is that we have lost the forest for the trees, with the composition of boards of directors and rules on proxy voting receiving disproportionate attention, from both legislators and regulators, often at the expense of bigger and more consequential issues. In the aftermath of the Enron and Tyco scandals in the United States, where insider-dominated boards were negligent in their oversight responsibilities, the Sarbanes-Oxley Act was passed in 2002, with improved corporate governance as one of its objectives. At about the same time, you saw the advent of services that used the disclosures that companies were required to make on governance to estimate corporate governance scores. We were told at the time that the combination of independent boards, increased disclosure and governance scores would create a revolution in corporate governance, where managers would act to advance shareholder interests. It is clear that twenty years later that all that Sarbanes Oxley has accomplished is replacing ineffective insider-dominated boards with ineffective independent boards, while creating hundreds of pages of disclosure that no one reads and giving rise to scores that are close to useless in judging governance. With the push towards diversity in board composition now taking precedence, this process is hurtling even more into irrelevance, with the only positive being that the ineffective boards of the future will meet all our diversity criteria.

I believe that for a true shift in corporate governance to happen, we have to reframe the meaning of good corporate governance, shifting away from a board-centered, check-box driven view to one that is centered on giving shareholders the power to change company management, if they choose to. In fact, good corporate governance is like a good democracy, where shareholders (voters) get the power to change management (governments), when they believe that their interests are not being served. As in a democracy, there is no guarantee that shareholders will make the right or even informed choices, sometimes choosing not to make changes, even when change is required, and sometimes deciding to replace good managers with bad ones. Good corporate governance is sometimes chaotic and often unsettling, and it is no surprise that there are many who are drawn to the benevolent dictatorship model, where "qualified, well-intentioned managers" are given lifetime tenure, with shareholders stripped of the power to challenge them. That latter model was the default for publicly traded companies in much of the world, for the twentieth century, and even in the US, you had managerial apologists like Marty Lipton and corporate strategists arguing that corporate management would be more effective, without shareholder oversight.

