I was planning to start this post by telling you that Tesla was back in the news, but that would be misleading, since Tesla never leaves the news. Some of that attention comes from the company's products and innovations, but much of it comes from having Elon Musk as a CEO, a man who makes himself the center of every news cycle. That attention has worked in the company's favor over much of its lifetime, as it has gone from a start-up to one of the largest market cap companies in the world, disrupting multiple businesses in the process. At regular intervals, though, the company steps on its own story line, creating confusion and distractions, and during these periods, its stock price is quick to give up gains, and that has been the case for the last few weeks. As the price dropped below $200 today (October 30,2023), I decided that it was time for me to revisit and revalue the company, taking into account the news, financial and other, that has come out since my last valuation in January 2023, and to understand the dueling stories that are emerging about the company.

My Tesla History

When I write and teach valuation, I describe it as a craft, and there are very few companies that I enjoy practicing that craft more than I do with Tesla. Along the way, I have been wrong often on the company, and if you are one of those who only reads valuations by people who get it right all the time, you should skip the rest of this post, because I will cheerfully admit that I will be wrong again, though I don't know in which direction. My first valuation of Tesla was in 2013, when it was a nascent automobile firm, selling less than 25,000 cars a year, and viewed by the rest of the automobile sector with a mix of disdain and curiosity. I valued it as a luxury automobile firm that would succeed in that mission, giving it Audi-level revenues in 2023 of about $65 billion, and operating margins of 12.50% that year (reflecting luxury auto margins). To deliver this growth, I did assume that Tesla would have to invest large amounts of capital in capacity, and that this would create a significant drag on value, resulting in a equity value of just under $10 billion.

In subsequent valuations, I modified and adapted this story to reflect lessons that I learned about Tesla, along the way. First, I learned that the company was capable of generating growth much more efficiently, and more flexibly, than other auto companies, reducing the capital investment needed for growth. Second, I noticed that Tesla customers were almost fanatically attached to the company's products, and were willing to evangelize about it, yielding a brand loyalty that legacy auto companies could only dream about. Third, in a world where many companies are run by CEO who are, at best, operating automatons, and at worst, evidence of the Peter Principle at play, where incompetence rises to the top, Tesla had a CEO whose primary problem was too much vision, rather than too little. In valuation terms, that results in a company whose value shifts with narrative changes, creating not only wide swings in value, but vast divergences in opinion on value. In 2016, I looked at how Tesla's story would vary depending upon the narrative you had for the company and listed some of the possible choices in a picture:

I translated these stories into inputs on revenue growth, profit margins and reinvestment, to arrive at a template of values:

Note that is multiple stock splits ago, and the prices per share here are not comparable to the share price today, but the overall lessons contained in this table still apply. First, when you see significant disagreements about what Tesla is worth, those differences come from divergent stories, not disagreements about numbers. Second, every news story or financial disclosure about Tesla has to be used to evaluate how the company's narrative is changing, creating multiplier effects that create disproportionate value changes.

Along the way, Tesla (or more precisely, Elon Musk) has made choices that could be, at best, described as puzzling, and, at worst, as perilous for the company's long term health, from borrowing money in 2017, when equity would have been a much better choice, to setting arbitrary targets on production (remember the 5000 cars a week for the company in 2018) and cash flows (positive cash flows in 2018) that pushed the company into a corner. If you add to that the self-inflicted wounds including Musk tweeting out that he had a deal to sell the company at $420 a share, funding secured, in 2018, it is not surprising that the stock has had periods of trauma. It was after one of these downturns in 2019, when the stock hit $180 (with a market cap of $32 billion), that I bought Tesla for the first time, albeit labeling it as my corporate teenager, an investment that would frustrate me because it would get in the way of its own potential.

I profited mightily on that investment, but I sold too soon, when Tesla's market capitalization hit $150 billion, and just before COVID put the company on a new price orbit. In fact, I revisited the company's value in November 2021, when its market capitalization hit a trillion, marveling at its rise, but also noting that it was priced to deliver such wondrous results ($600-$800 billion in revenues, with 20%+ margins) that I was uncomfortable going along:

In 2022, the stock came back to earth with a vengeance, losing more than 65% of its equity value, leaving the stock (on a post-split basis) trading at close to $100 a share at the end of the year. Three weeks later, i.e., at the start of 2023, I revalued the stock, allowing for uncertainties in my estimate of revenues and margins to deliver a median value per share of $153, with significant variation in potential outcomes:

I was about a week late on my valuation, since the stock price had already broken through this value by the time I finished it, leaving my portfolio Tesla-free, in 2023.

Tesla Update

My last Tesla valuation is less than ten months old, and while that is not long in calendar time, with Tesla, it feels like an eternity, with this stock. As a lead in to updating the company’s valuation, it makes sense to start with the stock price, the market’s barometer for the company's health. The stock, which started the year in a swoon, recovered quickly in the first half of the year, peaking around mid-year at close to $300 a share.

The last four months have tested the stock, and it has given back a significant portion of its gains this year, with the stock dropping below $200 on October 30, 2023. Since earnings reports are often viewed as the catalysts for momentum shifts, I have highlighted the four earnings reports during the course of 2023, with a comparison of earnings per share reported, relative to expectations. The first earnings report, in January 2023, has been the only one where the company beat expectations, and it matched expectations in the April report, and fallen behind in the July and October reports.

The earnings per share focus misses much of Tesla’s story, and it is instructive to dig deeper into the income statement and examine how the company has performed on broader operating metrics:

In the twelve months, ending September 2023, Tesla reported operating income of $10.7 billion on revenues of $95.9 billion; that puts their revenues well ahead of my 2013 projection of $65 billion, albeit with an operating margin of 11.18%, lagging my estimate of 12.5%. That makes Tesla the eleventh largest automobile company in the world, in revenue terms, and the seventh most profitable on the list, making it more and more difficult for naysayers to argue that it is a fad that will pass. Breaking down the news in the financials by business grouping, here is what the reports reveal:

Auto business: Tesla's auto business saw revenue growth slow down from the torrid pace that it posted between 2020 and 2022, with third quarter year-on-year revenue growth dropping to single digits, but given the flat sales in the auto sector and a sluggish electric car market, it remains a stand-out. The more disappointing number, at least for those who were expecting pathways to software-company like margins for the company, was the decline in profit margins on automobiles from 2022 levels, though the 17.42% gross margin in the third quarter, while disappointing for Tesla, would have been cause for celebration at almost any of its competitors.

Energy business: Tesla's energy business, which was grounded by its acquisition of Solar City in 2016, has had a strong year, rising from 4.8% of the company's revenues in 2022 to 6.2% in the twelve months ending September 2023. In conjunction, the profitability of the business also surged in the last twelve months, and while some of this increase will average out, some of it can be attributed to a shift in emphasis to storage solutions (battery packs and other) from energy generation.

In short, Tesla's financial reports, are an illustration of how much expectations can play a role in how markets react to the news in them. The post-COVID surge in Tesla's revenues and profitability led to unrealistically high expectations of what the company can do in this decade, and the numbers, especially in the last two quarters, have acted as a reality check.

As a story stock, Tesla is affected as much by news stories about the company and its CEO, as it is by financials, and there are three big story lines about the company that bear on its value today:

Price Cuts: During the course of 2023, Tesla has repeatedly cut prices on its offerings, with the most recent ones coming earlier this month, The $1,250 reduction in the Model 3 should see its price drop to about $39,000, making it competitive, even on a purely price basis, in the mass auto market in the United States. Some of this price cutting is tactical and in response to competition, current or forecast, but some of it may reflect a shift in the company's business model.