The "Right" Management: A Corporate Life Cycle Perspective

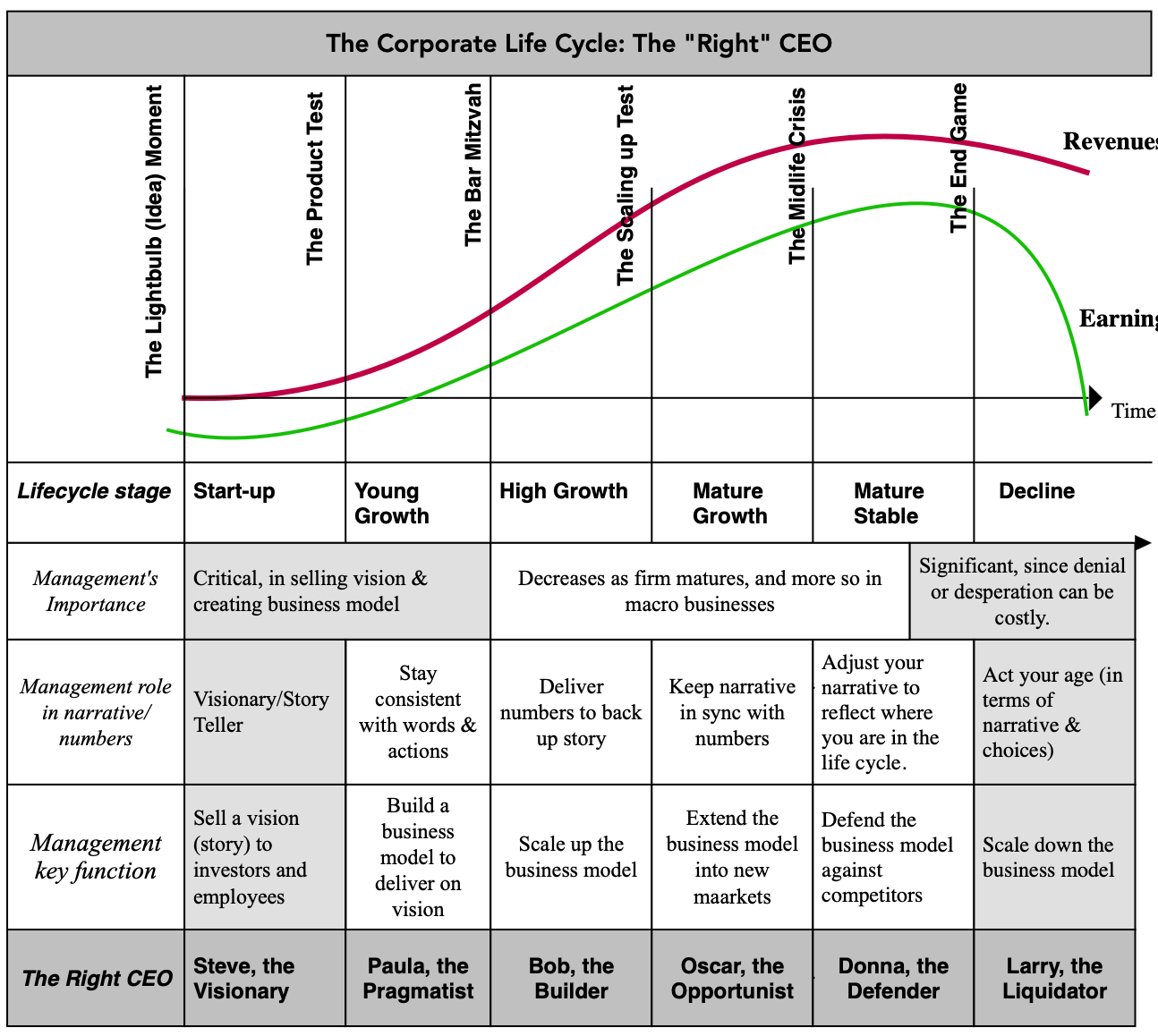

If corporate governance is about giving more power to business owners to change management at the companies that they are invested in, if they choose to, to understand it, we have to begin by looking at why management change may be needed in the first place. I will use the corporate life cycle, a structure that I have used in many other contexts, to set the stage for this discussion, by noting that the qualities that you will look for in "good" management will change as companies move through the life cycle, from start-up to growth to mature and then on to final decline. In the figure below, I have highlighted the role that top management play at a business, and how that role will change as companies age.

Early in the life cycle, as a start-up, the quality that you value most in your top management (and especially in your CEO) is vision, the capacity to tell the story of the business, and get investors and employees on board. As you move from idea to product, you still need vision, but it has been paired with pragmatism, and you would like the business to be run by someone who is willing to make compromises on design and strategy, to create a market for the product. The trash can of failed businesses is filled with purist founders who insisted on having their way, and refused to bend their dreams to meet reality. In the next phase, you need a CEO who is willing to do the work needed to build a business, an often unexciting job that requires attention to supply chains, marketing campaigns and product manufacturing. As businesses look to scale up, they are best led by opportunists who can seek out new markets that allow small businesses to become bigger, and once mature, you want an executive at the top who can play defense against competitors and disruptors. In decline, you need a realist who takes what the business has to offer, and does not try to overreach, in many ways the polar opposite of the visionary you sought out as a start-up.

Management Mismatches across the Life Cycle

Understanding how the qualities that you look for in good management change, as the company changes, provides a framework for assessing why you can end up with management mismatches, where the managers running the firm are unsuited to running it. In some cases, it can happen because the business changes (from start up to young growth or from high growth to mature), but the person running it does not, will not or cannot change. In other cases, it can represent a hiring mistake, as is the case when the board of directors at a high growth firm seek out the CEO of a mature company, competent but risk-averse, to run their business. In still others, it can just be hopeful thinking, where the board of directors at a declining firm seek out a visionary CEO, hoping that this hire can reverse aging and become young again. In the figure below, I have listed CEO/Company mismatches across the life cycle:

The Compressed Life Cycle

A corporate life cycle resembles the human life cycle, in terms of its sequence, but there are two significant differences. The first is that the mortality rate is far higher in the corporate life cycle, as more than two thirds of businesses do not make it through the early stages, than it is for human beings, at least in the twenty first century. The second is that unlike the human life, the corporate life cycle does not follow chronological time. Kongo Gumi, a family-owned Japanese company in the business of constructing temples and shrines, lasted for almost 1500 years, before being acquired in 2006. In contrast, there are businesses that are shooting stars that survive for only 15 or 20 years, before liquidating or selling themselves. In the figure below, I look at the variables that determine how quickly a business grows, how long it stays at the top and the speed of its decline:

The Investor Surrender

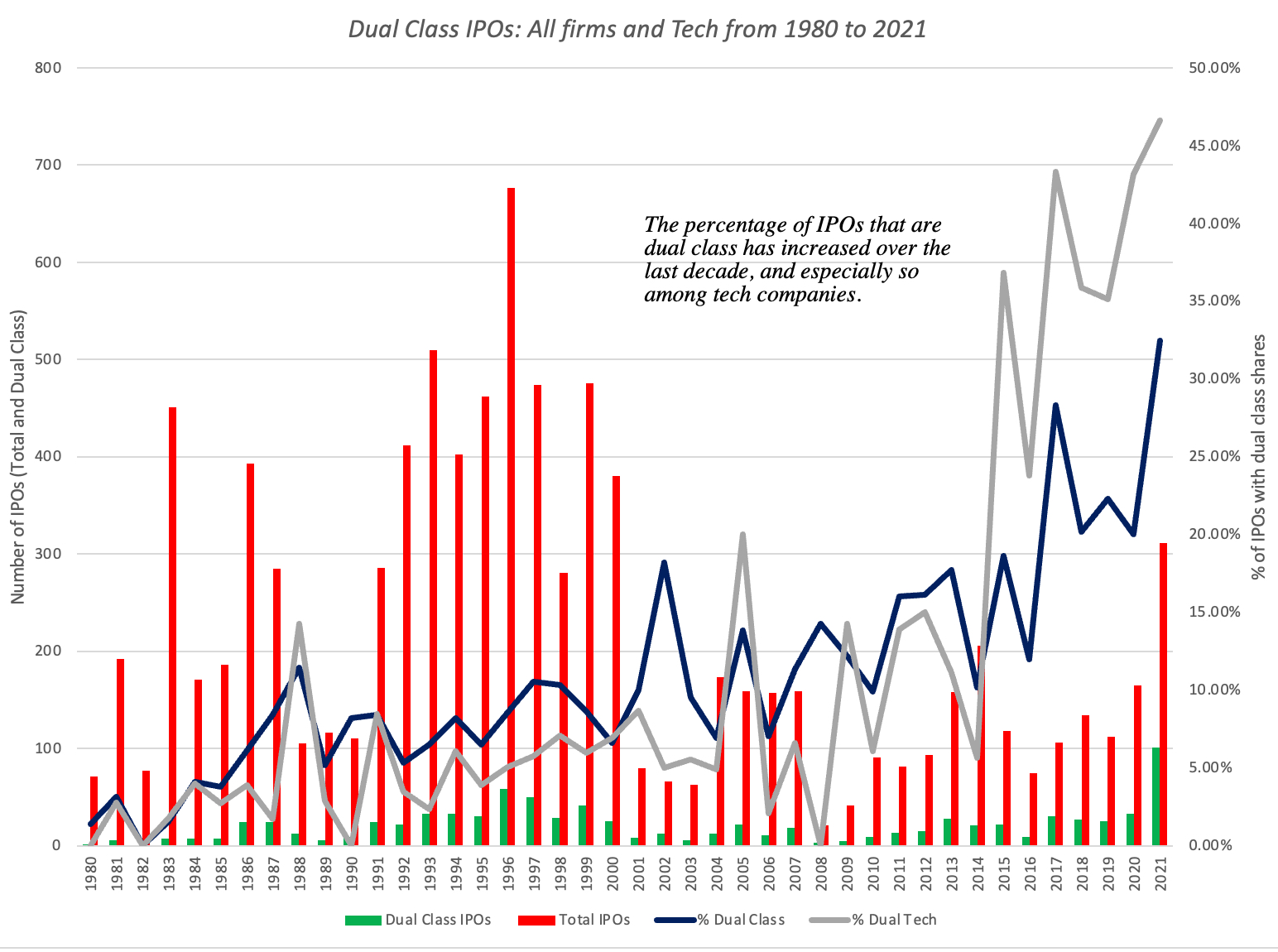

If you accept my thesis that shorter corporate life cycles increase the likelihood of management mismatches at companies, it follows that we, as investors, need tools and processes that increase our power to change management at these firms. It is in this context that we have look back, with dismay at how willingly we have given away the power to create change at companies, and especially so at technology companies. While corporate governance measurement services and academics were obsessing over board composition and management compensation, companies have been changing the rules of the governance game, tilting power decisively away from shareholders, with little or no pushback. In the last two decades, US companies, have increasingly turned to dual-class shares, with one class having significantly more voting rights than the other, and with founders/insiders holding these voting shares. You can see this phenomenon play out in the chart below, where I graph out the percentage of companies, going public with dual-class shares, each year from 1980 to 2021:

Cutting to the chase, Zuckerberg controls 57% of the voting rights in the company, while owning only 13.52% of all outstanding shares, largely because he holds the bulk of the voting shares. Rather Han a corporate democracy, Facebook’s elections resemble those in authoritarian regimes, where you can vote for whoever you want, but the winner is pre-determined. (Just as an aside, I found a Facebook proposal to the SEC, thankfully stillborn, to create Class C shares with no voting rights, in 2017. That would have added insult to injury!)