Full Self Driving (FSD): Tesla, as a company, has pushed its work on full self driving to the forefront of its story, though there remains a divide in how far ahead Tesla is of its competition, and the long term prospects for automated driving. Its novelty and news value has made it a central theme of debate, with Tesla fans and critics using its successes and failures as grist for their social media postings. While an autopilot feature is packaged as a standard feature with Teslas, it offers FSD software, which is still in beta version, offers an enhanced autopilot model, albeit at a price of $12,000. The FSD news stories have also reignited talk of a robotaxi business for Tesla, with leaks from the company of a $25,000 vehicle specifically aimed at that business.

Cybertruck: After years of waiting, the Tesla Cybertruck is here, and it too has garnered outsized attention, partly because of its unique design and partly because it is Tesla's entree into a market, where traditional auto companies still dominate. While there is still debate about whether this product will be a niche offering or one that changes the trucking market, it has undoubtedly drawn attention to the company. In fact, the company's reservation tracker records more than two millions reservations (with deposits), though if history is a guide, the actual sales will fall well short of these numbers.

This being Tesla, there are dozens of other stories about the company, but that is par for the course. We will focus on these three stories because they have the potential to upend or alter the Tesla narrative, and by extension, its value.

Story and Valuation: Revisit and Revaluation

In my Tesla valuations through the start of 2023, I have valued Tesla as an automobile company, with the other businesses captured in top line numbers, rather than broken out individually. That does not mean that they are adding significantly to value, but that the value addition is buried in an input to value, rather than estimated standing alone. In my early 2023 valuation, I estimated an operating margin of 16% for Tesla, well above auto industry averages, because I believed that software and or the robotaxi businesses, in addition to delivering additional revenues, would augment operating margins, since they are high-margin businesses.

The news stories about Tesla this year have made me reassess that point of view, since they feed into the narrative that Tesla not only believes that the software and robotaxi businesses have significant value potential as stand-alone businesses, but it is acting accordingly. To see why, let me take each of the three news story lines and work them into my Tesla narrative:

Cybertrucks: The easiest news items to weave into the Tesla narrative is the Cybertruck effect. If the advance orders are an indication of pent-up demand and the Cybertruck represents an extension into a hitherto untapped market, it does increase Tesla's revenue growth potential. There are two potential negatives to consider, and Musk referenced them during the course of the most recent earnings call. The first is that, even with clever design choices, at their rumored pricing, the margins on these trucks will be lower than on higher-end offerings. The other is that the Cybertruck may very well require dedicated production facilities, pushing up reinvestment needs. If Cybertruck sales are brisk, and the demand is strong, the positives will outweigh the negatives, but if the buzz fades, and it becomes a niche product, it may very well prove a distraction that reduces value. The value added by Cybertrucks will also depend, in part, on who buys them, with Tesla gaining more if the sales comes from truck buyers, coming from other companies, than it will if the sales comes from Tesla car buyers, which will cannibalize their own sales.

FSD: As I look at the competing arguments about Tesla's FSD research, it seems clear to me that both sides have a point. On the plus side, Tesla is clearly further along this road than any other company, not only from a technological standpoint, but also from business model and marketing standpoints. While I do not believe that charging $12,000 for FSD as an add-on will create a big market, lowering that price will open the door not only to software sales to Tesla drivers, but perhaps even to other carmakers. In addition, it seems clear to me that the Tesla robotaxi business has now moved from possible to plausible on my scale, and thus merits being taken seriously. On the minus side, I do agree that the world is not quite ready for driverless cars, on scale, and that rushing the product to market can be catastrophic.

Price cuts: The Tesla price cuts have led to a divide among Tesla bulls, with some pointing to it as the reason for Tesla's recent pricing travails and others viewing it as a masterstroke advancing it on its mission of global domination. To decide which side has the more realistic perspective, I decided to take a look at how price cuts play out in value for a generic company. The first order effect of a price cut is negative, since lowering prices will lower margins and profits, and it is easy to compute. It is the second order effects that are tricky, and I list the possibilities in the figure below, with value consequences:

In short, price cuts can, and often will, change the number of units sold, perhaps offsetting some of the downside to price cut (tactical), make it more difficult for competitors to keep up or enter your business (strategic) and expand the potential for side or supplemental businesses to thrive (synergistic). This figure explains the divide on the Tesla price cuts, with the pessimists arguing that electric car demand is too inelastic for volume increases that will compensate for the lower margins, and the optimists arguing that the value losses from lower margins will be more than offset by a long-term increase in Tesla's market share, and increase the value from their software and robotaxi businesses.

To bring these stories into play, I break Tesla down into four businesses - the auto business, the energy business, the software business and the robotaxi business. I do know that there will be Tesla optimists who will argue that there are other businesses that Tesla can enter, including insurance and robots, but for the moment, I think that the company has its hands full. I look out the landscape for these businesses in the picture below, looking at the potential size and profitability of the market for each of these businesses, as well as Tesla's standing in each.

Note that the auto business is, by far, the largest in terms of revenue potential, but it lags the other business in profitability, especially the software and robotaxi businesses, where unit economics are favorable and margins much higher. Note also that estimates for the future in the robotaxi and auto software businesses are squishy, insofar as they are till nascent, and there is much that we do not know.My Tesla story for each of these businesses is below, with revenue and profitability assumption, broken down by business:

With these stories in place, I estimate revenues, earnings and cash flows for the businesses, and in sum, for the company, and use these cash flows to estimate a value per share for the company:

In sum, the value per share that I get with Tesla's businesses broken down and allowing for divergent growth and profitability across businesses, is about $180 a share. That is higher than my estimate at the start of the year, with part of that increase coming from the higher profit potential in the side businesses, and expectations of a much larger end game in each one.

Given that this value comes from four businesses, you can break down the value into each of those businesses, and I do so below:

Just as a note of caution, these businesses are all linked together, since the battery technology that drives the auto and energy businesses are shared, and FSD software sales will be tied to car sales. Consequently, you would not be able to spin off or sell these businesses, at least as these estimated values, but it does provide a sense of investors should watch for in this company. Thus, with a chunk of value tied to FSD, from software and robotaxis, any signs of progress (failure) on the FSD front will have consequences for value.

An Action Plan

As you review my story and numbers, you will undoubtedly have very different views about Tesla going forward, and rather than tell me that you disagree with my views, which serves neither of us, please download the spreadsheet and make your own projections, by business. So, if you believe that I am massively underestimating the size of the robotaxi business, please do make your own judgment on how big it can get, with the caveat that making that business bigger will make your auto and software businesses smaller. After all, if everyone is taking robotaxis, the number of cars sold should drop off and existing car owners may be less likely to pay extra for a FSD package.

At $197 a share, Tesla remains over valued, at least based on my story, but a stock that has dropped $54 in price in the last few weeks could very well drop another $20 in the next few. To capture that possibility, I have a limit buy at my estimated value of $180, with the acceptance that it may never hit that price in this iteration. For those of you who wonder why I don't have a margin of safety (MOS), I have argued that the MOS is a blunt instrument that is most useful when you are valuing mature companies where you face a luxury of riches (lots of under valued companies). Furthermore, as my January 2023 simulation of Tesla value reveals, this is a company with more upside than downside, and that make a fair-value investment one that I can live with. Put simply, the possibility of other businesses that Tesla can enter into adds optionality that I have not incorporated into my value, and that acts as icing on the cake.

Obviously, and this will sound like the postscript from an email that you get from your investment banking friends, I am not offering this as investment advice. Unlike those investment banking email postscripts, I mean that from the heart and am not required by either regulators or lawyer to say it. I believe that investors have to take ownership of their investment decisions, and I would suggest that the only way for you to make your own judgment on Tesla is to frame your story, and value it based on that story. Of course, you are welcome to use, adapt or just ignore my spreadsheet in that process.

In my first two posts on Facebook, I noted that its most recent earnings report, and the market reaction to it, offers an opportunity for us to talk about bigger issues. I started by examining corporate governance, or its absence, and argued that some of the frustration that investors in Facebook feel about their views being ignored can be traced to a choice that they made early to give up the power to change management, by acquiescing to dual class shares. Facebook, I argued, is a corporate autocracy, with Mark Zuckerberg at its helm. In the second post, I pointed to inconsistencies in how accountants classify operating, capital and financing expenses, and the consequences for reported accounting numbers. Some of the bad news in Facebook's earnings report, especially relating to lower profitability, reflected accounting mis-categorization of R&D and expenses at Reality Labs (Facebook's Metaverse entree) as operating, rather than capital expenses. In fact, I concluded the post by arguing that investors in Facebook were pricing in their belief that the billions of dollars the company had invested in the Metaverse would be wasted, and argued that Facebook faced some of the blame, for not telling a compelling story to back the investment. In this post, I want to focus on that point, starting with a discussion of why stories matter to investors and traders and the story that propelled the company to a trillion-dollar market capitalization not that long ago. I will close with a look at why business stories can break, change and shift, focusing in particular on the forces pushing Facebook to expand or perhaps even change its story, and whether the odds favor them in that endeavor.

Narrative and Value

As someone who has spent the last four decades talking, teaching and doing valuation that we have lost our way in valuation. Even as data has become more accessible and our tools have become more powerful, it is my belief that the quality of valuations has degraded over time. One reason is that valuation, at least as practiced, has become financial modeling, where Excel ninjas pull numbers from financial statements, put them into spreadsheets and extrapolate based upon past trends. Along the way, we have lost a key component of valuation, which is that every valuation tells a business story, and understanding what the story is and its weakest links is key to good valuation,

The Connection

In the first session of my valuation class, I pose a question, "What comes more naturally to you, telling a story or working with numbers?", and I very quickly add that there is no right answer that I am looking for. That is because the answer will vary across people, with some exhibiting a more natural tendency towards story-telling and others towards working with numbers. In my valuation classes, the selection bias that leads people to come back to business school, and then to pick the valuation class as an elective, also results in the majority picking the "numbers" side, though I am glad to say that I have enough history majors and literature buffs to create a sizable "story" contingent. In the immediate aftermath, I then put forth what I believe is one of the biggest hidden secrets in valuation, which is that a good valuation is not just numbers on a spreadsheet, which is the number-crunching vision, or a big business story, which is the story-tellers' variant, but a bridge between stories and numbers:

To explain what I mean by "a bridge", in a good valuation, every number you have in your valuation, from growth to margins to risk measures, should be backed up by a story about that number, and every story you tell about a company, including its great management, brand name or technological edge, has be reflected in a number in your valuation. If making this connection comes naturally to you, you are lucky and definitely the exception, because it is hard work for the rest of us. As someone who is more naturally drawn to numbers, I came to the recognition of the need for stories late to the game, and I had not only to teach myself how to tell stories but also create a process where I stayed disciplined about incorporating them into valuations. In case you are interested, I did write a book on the process that I use to convert stories to numbers, but if you are budget-constrained, many of the ideas in the book are captured in posts that I have done over time on valuation.

Stories + Numbers: The Symbiosis

The challenge in valuation, and it has only become worse in time, is that the divide between story tellers and number crunchers has only become wider over time, and has reached a point where each side not only does not understand the other, but also views it with contempt. Venture capitalist, raised on a diet of big stories and total addressable markets has little in common with bankers, trained to think in terms of EV to EBITDA multiples and accounting ROIC, and when put in a room together, it should come as no surprise that they find each other's language indecipherable. At the risk of being shunned by both groups, I will argue int his section that each side will benefit, from learning to understand and use the tools of the other side.

1. Why stories matter in a numbers world

If you are a numbers valuation, you start with some advantages. Not only will you find financial statements easier to disentangle, but you will also be able to develop a framework for converting these numbers to forecasts fairly easily. In other words, you will have no trouble creating something that looks like a legitimate valuation, with numbers details and an end value, even if that value is nonsensical. With a just-the-numbers valuation, there are four dangers that you face:

Play with numbers: When a valuation is all about the numbers, it is easy to start playing with the numbers, unconstrained by any business sense, and change the value. It is not uncommon to see analysts, when they estimate a value that they think is "too low", to increase the revenue growth rate for a company, holding all else constant, and increase the value to what they would "like it to be".

False precision: Number crunchers love precision, and the pathways they adopt to get to more precise valuations are often counter-productive, in terms of delivering more accurate valuations. From estimating the cost of capital to the fourth decimal point to forecasting all three accounting statements (income statements, balance sheet and statement of cashflows), in excruciating detail, for the next 20 years, analysts lose the forest for the trees, and produce valuations that look precise, but are not even close to being estimates of true value.

Drown in data: If the complaint that analysts in the 1970s and even the 1980s might have had is that there was not enough data, the complaint today, when they value companies, is that there is too much data. That data is not only quantitative, with company disclosures running to hundreds of pages and databases that cover thousands of companies, but also qualitative, as you can access every news story about a company over its history, and in real time. Without guard rails, it is easy to see why this data overload can overwhelm investors and analysts, and lead them, ironically, to ignore most of it.

Denial of biases: It is almost impossible to value a business without bias, with some bias coming from what you know about the business and some coming from whether you are getting paid to do the valuation, and how much. In a valuation driven entirely with numbers, analysts can fool themselves into believing that since they work with numbers, they cannot be biased, when, in fact, bias permeates every step in the process, implicitly or explicitly. Put simply, there are very facts in valuation and lots of estimates, and if you are making those estimates, you are bringing your biases

If you are a number-cruncher, at heart, and have run into these or other problems when valuing companies, bringing numbers into your valuation can not just alleviate these problems, but also help you in convincing not just other people, but yourself, about your valuation.

Stories are memorable, numbers less so: Even the most-skilled number cruncher, aided and abetted with charts and diagrams, will have a difficult time creating a valuation that is even close to being as good a compelling business story, in hooking investors and being memorable. I believe that long after my students have forgotten what growth rates and margins I assumed in the valuation of Amazon that I showed them in 2012, they will remember my characterization of Amazon as my "field of dreams company", built on the premise that if they build it (revenues), they (profits) will come.

Stories allow for consistency-tests: When your valuation numbers come from a story, it becomes almost impossible to change one input to your valuation without thinking through how that change affects your story. An increase in revenue growth, in a company in a niche market with high margins, may require a recalibration of the story to make it a more mass-market story, albeit with lower margins.

Stories allow you to screen and manage data: Having a valuation story that binds your numbers together and yields a value also allows you a framework for separating the data that matters (information) from the data that does not (distractions), and for organizing that data.

Stories lead to business follow-through: If you are a business-owner, valuing your own business, understanding the story that you are telling in that valuation is extraordinarily useful in how you run the business. Thus, if you want to follow Amazon's path to the Field of Dreams, your business strategy should be built around expanding your market and increasing revenues, while also mapping out a pathway to eventually monetizing those markets and gaining access to enough capital to be able to do so.

If you are a number cruncher like me, you will find that adding a story to your valuation will only augment your number skills and improve your valuations.

2. Why numbers matter in a story world

I am not a story-telling natural, but I have tried to look at valuation, through the eyes of story tellers, over the last few years. Again, you start with some advantages, as a skilled story teller, especially if you also have the added benefit of charisma. You can use your story telling skills to draw investors, employees and the rest of the world into your story, and if you frame it well, you may very well be able to evade the type of scrutiny that comes with numbers. There are dangers, though, including the following:

Fairy tales: Without the constraint of business first principles or explicit numbers about key inputs, you can tell stories of unstoppable growth and incredible profits for your company that are alluring, but impossible. If you are a con man, that is your end game, but even if you are not a con man, it is easy to start believing your own tall stories about businesses. As you watch the unraveling of FTX, you have to wonder whether Sam Bankman-Fried (SBF) set out to create a crypto-based Ponzi scheme, or whether this is the end result of a business story that was unchecked by any of the big name investors who participated into its growth.