In short, shareholders have been disempowered at some of our largest and most valuable companies, and they have, for the most part, gone along. There is plenty of blame to go around, but the following culprits stand out:

- Market-share seeking Stock Exchanges: For much of the last century, starting with a de facto ban in 1926 and a rule in 1940, the New York Stock Exchange barred companies listed on the exchange from from issuing shares with different voting rights, and with its dominance over US equity markets, that became the rule followed by most US companies. The American Stock Exchange adopted slightly looser rules, hoping to get market share from the NYSE, but it was the NASDAQ that threw caution to the winds entirely and removed all restrictions on voting and non-voting shares. That proved to be a great business decision, since the largest tech companies of this century have not only listed on the NASDAQ, but chosen to stay there, but it came at the expense of shareholder powers.

- Founder Worshippers: For the last few decades, we have glorified the founders of technology companies, and while there is much to admire in their accomplishments, there is a danger in putting them on pedestals and attributing to them heroic or superhuman qualities. In the case of companies like Google and Facebook, and especially so at the time of their public offerings, there were many investors, including some of the largest institutional players, that were willing to make the trade off of giving up power to change management in return for being invested in companies run by "young, tech geniuses". In fact, there are some researchers who were willing to argue that removing the threat of shareholder power made founder-run companies more valuable, because founders are smarter and think more long-term than investors.

- Lazy Investors: Much as we would like to blame others for our misfortunes, the truth is that get the corporate governance we deserve. Most of us, as investors, chose to give away our voting rights willingly because we wanted shares of the "next big thing", and at the time we did so, we rationalized it by arguing it that we would not need that voting power any time soon. I have little sympathy for the hand wringing and complaints from investors, institutional or retail, in Facebook that management is not listening to them. Investing in Facebook and complaining that Mark Zuckerberg will not listen to you is like getting married to one of the Kardashians and complaining that your privacy is being invaded.

- Lax Regulators: For some of you reading this post, the villain is going to be the SEC and regulators, with the argument being that they could have protected you by banning dual class shares. I see your point, but remember that the inertia, laziness or me-tooism that led you to buy dual-class shares, will outlast the regulatory ban. Regulators cannot protect us from our own worst instincts!

The Consequences

If the essence of corporate governance is the giving shareholders the power to change management at companies, where there is a mismatch, and if those mismatches are more likely to occur at tech companies, where shareholders have unilaterally disarmed, there are predictable consequences:

- Chaotic Management Transitions: It is true that we have made it more difficult to change management at tech companies, even when that change is overdue. That said, there will be tech companies where change will occur, but my prediction is that this change will often be forced by either insider in-fighting (where co-founders and insiders turn on each other) or precipitated by a pricing collapse. While Elon Musk’s acquisition of Twitter is one of a kind, the chaos that you are observing at the company is a precursor to changes that you will see at other tech companies in the years to come.

- Locked-in Mismatches: There are other tech companies where the game has been so thoroughly tilted in favor of insiders and incumbent management that change is impossible. In these companies, as an outside investor, you have to build that reality into your valuations, leading to discounts to your value that reflect how much you trust management. In short, if management has adopted policies that are value-destructive, in the long term, there will be a much smaller chance of reversal at companies with locked-in management than at companies where change remains possible. In the case of Facebook, the company has clearly made a huge bet on the Metaverse, investing $15 billion in the most recent year and planning almost $100 billion in additional investments in the coming years. It is too early to pass judgment on whether these investments will pay off, but assume that the data that comes in over the next two years indicates that Facebook should scale back its investments and slow down. I would like to believe that Zuckerberg is too smart a businessman not to do the right thing, but the qualities that made him a successful founder (over confidence, stubbornness in the face of failure, arrogance) may very well keep him on his pre-determined path, and without checks and balances, Facebook will lose a lot more money over a longer period, before he gives in.

- Voting Share/Non-voting Shares: In a paper on valuing control from a few years ago, I argued that the differential in prices between voting and non-voting shares will reflect the value of expected control in a company, and will be higher at companies where management change is plausible than in firms where it is unlikely. When tech companies go public, it is entirely possible that there will be a honeymoon period, perhaps even an extended one, where investors are dazzled by scaling successes and are willing to overlook shortcoming, when shares with different voting rights trade at the similar prices. As disillusionment sets in, I would expect voting share premiums to rise, and to rise more at those firms where investors trust managers the least.

No comments:

Post a Comment