Anecdotal evidence: Story tellers tend to gravitate towards anecdotal data that supports their valuation stories. Rather than drown in the data overflow world we live in, story tellers pick and choose the data that best fits their stories, and use them to good effect, often fooling themselves about viability and profitability along the way.

Unconstrained biases: If number crunchers are in denial about their biases, story tellers often revel in their biases, presenting them as evidence of the conviction that they have in their stories. Using the FTX example again, SBF was open about his belief that the future belonged to crypto, and that his entire business was built on that belief, and to his audience, composed of other true crypto-believers, this was a plus, not a minus.

In every market boom, you see the rise of story tellers, and while many crash and burn like SBF, as reality bites, there are a few that succeed, building some of our greatest business successes. One reason is that they find a way to bring numbers into their stories, with the following benefits:

Numbers give credibility to stories: As we noted in the last section, stories are hooks that draw others to a business idea, but it may not be enough to get them to invest their money in it. For that to happen, you may have to use numbers to augment and back up your business story to give it credibility and create enough confidence that you have the business sense to make it succeed.

Numbers allow for plausibility checks: If you are on the other side of a valuation pitch, especially one built almost entirely around a story, the absence of numbers can make it difficult to take the story through the 3P test, where you evaluate whether it is possible, plausible and probable. It is your obligation as an investor to push for specificity, often in terms of the market that the business is targeting and the market share and profitability numbers that will determine its profitability. Again, business owners and analysts who can respond to this demand for specifics and numbers are more likely to get the capital that they seek.

Number create accountability: For business owners and managers, the use of numbers allows for accountability, where your actual numbers on total market size, market share and profitability can be compared to your forecasts. While that lead to uncomfortable findings, i.e., that you delivered below your expectations, it is an integral part of building a successful business over time, since what you learn from the feedback can allow you to alter, modify and sometimes replace business models that are not working well.

Just as great number crunchers can benefit from bring stories into their valuations, great story tellers will benefit by bringing in numbers to add discipline to their story telling.

The Facebook Narrative

In the last few months, as Facebook has collapsed, investors seem to have forgotten about its astonishing climb in the decade prior, with market capitalization increasing from $100 billion at its IPO in 2012 to its trillion-dollar capitalization in July 2021. In my view, a key factor behind the stratospheric rise was the valuation story told by and about the company, and the story's appeal to investors.

The Facebook Story

The core of the Facebook story is its mammoth user base, especially if you include Instagram and WhatsApp as part of the Facebook ecosystem, but if that is all you focused on, you would be missing large parts of its appeal. In fact, the Facebook story has the following constituent parts:

Billions of intense users: If there is one lesson that we should have learned from our experiences with user-based and subscriber-based companies over the last decade, it is that not all users or subscribers are created equal. With Facebook, it is not just the roughly three billion people who are in its ecosystem that should draw your attention, but the amount of time they spend in it. Until TikTok recently supplanted it at the top, Facebook had the most intense user base of any social media platform, with users staying on the platform roughly an hour a day in 2019.

Sharing personal data in their postings: As a platform that encourages users to share everything with their "friends", it is undeniable that Facebook has accumulated immense amounts of data about its users. If you are a privacy purist, and you find this unconscionable, it is worth noting that these users were not dragged on to a platform and forced to share their deeply personal thoughts and feelings, against their wishes.

Which could be utilized to focus advertising at them: In 2018, at the peak of the Cambridge Analytica scandals, when people were piling on Facebook for its invasion of privacy, I noted invading user privacy, albeit with their tacit approval, lies at the core of Facebook's success in online advertising. In short, Facebook uses what it has learnt about the people inhabiting its platform to focus advertising to them.

In a world where online ads were consuming the advertising business: Facebook also benefited from a macro shift in the advertising business, where advertisers were shifting from traditional advertising modes (newspapers, television, billboards etc.) to online advertising; online advertising increased from less than 10% of total advertising in 2005 to close to 60% of total adverting in 2020.

In sum, the story that took Facebook to the heights that it reached in July 2021 was that of an online advertising juggernaut, whose success came from using the data that it had acquired on the billions of users who spent a chunk of their days on on its platform, to deliver focused advertising.

And its appeal

Every business, especially in its youth, markets itself with a story and it is worth asking why investors took to Facebook's story so quickly and attached so much value to it.

Simple and easy to understand: In telling business stories, I argue that it pays to keep the story simple and to give it focus, i.e., lay out the pathways that the story will lead the company to make money. Facebook clearly followed this practice, with a story that was simple and easy for in investors to understand and to price in. Just to provide a contrast, consider how much more difficult it is for Palantir or Snowflake to tell a business story that investors can grasp, let alone value.

Personal experiences with business: Adding to the first point, investors feel more comfortable valuing businesses, where they have sampled the products or services offered by these businesses and understand what sets them apart (or does not) from the competition. I would wager that almost every investor, professional or retail, who invested in Facebook has a Facebook page, and even if they do not post much on the page, have seen ads directed specifically at them on that page.

Backed up by data: In the last decade, we have seen other companies with simple stories that we have personal connections to, like Uber, Airbnb and Twitter, go public, but none of them received the rapturous response that Facebook did, at least until July 2021. The reason is simple. Unlike those companies, Facebook, from day one as a public company, has been able to back its story up with numbers, both in terms of revenues and profitability, as can be seen in the graph below, where I look at its revenues and operating profits from 2012 to 2021:

With revenues growing from less than $4 billion in 2011 to $118 billion in 2021, and operating margins of more than 40%,through almost the entire period, it is easy to see why both value and growth investors gravitated to this stock.

With value consequences

I have valued Facebook many times over the last decade, and have bought and sold based upon my valuations. For those of you who have been following these valuations, I am sure that you are well aware that my most recent valuation of Facebook, at the end of February 2022, was $346 per share, well above the stock price then of $220/share:

Having bought shares in the company at $133/share after the Cambridge Analytica scandal in 2018, I stayed invested in the company. Obviously, at today's price of just over $100/share, it should be time for regrets, but I have none. There are clearly aspects of my valuation, where I overreached, including revenue growth of 8% a year that I would reset to a lower number, with the recognition that online advertising is seeing growth level off, faster than I thought it would, and is more cyclical than I assumed it would be. As for profitability, my estimated target operating margin of 40% looks hopelessly optimistic, given that the operating margins in the last twelve months is closer to 20%, but as I noted in my last post, that drop is less a reflection of a collapse in the online advertising business model and more the result of Facebook's big bet of Metaverse, and the expenses emanating from that bet.

Narrative Changes and Resets

The value of a business is, in large part, driven by your story for the business, but that story will change over time, as the business, the market it is in and the macro environment change. In some cases, the story can get bigger, leading to higher value, and in some, it can get smaller, and we will begin by looking at why business stories change, and classify those changes, before looking at the Facebook story.

Narrative Breaks, Changes and Shifts

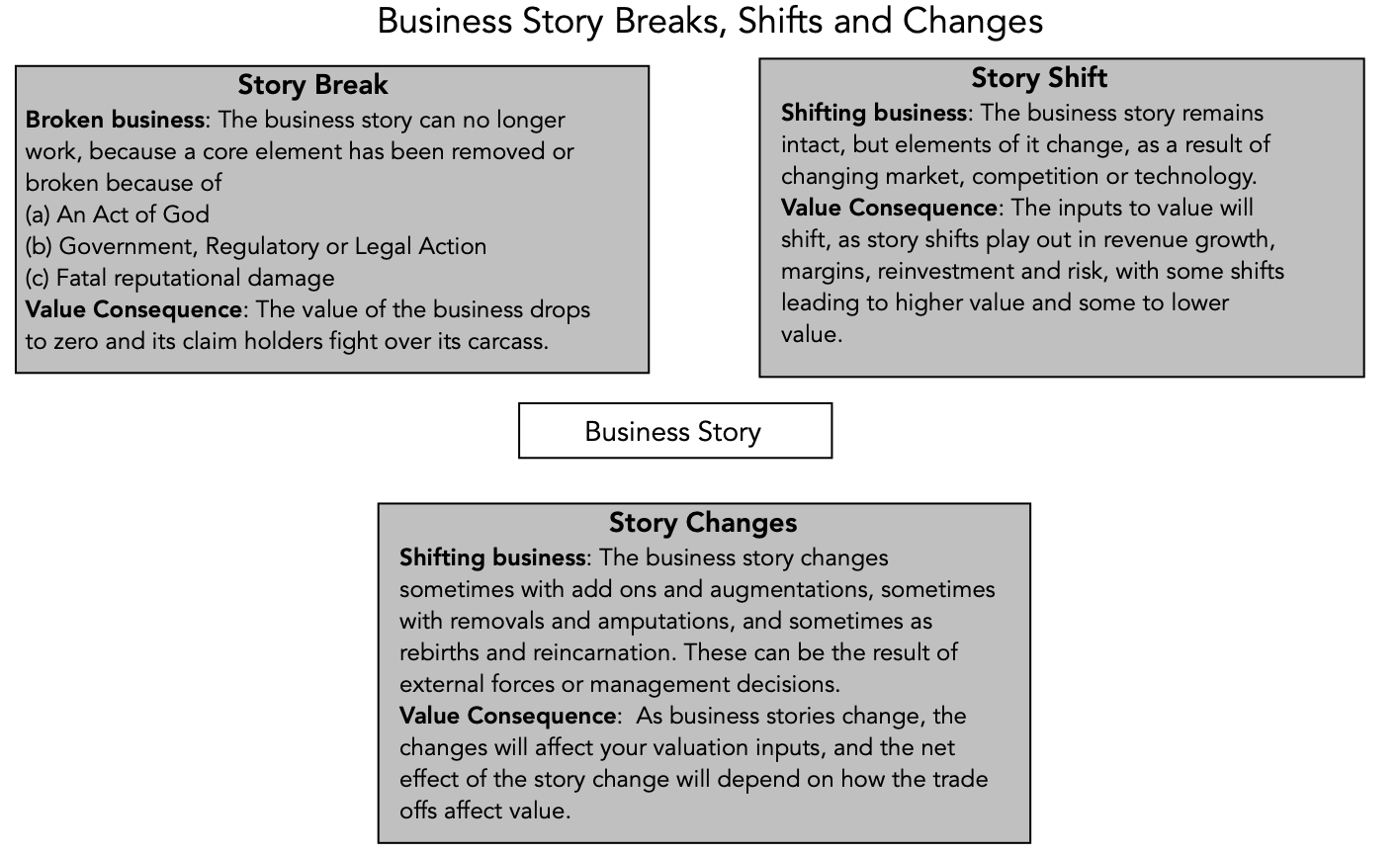

If business stores change over time, what form will that change take? To answer the question, I broke down business story changes into three groups, with the proviso that there are some business changes that fall into more than one group:

Story breaks: The most consequential value change comes from a story break, where a key component of a business story breaks, sometimes due to external factors and sometimes due to miscalculations and missteps on the part of the management of the company. In the former group, we would include acts of God (terrorism, a hurricane or COVID) and regulatory or legal events (failure to get regulatory approval for a drug, for a pharmaceutical company) that put an end to a business model. In the latter, we would count companies where management pushed the limits of the law to breaking point and beyond, damaging its reputation to the point that it cannot continue in business.

Story shifts: At the other end of the spectrum are story shifts, where the core business model remains intact, but its contours (in terms of growth, profitability and risk) change, as the result of market changes (market growth surges, slows or stalls), competitive dynamics (a competitor introduces a new product or withdraws an existing one) or technology (working in favor of the story or against it). Note the resulting changes in value can be substantial, and in either direction, depending on how and how much the valuation inputs change as a result of the story shift.

Story changes: Finally, there are story changes, where a company augments an existing business story by investing in or acquiring a new business, shrinks its existing business by withdrawing or divesting an existing business or product or attempts a story reset or rebirth, by replacing an existing business story with a new one.

I summarize these possible story alterations in the picture below:

As you can see from the types of changes that can occur, some business story changes are triggered by external forces, and can be traced to changes in macroeconomic conditions, country risk or regulatory/legal structures, some business story changes are the result of management actions, at the company or at its competitors and some business story changes are the consequence of a company scaling up and/or aging. It is worth noting that disruption, at its core, creates changes to a sector or industry that can break some status-quo businesses, while creating new ones with significant value.

Facebook: A Narrative Reset?

In the last section, we looked at the incredible success that Facebook had between 2012 and 2021 with its user-driven, online advertising business model, both in terms of market capitalization (rising from $100 billion to $ 1 trillion) and in terms of operating results. You may wonder why a company that has had this much success with its story would need to change, but the last year and a half is an indication of how quickly business conditions can change.

Forces driving a reset

Facebook's original business story was built on two premises, with the first being the use of data that it obtained on its customers to deliver more focused advertisements and the second being the rapid growth in the online advertising business, largely at the expense of traditional advertising. Both premises are being challenged by developments on the ground, and as they weaken, so is the pull of the Facebook story.

On the privacy front, the Cambridge Analytica episode, though small in its direct impact, cast light on an unpleasant truth about the Facebook business model, where the invasion of user privacy is a feature of its business story, not a bug. Put differently, if Facebook decides not to use the information that you provide it, in the course of your postings, in its business model, a large portion of its allure to advertisers disappears.

The halcyon days of growth in the online advertising market are behind us, as it acquires a dominant share of overall advertising, and starts growing at rates that reflect growth in total advertising. As one of the two biggest players in the market, with Google being the other one, Facebook does not have much room on the upside for growth.

While many investors were shocked by the stagnant revenues that Facebook reported in its most earnings report, and some have attributed that to a slowing economy, the truth is that the pressures on Facebook's business story have been building for a while, and it is only the speed with which the story has unraveled that is shocking.

Choices for the company

Faced with slower revenue growth and concerned about the effect that privacy regulations in the EU and the US will alter its business model, Facebook has been struggling with a way forward. As I see it, there were three choices that Facebook could have made (though we know, in hindsight, which one they picked):

Acceptance: Accept the reality that they are now a mature player in a slow-growth business (online advertising), albeit one in which they are immensely profitable, and scale back growth plans and spending. While this may strike some as giving up, it does provide a pathway for Facebook to become a cash cow, investing just enough in R&D to keep its existing business going for the foreseeable future, while returning huge amounts of cash to its investors each year (as dividends or buybacks).

Denial: View the slowdown in growth in the online adverting market as temporary, and stay with its existing business model, built around aggressively seeking to gain market share from both traditional players in the advertising market and smaller online competitors. With this path, the company may be able to post higher revenue growth than if it follows the acceptance path, but perhaps with lower operating margins and more spending on R&D, if market growth is leveling off.

Rebirth: The choice with the most upside as well as the greatest downside is for Facebook to try to reinvent itself in a new business. That may require substantial reinvestment to enter the business, and hopefully draw on Facebook’s biggest strength, i.e., its intense and mammoth user base.

Facebook did pick the third path, and it made the choice well before the revenue slowdown in the most recent year, perhaps as early as 2014, with its acquisition of Oculus for $2 billion. In the last three years, the push into the Metaverse has intensified, with billions invested in Reality Labs and a name change for the company.

Facebook has also telegraphed its commitment to be a leading player in this space, planning to invest close to $100 billion, over the next decade. The big question, as I noted in my last post, that hangs over the company is whether this investment can create enough in additional earnings and cash flows to cover these huge upfront costs.

What's the story?

Facebook’s plans to invest tens of billions in the Metaverse makes it an expensive venture, by any standards, and there are some who suggest that it is unprecedented, especially in technology, which many view as a capital-light business. That perception, though, collides with reality, especially when you look at how much big tech companies have been willing to invest to enter new businesses, albeit with mixed results.

Microsoft invested $15 billion for its entry in 2015 into Azure, its cloud business, and it has invested tens of billions in data centers since, expanding its reach. That investment has paid off both quickly and lucratively, and has played a role in Microsoft's rise in market capitalization.

Google, renamed itself Alphabet in 2015, in a well-publicized effort to rebrand itself as more than just a search engine, and has invested tens of billions of dollars in its other businesses since, but with a payoff primarily in its cloud business, which generated $19.2 billion in revenues in 2021. Just to provide a measure of how its other bets are still lagging, Google generated only $753 million in revenues from its other businesses in 2021, almost unchanged from its revenues in 2019 and 2020.

Amazon has also invested tens of billions in its other businesses, with its biggest payoff coming in the cloud business (notice a pattern here). It has much less to show for its investments in Alexa and entertainment, and it is estimated to have lost $5 billion on its Alexa division in 2021 and spent $13 billion on new content for Amazon video.

Facebook, Microsoft and Google have all used the cash flows from their core businesses (Online advertising for Facebook and Google, Windows and Office for Microsoft) to fund their entry into new businesses, but at Amazon, it is the AWS (its cloud business) that has provided the profits and cash flows to cover its growth plans in other businesses.

Facebook's investment plans for the Metaverse represent a big bet, but it is not an unprecedented one, which raises the question of why investors have been less willing to cut it slack than they have for its large tech competitors. One reason is timing, since markets are much more receptive to big growth investments, when times are good, as they were for much of the last decade, than in bad times, as much of 2022 has been. The other is the story line that backs the investment. Fairly or otherwise, the big cloud investments that Microsoft, Google and Amazon made came with story lines of growth and profitability that investors bought into, and for the most part, the results have justified that view. The more opaque investments, including Google's bets and Amazon's Alexa and prime video spending have been viewed more skeptically. The problem that most investors have with Facebook's Metaverse investment is that it is not just that the payoff is uncertain, but it is unclear what business the payoff will come from. After all, the Metaverse is a space (virtual), not a business, and to make money in that space, you need a business model, which Facebook has not provided much guidance on. In fact, the most detailed document that I was able to find anything on Facebook's Metaverse plans were from 2015, where Zuckerberg described his vision for the business, and from 2018, in a 50-page presentation that Facebook, where the company talks about revenues coming from advertising and hardware, but only in very general terms. It is true that Facebook has laid out its Connect 2021 vision online, but the document is heavy on hype and technology, and light on business details.

As I see it, the combination of market conditions and opacity about business plans is creating the worst of all combinations for Facebook, in financial markets. The market has clarity about how much Facebook plans to spend on the Metaverse and is not just skeptical, but extremely confused, about how exactly Facebook will make money in the Metaverse. To give you a sense of how negative investors are about Facebook's future prospects, I created the most conservative estimate of value, which I call my Doomsday valuation, for the company based upon the following assumptions:

I used the company's actual operating income from its online advertising business from the last twelve months, weighed down as they are from a slowing economy and a stronger economy, and assumed no growth and a remaining life of 20 years for the business, with a zero liquidation value at the end of year 20.

I assumed that the company will continue to spend R&D at the same scorching rate that it set in the last twelve months, where it spent just over $32 billion on R&D, for the next 20 years.

I also assumed that not only will Facebook to lose $10 billion a year on the Metaverse, but also that this will continue for the next decade and beyond, with no payoff in terms of increased revenues or earnings from this spending.

I assume that Facebook is a risky company, falling at the 75th percentile of all US companies in terms of risk, and give it a cost of capital of 9%.

The table below shows the value that I estimate with this combination of assumptions, and compares it to the value that I would obtain, if I removed the Metaverse numbers from the valuation:

Note that in Doomsday scenario, where Facebook continues to spend money on R&D and invest heavily in the Metaverse, with no payoff in higher growth or longer business life from those investments, the value of equity that I obtain is $258.6 billion. Doing the valuation with the Metaverse revenues and expenses removed from the mix yields $330 billion, suggesting that treating the entire Metaverse investment as wasted expenditure reduces Facebook's value by approximately $71 billion.

The market capitalization of Facebook on October 29, 2022 was $247 billion, below the Doomsday scenario value, indicating that investors were, in fact, treating the $100 billion to be invested in the Metaverse as a wasted expense, a remarkably cynical and pessimistic take on a company that has had a history of delivering profits. The market capitalization has risen to $311 billion as of November 15, 2022, and while that suggests a more positive perspective, that value still reflects a presumption that the Metaverse investment will destroy about $18.9 billion of Facebook's value. In truth, using a more realistic growth rate (rather than zero) or lowering the cost of capital (from 9% to 8%, the median cost of capital for a US company) or extending the life of the company (from 20 years to a longer period) can only add value to Facebook, and you can experiment with these inputs in the attached spreadsheet.

Turning the Trust Corner

It is undeniable that Facebook has lost the trust of investors, and that it is being priced on assumptions that reflect that mistrust. In my experience, trying to jawbone investors to trust you does not work, but there is a plan of action that Facebook can follow, that will start the process of rebuilding trust :

Tell with a business story for the Metaverse: Investors do not have a clear sense of what the Metaverse is, and more importantly, the business opportunities that exist in that space. Facebook needs to fill in that gap with a business story for its investments, laying out what is sees as a pathway to making money in that virtual world, as well as the strengths it will bring to delivering value on this path. I am sure that Facebook is much more qualified than I am to frame this story, but just in case they could use some guidance, here are a few possible Metaverse business models:

Of these choices, advertising clearly is the most logical extension of their existing business, but it also offers the least upside, since the company is already a dominant player in the online ad business. The acquisition of Oculus and the VR headsets that Facebook sells give it a foothold in the hardware business, but hardware is a business with lower margins and limited market size. The most lucrative story, in my view, is a ecosystem story, where Facebook gains a dominant share of the virtual world, and takes a slice of any business (transactions, gaming, subscriptions) done in that world, mirroring what Apple has done in its iPhone ecosystem. It is worth remembering that the audience that you are trying to sell this business story to is not the audience that you will be seeking out in the Metaverse, which would imply that your story should be less about technology and more about business. (I may be old and cranky. I have zero interest in the virtual world, but as a Facebook investor, I would be interested to learn its business model for this world.)

Build in specifics into your investment story: Facebook has been clear about its plans to invest billions in its new businesses, but rather than just emphasizing the total amount that it plans to make, it would be better served connecting its investment plans with the business story being told. If nothing else, it would be useful to know how much of the $12 billion spent in Reality Labs was spent on people, on technology, on software and in making better VR glasses and why all of this spending is bringing the company closer to a money-making business model.

With markers on operating payoffs: I know that there are huge uncertainties overhanging these investments, but it would still make sense to give rough estimates of how Facebook expects revenues and operating margins to evolve on its Metaverse investment, over time. That will give investors and managers targets to track, as the company delivers results, and use the results (positive or negative) to make changes in the way future investments are made.

And escape hatches, if things don't work out: While many companies refuse to talk about what their plans are, if a business does not pan out, viewing it as a sign of weakness or lack of conviction, I believe that Facebook will be best served if they are open about what can go wrong with their Metaverse bet, and not only about what they are doing to protect themselves, if it happens, but also exit plans, if they decide to walk away. After all, if the market is already assuming the worst, as it was just a couple of weeks ago, how can any scenario you present, no matter how negative, worsen your market standing?

As I mentioned in my first post on Facebook a couple of weeks ago, I made an exception to my rule of not doubling down and doubled my holding of Facebook on November 4, 2022, because its valuation looks compelling. I did so with the acceptance that I will have little influence over the management of the company, in general, and Mark Zuckerberg, in particular, and it is entirely possible that I will come to regret it. If I do so, I am sure that many of you will remind me, and I okay with that as well!

Just over a week ago, I valued Zomato ahead of its market debut, and as with almost every valuation that I do on this forum, I heard from many of you. Some of you felt that I was being far too generous in my assumptions about market share and profitability, for a company with no history of making money, and that I was over valuing the company. Many others argued that I was understating the growth in the Indian food market and the company's potential to enter new markets, and thus undervaluing the company, a point that the market made even more emphatically by pricing the stock at about three times my estimated value. A few of you posited that I was missing the point entirely, and that Zomato is a trader's game, and that there are plenty of reasons for traders to be optimistic about its future prospects. In this post, rather than impose my story (and value) on you, I offer a template for telling your own story about Zomato, and arriving at your own estimate of value.

The Prelude

After I posted my valuation last week, I did find some of the portrayals of my post to be a little unsettling. Some started by describing me as some kind of valuation luminary, and then proceeding to describe what I did to arrive at value as the result of deeply insightful research. Let me dispel both delusions. First, there is nothing in valuation that merits the use of “expert” or “guru” as a descriptor, since it is for the most part, common sense, layered with a few valuation basics. Second, while valuation practitioners have created their own buzzwords to create an aura of mystery, and added complexities, often with no reason other than to intimidate outsiders, I believe that anyone should be able to value a company, as I hope to show later in this post. There was also some who misread my post to imply that I disliked Zomato as a company, or that I was trying to talk others out of investing in the company. Neither assertion is true, and since they relate to what I view as fundamental truths about investing, let me elaborate:

Good Company versus Good Investment: While it is true that, at least in my assessment, Zomato is over priced, making it a bad investment, it does not follow that it is a bad company. I have written about the contrast between good investments and good companies before, but the picture below captures the essence:

In short, your assessment of whether a company is good, average or bad is based upon how you see their business model playing out in future earnings and cash flows, but your assessment of whether it is a good investment depends upon whether your expectations for the company are more positive or negative than the market expectations for that company. My story for Zomato is a very positive one, where the company not only maintains its market share of a growing Indian market, but preserves its profitability, in the face of competition. That is one reason that I emphasized that unlike some, who have concluded that its money-losing status and big ambitions make it a "bad" company, my conclusion is that it is a good company. That said, the market seems to be pricing in the expectation that it will be a great company, and in my view, that judgment is premature.

Taking ownership of investment decisions: I value companies for an audience of one, and that audience member is forgiving and understanding, because I see him in the mirror every day. It has always been my belief that as investors, each of us needs to take ownership of our investment decisions, and that buying or selling a company because someone else is doing so, even if that person has legendary investment credentials, is a dereliction of investment due diligence. Thus, if you find Zomato to be cheap and buy it, I have no desire to talk you out of your decision, since it is your money that you are investing, and that decision should be based upon your assessment of the company's prospects, not mine.

If investing is all about market price and how it relates to your assessment of value, it follows that there will never be consensus, and that disagreement is not only part and parcel of the process, but a healthy component in good valuation.

Valuation Storytelling: The Feedback Loop

In my valuation of Zomato, I laid out the story that I was telling about the company and how it played out in valuation numbers. It is part of a broader theme that I have harped on for years, which is that a good valuation is a bridge between story and numbers, and in my book on how to build that bridge, I talked about a five-step process:

In my last post on Zomato, you saw much of this process play out, but I want to focus on the fifth step, i.e., keeping the feedback loop open, and what it requires:

Talk to a diverse audience: We live in a world of specialization, in almost every aspect of life, and that trend comes with mixed blessings. On the plus side, we now have experts who have spent their entire lives delving into an extraordinarily narrow slice of a discipline, often at the expense of the rest of that discipline. On the minus side, this expertise creates tunnel vision, where these experts often lose the forest for the trees. To make things worse, we have created workplaces, where these specialists often interact only with each other, making their isolation almost complete. I am lucky that I am able to interact with people with very different backgrounds (bankers, VCs, founders, CFOs, regulators), from different geographies and with very different perspectives, through my teaching and writing, and my suggestion is that you hang out less with people who think just like you do (often because they have the same training and credentials) and more with people who do not.

Transparency over opacity: You have all heard the old saying about economists (and market gurus) needing three hands, because they constantly seem to have two of them busy, with their "on the one hand, and the other" prevarications about the future, that leave listeners confused about what they are predicting. I start with my valuation classes with the motto that I would rather be transparently wrong than opaquely right. Consequently, when I value companies, I try to take a stand on value, and be open about process, data and mechanics, so that anyone can not only replicate what I did, but also find their own points of disagreement, and reflect those changes in their own assessed values. I am also well aware of the risk that by putting out valuation details, I will be proven wrong in the future, but I like the accountability that comes with disclosure. In commenting on my Zomato valuation, some of you pointed to how wrong I have been in valuing Uber and Tesla in the past, and while that is fair game, I have made peace (really) with my mistakes.

Listen to those who disagree with you: I try to listen to those who disagree with me on any forum, whether it be social media or snail mail, for a very selfish reason. On every company that I value, I know that there are people out there who know more than I do about some aspect of the company (its products, market or competition) that I am valuing, and I can learn from them. With Zomato, for instance, I have learned about online food delivery and restaurants in India in the two weeks since I posted my Zomato valuation. I have some understanding of why Zomato Pro has not caught on as quickly as the company thought it would, why some of you prefer Swiggy, and even what you like to order from restaurants. (Biryani seems to a much bigger draw, for Indian diners, than it was in the days that I was growing up in India.)

Be willing to change: The three most freeing words in investing and valuation are “I was wrong”, and I would be lying if I said they comes easily to me. That said, I find it easier to say those words now that I have had practice, and while some view this as an admission of weakness, saying it releases you to tell a better, and sometimes different, story. Bill Gurley’s critique of my narrow definitions of total market in my first Uber valuation significantly changed not only my valuation of that company, but has played a role in how I estimate total market size and value sharing economy companies.

The feedback that I have received on Zomato has already had tangible effects on my valuation. For instance, some of you noted that the corporate tax rate in India is 25%, not 30%, and while the Indian tax code with its predilection to add in surcharges that seem to last forever, and exceptions, still leaves me confused, I will concede on this point (pushing up my value per share marginally from 41 INR/share to about 43 INR/share). I have had pushback on my story’s focus on Indian food delivery, with some pointing to the potential for Zomato to expand its market globally, and others to the expansion possibilities in Indian grocery deliveries and from cloud kitchens. While I believe that the networking advantage that works to Zomato’s benefits will stymie them if they try to expand to large foreign markets and that the grocery delivery market, at least for the moment, offers too small a slice of revenues to be a game changer for the company, those are legitimate points.

A DIY Valuation of Zomato

If, as you read my Zomato valuation, you found yourself disagreeing with me, I would like to offer you a way of valuing the company, with your disagreements incorporated into the value. Put simply, I will take care of the background work and the valuation mechanics, if you can supply the story. So, if you are ready, let’s go!

1. Total Addressable Market & Scaling Growth

The first and biggest part of the Zomato story is the total market that it can go after, since it defines how big a story you can tell, and by extension, how big your value can be. In my valuation, I assumed that Zomato’s primary revenues would continue to come from customers ordering food from restaurants for pickup and delivery, and that notwithstanding its global ambitions, India will remain its main market. That assumption led to my base case estimate of about 2,000 billion rupees (just over $25 billion) for the total market. This was the assumption that got the most pushback, on two fronts, first that I was ignoring the possibility that Zomato’s global reach could expand that market and second that adding grocery deliveries could make the market bigger. Some also mentioned the potential for growth from cloud kitchens, i.e., restaurants (small and large) that offer food only for delivery. So, with no further ado, here are your choices:

For pessimists about Indian growth and eating habits, I offer the possibility that the total market will grow to only 1,125 billion ($15 billion) in ten years. For optimists, allowing for more growth in the Indian market or adding global growth makes the market bigger, and adding grocery deliveries to the total market more than doubles the market. In addition, you can make a judgment on whether the growth will be front ended (more growth in the early years) or spread evenly over time:

This choice will be tied to how quickly you think that the Indian economy and food delivery market will develop over time.

2. Market Share

Zomato is currently one of the two largest companies in the Indian food delivery market, with a market share that is just above the the 40%. In my valuation, I assume that the food delivery market, following a pattern that seems to be forming globally, will remain dominated by a couple of players, and leave the market share at 40%. Many of you suggested that the Indian market’s diversity, across regions and income classes, would result in a more splintered market, with lower market share, but a few argued that Zomato’s capital raise would allow it to dominate the market, earning an even higher market share:

In making this judgment, keep in mind that the more expansively you define the total market, the more you may have to pull back on market share. Also, if you do choose a dominant market share (60% or higher), consider the potential for legal and regulatory pushback.

3. Revenue Slice

The driver for the online food delivery business remains the slice of the total food order that accrues to them as base revenues, and this slice is what has to use to pay delivery personnel, cover operating costs and be used to acquire new customers. In my base case valuation, I assumed that Zomato would get to keep the 22% of gross order value in the future, a little higher than its COVID-affected FY 2021 numbers and a little lower than its FY 2020 numbers. As Zomato tries to maintain its leading market share of the Indian market, this number will be the one that will come under the most pressure, since an aggressive competitor (like Amazon Food) may be willing to settle for a lower percentage. Note that there is also the possibility that the Indian food delivery market will end up dominated by two or three companies, and that these companies could come to an implicit agreement to leave the GOV slice untouched. That would be unfair to restaurants, but will improve the bottom line for the online delivery companies:

In making a choice on revenue slice, recognize that it will be affected by your choices on market size and market share. Thus, if your total market is much bigger, because you have added in grocery deliveries, you should also be using a lower revenue slice, since grocery stores, with their lower profit margins, are reluctant to let delivery companies keep more than 10% of the order. In the US, for instance, large grocers have pushed back against Instacart’s cut (about 9%) of gross order value, and have started their own delivery services.

4. Operating Margins & Pathway to Profitability

In my valuation of Zomato, I noted that one of the advantages of being an intermediary is that the gross and operating margins tend to be high, once growth subsides that the expenses (selling and advertising costs) associated with delivering that growth scale down. In my base case, I assumed a pre-tax target operating margin of 35%, but that margin will depend on how the competitive landscape evolves. If you have only two or three players, with a live-and-let-live attitude, margins will be high for all of the competitors, but if they continue to try to aggressively claw back from market share, through advertising and discounting, they will decline for all of the players.

In my Zomato valuation, I also assumed that the company would continue to lose money in the near term, but that operating margins would converge on the target value in year 7. This assumption implicitly stands in for your views on how smooth the pathway to profitability will be for Zomato, with rockier pathways leading to a longer time period before you reach the target margin:

Here again, the assumptions about margins will depend on the businesses that you believe that Zomato can enter, using its platform capabilities. In the last week, I have heard arguments that Zomato can go beyond food delivery into running cloud kitchens, enter the health/fitness market and even be a lender to restaurants. While all of these are possible, these are businesses with very different profitability profiles, and are unlikely to earn operating margins even remotely close to the margins that can be earned in the online food delivery business.

5. Reinvestment

The key ingredient connecting value to growth is the reinvestment needed to sustain that growth. Put simply, a company that has to reinvest large amounts to deliver a specific growth rate will have lower cash flows and be worth less than an another company with the same growth rate, but lower reinvestment needs. The input that I used in the Zomato valuation to bring in reinvestment is the sales to capital ratio, a metric measuring how much revenue is generated for each dollar of capital invested, with reinvestment defined broadly to include net capital expenditures (capital expenditures minus depreciation), working capital needs, technology investments in the platform and acquisitions, with a higher number reflecting more efficient reinvestment. In my story, I see a continuation of their historical pattern of reinvesting in acquisitions and technology, albeit with more efficient growth in the near term, as the company bounces back from the COVID effect; my sales to capital ratio for next year is 5.00, dropping to 3.00 in years 2-5, before settling into 2.50 in steady state. Here again, there is room for debate, since you could argue for less reinvestment in the future (than I am assuming), based upon past acquisitions paying off, or for more reinvestment, if the company tries to buy its way into new markets and businesses.

Since the sales to capital ratio is not one that is widely reported, you may find yourself lacking perspective on what comprises a high, low or typical number.

6. Risk

There are two risk parameters in intrinsic valuation, the cost of capital accounting for the risk or variability in expected cash flows and the failure probability incorporating the risk that your company will not make it as a going concern. In the Zomato valuation, I attached a 10% chance of failure, with the large cash balance (especially after the IPO) offsetting concerns from the company's money losing, cash burning status. For the cost of capital, I followed the traditional route of estimating the company's costs of equity (based upon its exposure to market risk) and after-tax cost of debt, to arrive at an initial cost of capital of 10.25%, which I lowered over time to 8.97%, with both numbers in Indian rupees. For those of you who may disagree with my estimates on these numbers, I will make the confession that in this valuation, this input is not on my top ten list of key inputs. To see why, consider this histogram of costs of capital (that I computed) for publicly traded Indian companies in July 2021:

Note that 80% of Indian companies have costs of capital between 8.01% and 13.16%, and that half have costs of capital between 9.50% and 12.06%. To estimate a cost of capital for Zomato, consider this simplistic (but effective) approach, based on these estimates:

Thus, if you feel that I have underestimated Zomato's risk in my valuation, consider going with an initial cost of capital of 12.06% (the third quartile), whereas if you believe that I have overestimated the risk, go with 9.50% (the first quartile). Then, move on to the inputs that really matter, since, in my view, this is not one of them.

Possible, Plausible and Probable

A common pushback against story telling is that it allows investors, analysts and appraisers to let their imaginations run riot, creating fairy tale valuations. It is to counter that possibility that I argue that every valuation story has to go through a three part test:

As you navigate your way through the choices, you may be tempted as an optimist to go with the most positive (for Zomato's value) choices on each variable (biggest market, highest market share, highest margin, lowest cost of capital) or the most negative (smallest market, lowest market share, lowest margin, highest cost of capital). In fact, the former if often labeled a "best case" and the latter a "worst case" valuation, when in fact, neither passes the possible/plausible/probable test, since assuming that you will go after the biggest market will mean accepting lower margins and higher reinvestment. Thus, I could tell you that the best case value is ₹423 and that my worst case value is ₹0, but that would be both useless and misleading. That said, you can already see, no matter what your priors, that there is a whole range of stories for Zomato that pass the test, and that they can yield values per share that are very different:

No failure risk in juggernaut stories, 10% risk in others